This blog is part of a project exploring how the agenda for economic growth is being reshaped by forces of change, particularly technological change.

The 2010s have not been kind to the global economy. Global growth has slowed. It also faces weak prospects in the decade ahead. What is happening?

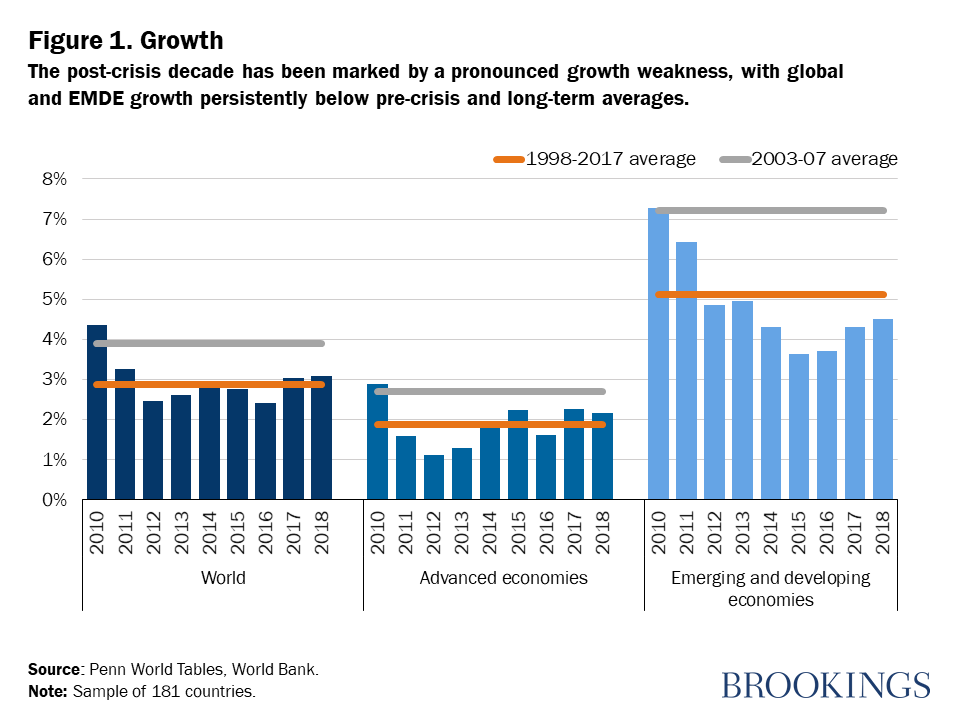

Global growth has fallen sharply below its average prior to the global financial crisis of 2007-09. It has fallen even below its long-term average (Figure 1). Several factors have contributed to this weak performance: legacies of the global financial crisis, the post-crisis weakness in commodity prices, the 2011-12 euro area debt crisis, currency crises in some large emerging markets, and recent trade tensions between major economies. But as we analyze in our chapter in the just-published book “Growth in a Time of Change,” the growth slowdown is not explained by these cyclical factors alone. Multiple structural factors also have played a role, slowing global potential growth—the pace of growth the global economy can sustain at full capacity and full employment (Figure 2).

Why has potential growth slowed since the global financial crisis?

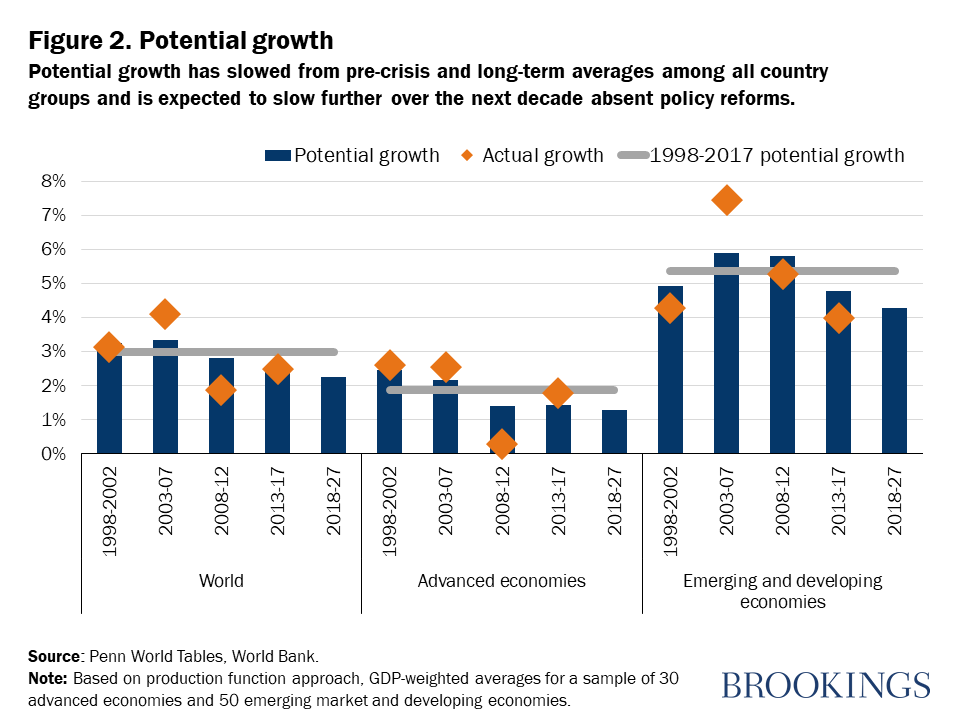

Our estimates indicate that, during 2013-17, global potential growth (2.5 percent per year) fell 0.5 percentage point below its long-term average (1998-2017)—and even further below its pre-crisis average (2003-07). The weakness in potential growth has been broad-based, affecting roughly nine-tenths of advanced economies and almost half of emerging and developing economies (EMDEs), together representing about 70 percent of global GDP. In advanced economies, potential growth slowed to 1.4 percent per year during 2013-17, 0.5 percentage point below its long-term average. Potential growth in EMDEs slowed to 4.8 percent per year, 0.6 percentage point below its long-term average.

The post-crisis weakness in potential growth reflects a host of factors, including weaker-than-average rates of capital accumulation, slower total factor productivity growth, and slowing working-age population growth. Of the 0.5 percentage-point fall in post-crisis global potential growth below its long-term average, about half can be attributed to weaker capital accumulation and the remainder in about equal measure to weaker productivity growth and slower labor supply growth.

Weak global capital accumulation is accounted for mainly by subdued investment in advanced economies in the wake of the financial crises in the United States and Europe, and a policy-driven rebalancing away from investment in China. Unfavorable demographics and slowing productivity growth have been features of both advanced economies and EMDEs.

In EMDEs, productivity growth surged to 2.5 percent per year in pre-crisis years, reflecting productivity-enhancing investment, partly financed by capital inflows. Reforms of policy frameworks after the financial crises of the late 1990s and early 2000s and greater integration into global value chains (GVCs) provided a conducive environment for rapid productivity growth. Significant strides toward improving education and health outcomes over the past two decades supported both productivity growth and labor force participation. On average in EMDEs, secondary and tertiary education completion rates increased by about one-third and one-half, respectively, from the turn of the century (1998-2002) to 27 percent and 10 percent, respectively, in 2013-17. Life expectancy rose by four years to 71 years, only 10 years short of the advanced-economy average.

However, after the global financial crisis, productivity growth in EMDEs slowed to 1.9 percent per year in 2013-17. Productivity growth may have slowed as the initial wave of information and communications technologies matured. The pace of cross-country diffusion of technology may also have diminished as the growth of GVCs slowed. In addition, aging workforces may have impeded the adoption of new ideas. In commodity-exporting countries, a downgrading of expectations for long-term profitability of resource projects would have reduced investment and, with it, embodied productivity gains. Finally, the large-scale factor reallocation—especially from agriculture to manufacturing, which had supported robust EMDE productivity growth over the previous two decades—appears to be fading.

Can the new decade bring relief?

At current trends, the slowdown in potential growth will likely extend into the 2020s, with potential growth falling further. The structural forces that depressed potential growth over the past decade are likely to persist over the next. For example, demographic headwinds will intensify. In advanced economies, the working-age share of the population is set to decline further. In EMDEs, the working-age share of the population peaked in 2015, following several decades of rapid growth, and is expected to stabilize around that level for the next decade.

In a series of counterfactual scenarios, we analyze the possible impacts on potential growth of policy reforms to improve the fundamental drivers of growth. These scenarios assume that countries repeat their best 10-year improvement in factors such as investment, education, and labor force participation over the next decade—an ambitious but not an impossible goal. We find that if such reforms are implemented, the anticipated further slowdown in potential growth over the next decade can not only be contained but reversed, leading to a recovery in potential growth.

Looking forward

A reform push is necessary to improve the prospects for potential growth over the next decade. The composition and priorities of reform differ across countries. But the need to reinvigorate reforms to address structural factors hampering growth is shared by all of them. Reforms are also needed to position economies to better harness the productivity growth potential of new technologies, led by digital transformation. The opportunities to reverse the slowdown in potential growth are there. It is time to act to capture them.

Authors’ note: The authors are World Bank staff. The findings, interpretations, and conclusions expressed in this article are those of the authors. They do not necessarily represent the views of the World Bank, its Executive Directors, or the countries they represent.

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Can policy reforms reverse the slowing of potential growth?

February 27, 2020