The shift away from the five-day office work week—which the COVID-19 pandemic only accelerated—has created an existential moment for many cities across the globe. Just within the United States, this disruption brings to mind other historical moments in which a changing economy evolved beyond the existing built environment inventory and infrastructure of cities. In the same way that mill buildings were the real estate that drove the Industrial Revolution, office buildings were the real estate that drove the postwar economy. During the Industrial Revolution, cities built their business models around the activity in the mills, and were forced to adapt when manufacturing mechanized and moved to more rural areas and abroad. In the post-industrial era, cities focused on taxing the activity in, through, and around office buildings. The potential for a shift in the behavior of office users may force a similar shift in the business models of many cities.

At the same time that this shift in office utilization patterns may be solidifying into a permanent part of post-pandemic life, American cities are experiencing the worst housing crisis of the postwar era—creating a renewed opportunity and an important mandate to convert underused offices into residential properties, particularly in hotter markets.

Yet actual office-to-residential projects in large U.S. cities have been slow to pick up. This is partially because there is continued market uncertainty in many office markets, which translates into continued uncertainty about the financial value of existing buildings for owners, renters, and financing partners. Conversion activity has also been slowed because in some markets, conversion projects collide with zoning constraints, reflecting the dated notion of separating office uses from housing.

This publication is part of a broader series examining the potential of office-to-residential conversions across six U.S. case studies. The project is part of a cooperative agreement with the US Department of Housing and Urban Development, and the research team is composed of contributors from Gensler, HR&A Advisors, Brookings, and Eckholm Studios.

From the series

Local leaders across U.S. cities are eager to break the conversion impasse and could benefit from practical tools tailored to each city’s unique circumstances. Optimizing office-to-residential policy and practice is a complex technical exercise that requires understanding a city’s fiscal structure, the financial feasibility of adaptive reuse, the architectural features of a city’s building stock, real-time information about the office and residential markets, and the regulatory environments governing zoning and permitting.

The work of advancing office-to-residential conversions is made all the more challenging due to the history of segregation and exclusion in American downtowns, which establishes a larger moral and political mandate and opportunity to make progress on equity and inclusion goals in new initiatives. This mandate is directly reflected in political interventions to incorporate affordable housing for low-income households into office-to-residential conversions, whether through inclusionary zoning reforms or targeted subsidies.

Local discussions of office-to-residential conversion activity are often complicated by two related sets of issues. First, there is often a lack of broad consensus on the problem local governments are trying to solve through conversion (office market distress, city fiscal conditions, or the housing crisis), leading to difficulty in evaluating tradeoffs between solutions and arriving at locally optimal solutions.

Second, both the public sector and the public at large are hampered by a shortage of accurate, publicly accessible data about what’s actually happening with respect to office vacancies and what constitutes a healthy vacancy rate. Office market data are a reflection of a large amount of information that is often proprietary, sensitive, or opaque. Landlords, tenants, brokers, and other interested parties respond to different incentives and may report different data to different sources. In larger markets, there may be market information from multiple competing providers that does not agree even about the size and composition of buildings in the market, and in smaller markets there may be no consistent market data at all.

To complicate matters further, property leases are rarely publicly recorded in the way that sales are, and owners, tenants, and other parties may have conflicting interests in reporting the availability, quality, and lease rate for any given space. This can create an environment in which important discussions of conversion policy are conducted without the benefit of a collective understanding of current conditions. Varying motivations and competing sets of facts have made it hard for both city leaders and the public to disentangle office-to-residential “myths” from reality.

With the upheaval of the pandemic and post-pandemic era, some experts argue that many American cities are at an inflection point regarding their economic model. With the right policy environment and financial tools in place, these cities can inaugurate a period of productive, equitable adaptation—rather than one of substantial decline, requiring decades of recovery.

The purpose of this study is to provide a framework to understand local office and housing market conditions and detail policies and incentives to spur conversion, affirmatively further fair housing, or some combination of both. We also provide illustrative case studies of how different combinations of policies relating to office-to-residential conversion produce activity in six representative cities.

A case study approach

In the study team’s review of office-to-residential (O2R) conversion activities in U.S. cities, we identified several overlapping motivations for why real estate actors and local jurisdictions pursue O2R conversions. These motivations are summarized and illustrated in Table 1.

|

Motivation |

Example |

|---|---|

|

Diversify office corridors by introducing a range of uses and users beyond office hours. |

Chicago’s LaSalle Reimagined initiative will bring 1,600 mixed-income units to its downtown. |

|

Preserve historic office cores and breathe new life into historically significant architecture. |

Prior to the pandemic, Philadelphia saw the conversion of around 40 office buildings, many of which used historic preservation tax credits. |

|

Create greater density in locations with strong infrastructure (transit, power, water, etc.) outside the urban core. |

California’s Office to Housing Conversion Act streamlines conversion approvals, including in California’s many suburban office parks. |

|

Broaden the tax and revenue base for local governments. |

Buildings converted in Lower Manhattan during the mid-1990s have seen a four-fold increase in property values and tax revenues. |

|

Use existing buildings to minimize embodied carbon associated with new construction. |

CALGreen establishes minimums for embodied carbon emissions on new construction, including a compliance pathway that includes re-use. |

|

Address underlying regional needs such as the creation of affordable housing. |

The city of Atlanta has purchased office buildings to turn into affordable housing. |

Note: Work prepared by The Brookings Institution, HR&A Advisors, Inc., Gensler, and Eckholm Studios as part of a cooperative agreement with the U.S. Department of Housing and Urban Development.

The team then used a data-driven process to curate a purposive sample of six representative markets that illustrate diverse combinations of these motivations, while also representing a range of economic and demographic criteria (market size, economic trajectory, housing affordability). From this process, we selected six case study markets to focus on for our analysis: Houston; Los Angeles; Pittsburgh; St. Louis; Stamford, Conn.; and Winston-Salem, N.C.

We then conducted mixed-method research in each case study city between June 1, 2024 and October 1, 2024.1 Our research included but was not limited to:

- A total of 68 qualitative interviews with up to 16 respondents in each city, including local public sector economic development and housing leaders, commercial property owners, residential developers, lenders, and community-based organization leaders.

- Quantitative analysis of real estate market trends using data from CoStar, the most widely adopted data source in commercial real estate research due to the market-leading size of their database of lease and sales transactions.

- Physical analysis of the feasibility gap of converting up to 25 buildings in each market using Gensler’s O2R conversion algorithm, which estimates how far a base building is from possessing the features of an idealized residential building.

Further details on our methodology for selecting cities and conducting case study research are described in Appendix A.

Key lessons learned about conversion activity

Each of the case studies represents a snapshot of a given community and the ways it has considered the questions and opportunities of residential conversion. Across these different experiences, a set of common themes and forces that are driving local discussions emerged. We synthesize those patterns here as a framework for helping local governments with diverse motivations and market conditions understand office-to-residential conversion.

Across all case studies, conversion of underutilized offices creates an opportunity to address three key policy needs:

- Unmet housing demand: Some cities, such as Los Angeles and Stamford, have struggled to provide enough housing to meet regional demand for new units. Even in cities where new units have been created, the supply of units that are affordable to lower-income households generally lags far behind the demand for such units.

- Obsolete office districts: Many cities, such as Pittsburgh and Houston, have struggled to maintain fiscal and other benefits associated with aging and underperforming office buildings and office districts. As the needs and desires of office tenants have changed and as industries have shifted, older office districts may struggle to remain productive parts of the regional economy and local tax base. This fiscal and economic challenge may stem from a macro challenge with the competitiveness of the overall city and region or a micro problem with an underperforming office submarket. In addition to residential conversions, strategies to address both ends of this regional-to-neighborhood spectrum may include conversions to other uses such as hotels or education.

- Affirmatively furthering fair housing: The Fair Housing Act requires recipients of federal housing funds to “take meaningful actions…that overcome patterns of segregation and foster inclusive communities free from barriers that restrict access to opportunity based on protected characteristics,” including race. In the largest 45 U.S. metro areas, the downtown is the largest job cluster (see Table 1 in this March 2023 report), and most of these jobs do not require a college degree (see Figure 6 in this July 2024 report). Therefore, policy actions that allow workers from protected-characteristic groups to live closer to these opportunities are affirmatively furthering fair housing. However, it is not a guarantee that O2R specifically is the most efficient way to achieve this.

Across our case studies, we found that the primary driver of office-to-residential conversion is market demand for more housing, and much of the existing conversion activity has occurred in high-demand markets with little to no local incentivization. For example, in Stamford, conversions are occurring despite what the case study identifies as a generally unfavorable policy and fiscal environment for developers, due to the extent of the pent-up regional demand for housing.

In short, the primary indicator of the potential for a successful office-to-residential conversion is the underlying strength of demand for new residential units and, in particular, a demand for the types of units (high/mid-rise apartments in developed areas of cities with rents in accordance with the cost of creating those units) that are likely to be created through conversion. We also found that in markets where there is strong demand for both multifamily residential and hotels, unique market dynamics and/or policy constraints can tip the scales in favor of one type of conversion over the other. For example, in Houston, offices have been primarily converted to hotels (not housing) in the downtown, as conversions rarely can accommodate in-building parking—a prerequisite amenity for most Houston residents, while hotel guests are accustomed to valet parking.

We also learned that across the full range from strong to weak housing markets, a number of jurisdictions have applied policy and fiscal tools to incentivize conversions. For example, in Pittsburgh, zoning was modified to allow conversion to happen “by-right” (that is, without need for changes in zoning or regulations for each project), an enhanced tax abatement program was enacted, and discretionary public grants have been made available to select conversion projects in the downtown. In general, the tools deployed may be targeted geographically or across the city, and vary widely by jurisdiction.

Understanding the efficacy of these tools rests on both understanding the specific public needs underlying the incentive(s) and then considering the efficiency with which the incentive achieves the goals. So, if a local government determines that the revitalization of an underutilized office corridor is an important policy goal, it is important to understand whether a set of incentives have in fact contributed to that goal, and done so in a way that reflects responsible stewardship of public resources. In general, we saw that in areas with weak demand for downtown living, even a relatively favorable policy and fiscal environment for real estate development failed to spur substantial conversion activity—suggesting some cities may need to make more direct investments if they want to revitalize their urban core.

State and local tools to facilitate office-to-residential conversion

Fundamentally, state and local governments have two interrelated tools at their disposal to encourage O2R conversion activity: 1) easing local processes for converting buildings (e.g., zoning); and 2) promoting the conversion of buildings by spending public money, either through reducing the cost of conversion (e.g., through tax credits) or increasing the value of the resulting building (e.g., through investing in public space downtown).

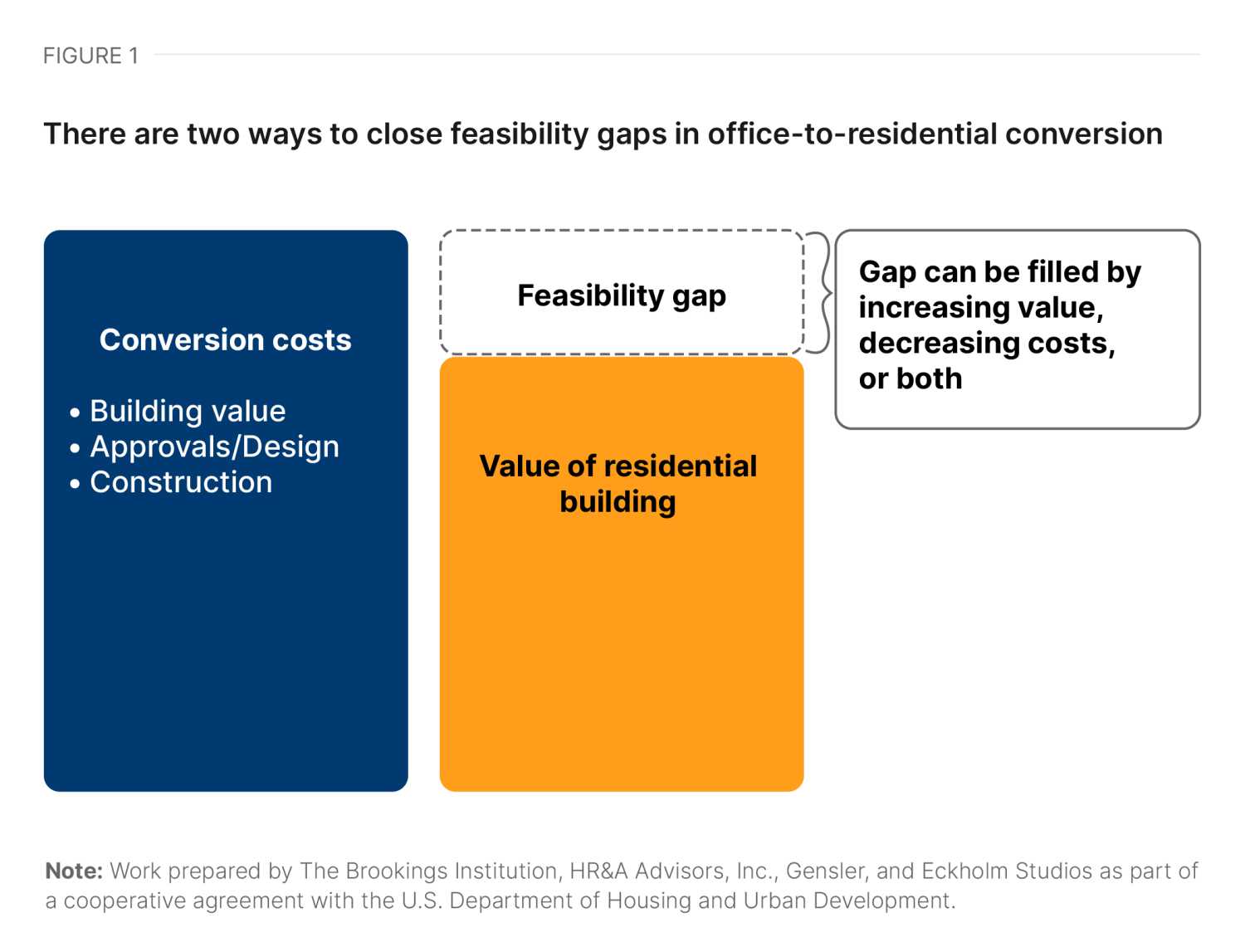

To understand which tools are appropriate in a particular market, it is helpful to consider the “feasibility” gap associated with local office-to-residential conversion (see Figure 1). The feasibility gap is defined as the gap between the cost of production of a housing unit and the value of that unit on the open market (either through rent or sales proceeds). Conceptually, this model is based on the economic premise that when the economic cost of creating a unit is higher than the economic value of the unit on the open market, that unit will not be created through market action alone.

Policy choices

Considering the case studies as a group suggests four different (though potentially complementary) actions taken by various levels of government and philanthropy. In each of the case studies, the approach varied based on local needs, context, and resources.

Across our six case studies, each jurisdiction deployed at least one of the following policy or fiscal tools, calibrated toward closing the feasibility gap for conversion in their market:

- Policy: Process tools. Local governments control the processes that govern what can be built, where, and at what speed through zoning, permitting, and the local building code. The policy environment that governs O2R impacts the speed—and thus costs—at which projects can occur, and ultimately their viability. When considered across six different case studies of six different cities, there is a wide range of approaches to local approvals and regulations for office-to-residential conversions. In some instances, the requirements are few, largely transparent, and available by-right. In other instances, processes can be opaque and uncertain. This variation largely mirrors land use approvals and building code interpretation broadly in the United States, in which local jurisdictions are largely in control of their own land use decisions.

- Financial: Subsidy tools. State and local governments create incentives that aim to reduce the costs associated with the conversion of office buildings to residential use. The states in which our case study cities are located all offer State Historic Tax Credits, which are commonly used in conjunction with Federal Historic Tax Credits on conversion projects. However, the extent of the credit varies by state and city—and many cities have instituted additional financial incentives focused on reducing the cost of conversion, such as low-cost financing or direct subsidies. These tools are often tied to affordability and/or fair wage and local hiring requirements. These incentives often reflect a carefully negotiated expression of public policy that directs public resources toward the conversion of offices into housing, while aiming to ensure that direct benefits accrue to a broader subset of residents in the city than the individual increment or aggregate revitalization effect of the conversion does naturally.

- Financial: Revenue tools. Government can reallocate demand—and therefore increase revenue potential—for specific buildings or places by giving residents a reason to move. For example, the Department of Housing and Urban Development (HUD) subsidizes demand by issuing vouchers for low-income housing. In recent years, some states and cities in need of population have gone a step further, using philanthropic partnerships to offer direct financial incentives for workers to relocate.

- Financial: Value tools. More broadly, state and local government—often also in conjunction with philanthropy—can strengthen demand by investing in neighborhood amenities, thereby increasing the value of the building. In addition to affordability, households make decisions about where to live based on resources such as parks, libraries, schools, transportation, accessibility (to work, to school, to shopping and dining), and countless other personal criteria. Careful decisions about how public resources are allocated across neighborhoods can increase demand in specific housing submarkets. For example, housing near public transportation and parks is frequently more valuable than otherwise comparable housing without such access.

Many cities are in the process of exploring how all four of these approaches can be deployed to catalyze conversion. A policy approach to promoting conversion through easing processes is a low-cost option that often offers ancillary benefits to other pro-development actors. A cost-oriented approach typically benefits office-to-residential conversion projects across a jurisdiction, and thus the aggregate demand for the approach and resulting cost are not known in advance. On the other hand, a revenue-oriented approach that addresses specific known costs often involves picking specific winners and/or areas of geographic focus (and therefore, areas that are left out of incentives or investments).

Finally, considering the value approach, cities are complex organisms, and different people within a city may place a different value on an investment in public infrastructure. Given the subjective nature of the value of an investment, it is difficult to say whether a strategy is “enough” to promote conversion activity. Considering these tradeoffs in cost, who benefits, and certainty can help observers understand why local and state governments may favor one strategy over another.

Translating six case studies to other cities across the nation

Each of the case study cities has seen some conversion activity to date, and in each city, we identified buildings that in both market and physical characteristics appear to be candidates for further conversion activity. These cities represent a range of sizes, market conditions, and regulatory perspectives, and each of the case studies offers important lessons for policymakers and industry participants:

- The most important factor in driving local conversion activity is sustained demand for the types of housing units that conversion can produce within a given housing market area (which could include a city, region, or specific submarket). When demand is high, the market will find ways to meet that demand, and cities that have invested in the types of environments that drive high demand have often seen large numbers of conversions.

- Beyond gaps between the cost to produce units and the value of those units, the largest impediment in many markets is the complexity of the process for approving and executing conversions. In some instances, this obstacle exists in the creation of any new multifamily housing, while in others, the obstacles relate to the special circumstances of conversions. Interviews with developers across multiple cities suggest that greater clarity, certainty, and ease of approvals and regulatory processes would significantly increase the production of new units.

- Programs to reduce the cost of the conversion of buildings have a mixed track record. In areas of weak market demand, it may be impractical to create enough subsidy to produce new units through conversion at a feasible cost. On the other hand, in areas of strong demand, subsidies may be deeper than are strictly necessary.

- The use of subsidies to achieve more targeted policy goals (such as affordable housing or neighborhood stabilization) remains relatively undeveloped in the specific instance of conversion of offices to residences. Local policymakers should carefully consider the overall policy goal, and then evaluate how conversion can best serve the determined goal(s). For example, a subsidy to encourage the use of vacant retail space may actually be more effective at generating demand for residential units in a dilapidated office neighborhood than an incentive to promote the conversion of an individual building.

As local policymakers consider the opportunities associated with office-to-residential conversion, these case studies provide a useful starting place for these discussions. The range of experiences across cities of different sizes and market conditions suggests the need to periodically reflect and adjust the framework of policies and programs as demographic realities and market conditions change.

The federal role

Efforts to promote O2R conversion are largely driven by states and cities. The federal government’s role in promoting O2R conversion is primarily through historic tax credits, which help close capital stack gaps by covering costs. At a cost to the federal government of $44.3 billion since 1977, the program has leveraged $235 billion in private investment to facilitate building conversions of many kinds across urban and rural contexts, and was used for the majority of office-to-residential conversions we studied.

In addition, the federal government does some subsidizing of demand through the provision of tenant and building-based vouchers for low-income renters and through the Low-Income Housing Tax Credit (LIHTC).

Across local public and private sectors, our interview subjects expressed strong interest for the federal government to play a larger role in facilitating building conversions.

Last fall, the White House released a guidebook for a range of programs—federal loans, grants, guarantees, and tax incentives—that owners might be able to use to help make office-to-residential conversion projects pencil. The 21 programs listed were mostly originally developed to promote adjacent societal goals such as transit-oriented development and emissions reductions, but the hope was that some could be creatively repurposed to also support O2R conversion. In practice, there has been limited uptake to date; beyond the federal historic tax credit and LIHTC, none of the projects we studied used federal incentives.

Looking forward, Congress and federal agencies including HUD could better direct federal resources to accelerating conversions. For example, HUD could encourage public housing agencies to provide project-based vouchers for conversion projects. In addition, the Department of Energy and/or Congress could restructure their tax incentives, and the Department of Transportation could streamline the loan programs it offers that may be applicable to conversion projects.

Conclusion and future work

The long-term survival of cities and regions is based in part on their ability to adapt and evolve to changing conditions. The factors that bring people together in places vary widely across geography, time, macroeconomic conditions, culture, and other factors—and so places themselves are constantly changing.

These case studies identify variations in the market conditions and policy ecosystems that produce office-to-residential conversions, which can help eliminate underperforming offices and strengthen specific office submarkets and, ultimately, local tax bases. The case studies provide useful examples of ways in which cities are already beginning to adapt to a shifting environment. However, the bigger question for many cities and the federal government is to what extent O2R conversions can produce housing supply at scale and affirmatively further fair housing.

Additionally, local policymakers will need to consider the extent to which local resources can and should be devoted to using O2R conversions to achieve local policy goals, and how much those incentives might cost. In a future report, we will investigate these questions through the lens of these same six case studies.

Office-to-residential conversion case studies

Authors

Authors listed in alphabetical order

-

Acknowledgements and disclosures

This research was supported by the U.S. Department of Housing and Urban Development under a cooperative agreement.

The authors thank Hanna Love for her review and Kate Collignon and Erman Eruz for their collaboration in the development of this piece. All remaining errors and omissions are those of the authors.

The work that provided the basis for this publication was supported by funding under an award with the U.S. Department of Housing and Urban Development. The substance and findings of the work are dedicated to the public. The author and publisher are solely responsible for the accuracy of the statements and interpretations contained in this publication. Such interpretations do not necessarily reflect the views of the Government.

-

Footnotes

- The landscape of office-to-residential conversion is rapidly evolving in most U.S. cities. The circumstances for each city’s downtown and specific buildings we discuss may have evolved since our analysis concluded on October 1, 2024.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).