This post was updated on May 31, 2024 with a correction to the RRIF L2C percentage for transit-oriented development

The joke goes: Two economists are walking down the street when one of them thinks he sees a $10 bill lying on the ground. He says to the other, “Hey, will you look at that? Ten dollars!” The friend says, “That’s impossible—if that was really a $10 bill, someone would have noticed by now and picked it up.” So they keep walking and leave a perfectly good $10 bill on the ground.

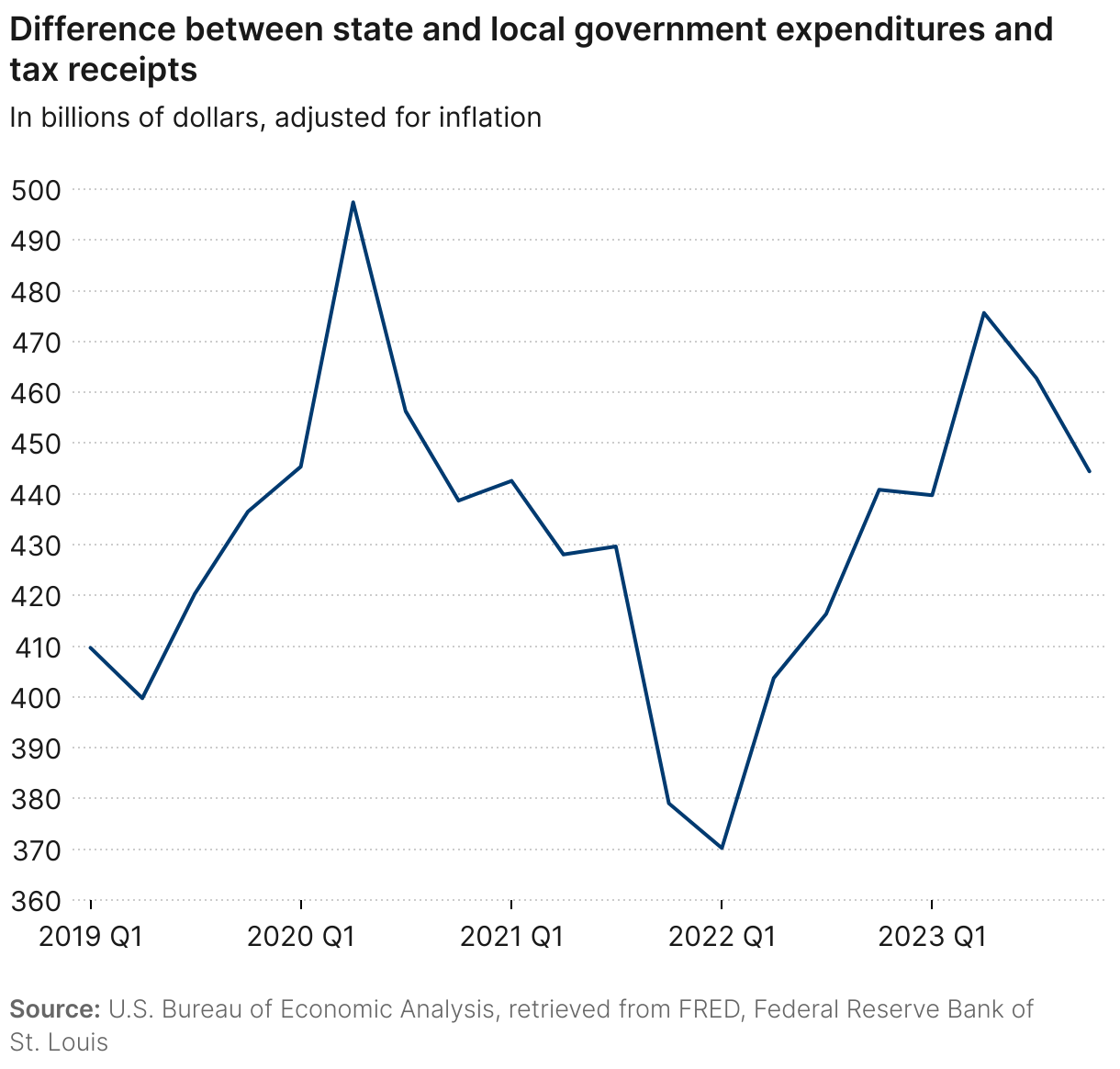

As local governments across the country present their budgets for fiscal year 2025, too many are still walking past $10 bills. The gap between state and local government expenditures and revenues (Figure 1) has been volatile during the COVID-19 period, even compared to historic recessions, and is currently 8% wider than at the beginning of 2019. Most recently, state and local tax revenues are down from a historic peak in Q1 2022, and state revenues declined 13% in real terms in the first three quarters of 2023.

Over the past few years, craters in the tax revenue road have been smoothed by transfers from the federal government via the American Rescue Plan Act (ARPA). However, according to Brookings’ Local Government ARPA Investment Tracker, nearly 88% of that money has been budgeted as of this spring. With ARPA funds drying up, local leaders are now confronting the fact that expenditures remain high as some cities face declining commercial property tax revenues, and states are not well positioned to help. It’s time to take a second look at what’s already on the ground.

On Wednesday, May 1, local, state, and federal leaders gathered at Brookings to unpack that metaphor by “Putting public assets to work through innovative finance.”

State and local governments own a lot of valuable real estate. For example, 14% of land in Boston is owned by the city itself. Diving deeper, a 2022 land audit found that the city of Boston owns 9.5 million square feet, or roughly 218 acres, of underutilized land. For context, the massive Boston Seaport master planned project is on only 33 acres. A similar review in Salt Lake County identified county-owned parcels near existing transit stations, which could yield a potential $13.5 billion in transit-oriented development.

Since the publication of “The Public Wealth of Cities” in 2017, more localities are realizing they can leverage underperforming public assets to generate value for their communities. Imagine a city with salt for snow removal stored on what was initially cheap land—but decades later, that same parcel is worth millions of dollars and is taking up precious acreage in a high-cost neighborhood with a critical lack of affordable housing. Or a surface parking lot and rundown library long past its expected life with no funding to repair or replace it, next to a transit line in a fast-growing neighborhood—a chance to rebuild a public asset and new housing, including affordable units.

At the May 1 event, we heard from three local governments that want to do more with the assets they own. Too often, governments don’t have a comprehensive view of what they have. Within department silos, the government staff responsible for any one asset have a full set of duties and are not responsible for asking if their asset could have a higher and better use. Furthermore, such staff understandably lack the expertise to negotiate a complicated public-private partnership, and can’t access the right types of capital to make a project feasible. Private sector parties pass over these prime public asset opportunities because working with government too often means higher predevelopment risks and, as a result, higher costs.

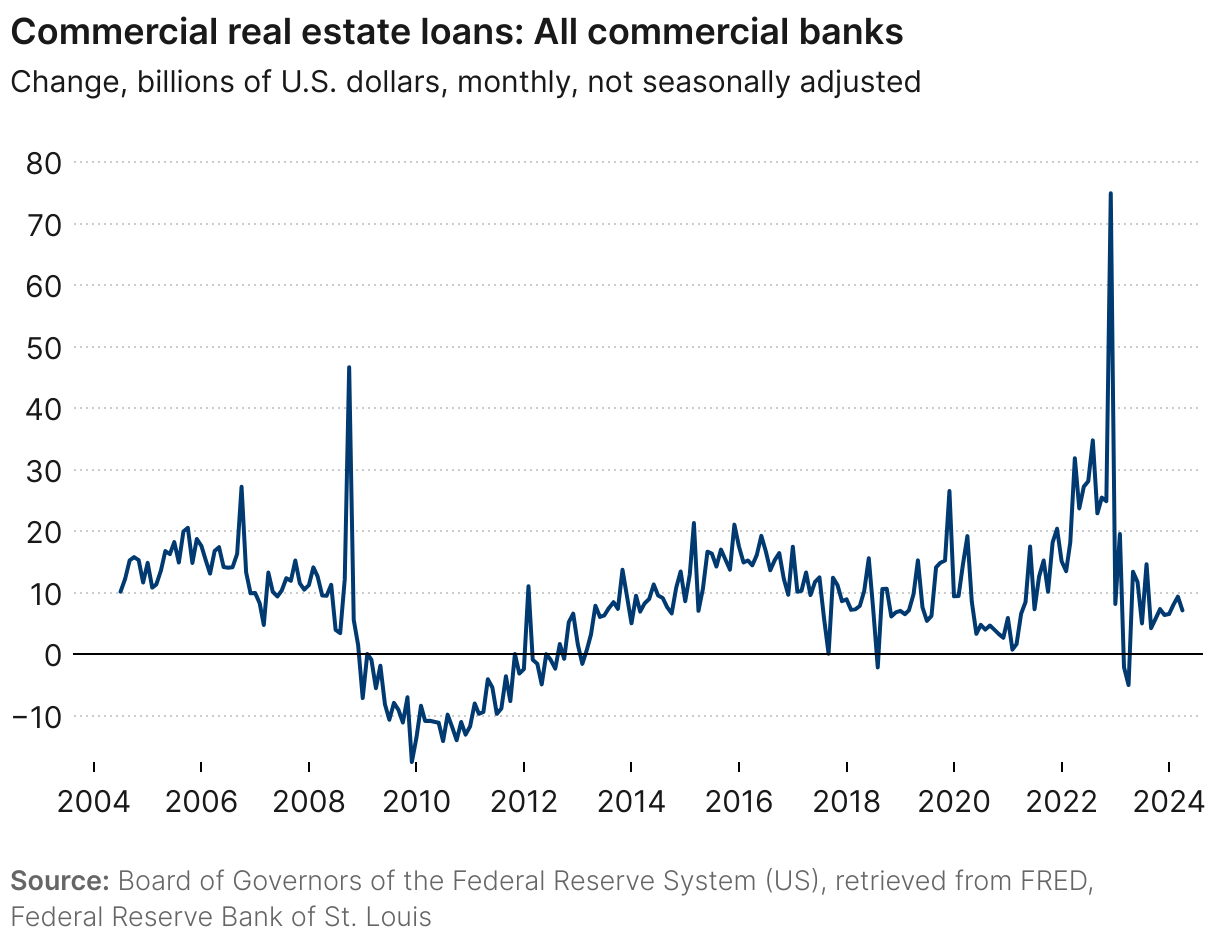

We believe circumstances justify a closer look at public assets and private partnerships. The current climate is one of a high cost of capital (interest rates) and new lack of capital liquidity, as shown in Figure 2, where commercial real estate lending has tightened since March 2023. This means many commercial real estate projects are infeasible. The timing couldn’t be worse for a commercial real estate sector engulfed in major disruption and requiring a significant capital outlay to evolve.

Thus, the time is now for cities—on their own or with the help of the federal government—to empower themselves with information; create the capacity and power to move with deliberate speed to place site control of key parcels in the development domain; establish new partnerships that capture more of the upside of putting assets to work for public benefit; and unlock financing.

Addressing local government’s limitations

The Government Finance Officers Association’s Putting Assets to Work (PAW) initiative has identified core informational, organizational, strategic, and capacity barriers to doing more with public land.

First, local governments don’t even know what they have. For three years, the PAW initiative has helped local governments inventory and map all of the assets they own—parking lots, underutilized office buildings, residential property, bits of right of way, and so forth—so that they can determine the value of these holdings and decide which may be ripe for redevelopment. Most cities don’t know their own balance sheets. They know how much they spend in their annual operating budget, but they often lack a real understanding of what they own and what it’s worth.

There are other barriers as well. Many local governments administratively separate housing and transportation departments, making collaboration between them inefficient and challenging. When traffic congestion means commute times are too long, many metro areas respond by widening roadways or expanding mass transit, but another response could be to more strategically locate housing closer to existing jobs. Similarly, a mayor may prioritize an economic development approach focused on luring the biggest employers possible; this requires cities to offer enormous plots of inexpensive, developable land that may be far from city centers and public transit. Moreover, most local governments suffer from a chronic lack of capacity.

Amid the many constituent demands on staff time, public servants find themselves justifiably focused on core responsibilities such as public safety, economic development, parks and recreation programs, or the challenges of individuals experiencing homelessness—without the capacity to envision and strategically manage a portfolio of real estate assets to maximize long-term benefits to the municipal balance sheet. It is not realistic to think that this reality will suddenly change—if we scope the problem as fixing local government, then assets will be left fallow instead of put to work. Instead, what if the next generation of mission-driven public-private partnerships enabled agile local action in new ways?

In other words, even the firmest nudges (a struggling office cluster, a crumbling school, a flailing transit system) and the juiciest bait (a revitalized downtown, new public amenities, revenue growth) cannot get local governments that are at their limit trying to deliver the core basics to do more without new capacity. Local governments need help, new models, and startup capital.

The case of transit-oriented development

Underdeveloped land near transit infrastructure is a classic example of an asset that could and should be put to work. Provisions of the Infrastructure Investment and Jobs Act (IIJA) make available new tools to address the traditional barriers for putting these assets to work.

The U.S. Department of Transportation (DOT) has over $100 billion ready for deployment at very low interest rates through the Transportation Infrastructure Finance and Innovation Act (TIFIA) and Railroad Rehabilitation and Improvement Financing (RRIF) program. These programs traditionally have helped fund major transportation projects, such as constructing roads, bridges, and tracks. The IIJA contains reforms intended to make it easier for transit-oriented development to leverage TIFIA and RRIF as well. This means TIFIA and RRIF funds can also be used to finance real estate development on publicly owned parcels near public transit, which helps maximize the productivity of fixed transportation assets. Local leaders who want to strengthen the tax base, make real progress toward carbon reduction, or reach their affordable housing goals can use these dollars to build in neighborhoods where density is or could be high, jobs are prevalent, low-cost transportation is convenient, and market demand is strong.

At the May 1 event, Morteza Farajian, executive director of the DOT’s Build America Bureau, announced a major milestone in federal transportation history: The first-ever TIFIA loan for a transit-oriented development project has closed. The deal provides a low-interest loan up to $26.8 million for the Mt. Vernon Library Commons Project in Washington state. The project includes a multiuse building with a public library, community center, meeting rooms, commercial kitchen, parking garage, public restrooms, STEM center, computing space, and electric vehicle chargers. The project, slated to be completed this summer, encompasses half a city block in downtown Mount Vernon, and will be a short walk from Skagit Station, Skagit County’s multimodal transportation center.

There are good reasons why it has taken until 2024 for this deal to happen, even with below-market interest rates on offer. Statutory and regulatory changes and clarifications are needed to make this resource more accessible:

- Because TIFIA and RRIF were originally intended for transit, rail, and roadway projects, there remains a requirement that projects undergo a review for environmental impact. That doesn’t make sense for infill real estate development. Projects are likely eligible for a categorical exclusion under the National Environmental Policy Act (NEPA), but it’s a time-consuming, bureaucratic headache for public-private investments that succeed or fail based on the time it takes for a project to go from conception to occupancy and stabilization.

- TIFIA and RRIF borrowers are required to have an investment grade rating in order to receive a loan. That’s unrealistic for a tool intended to encourage transit-oriented real estate development. Rating agencies don’t typically even rate the debt for these types of projects. Applicants have found some workarounds, but it’s another instance in which the tool needs an update to work better for this new use.

- Similarly, “Buy America” requirements that are impactful and make sense for billion- or trillion-dollar infrastructure projects are unnecessary deal-killers on smaller-scale real estate projects. An administrative waiver to speed up the more pressing policy priority of building housing near transit makes sense.

- Congress should consider increasing the maximum loan-to-cost (L2C) threshold for TIFIA from 49% to match the RRIF program, which allows loans up to 75% L2C for transit-oriented development and 100% L2C for public infrastructure. This would reduce the burden on local governments to find gap financing from other sources, which for some projects will make the difference between feasibility and impossibility. It is also more consistent with typical real estate practice, in which most real estate developments borrow 60% to 70% of their project costs from commercial lenders and secure the remaining 30% to 40% from private equity (at a much higher cost).

- Finally, the development of model documents—including a pro forma financial model—for transit-oriented development projects could provide more clarity than any number of webinars, workshops, or pages of guidance.

As the Build America Bureau implements the IIJA, more work is needed to refocus and accelerate local governments’ use of TIFIA—if not understand their assets better outright. Because of the other barriers to putting assets to work, just throwing money at the problem will not magically unclog a pipeline of transit-oriented development. Notably, the Build America Bureau recently published a notice of available funding for its Innovative Finance and Asset Concession Grant Program—$100 million that will be available over the next five years to fund a scan of public assets and some pre-development expenses for cities that want to pursue TIFIA funding. Critically, cities can use these resources to bring in private sector expertise.

Conclusion

The current fiscal picture for state and local governments in a context of high interest rates and limited commercial real estate lending is grim. Putting assets to work is a critical part of meeting the challenge. Moving assets into productive use generates tax revenue that many local governments need. And this is not just a short-term need—housing density near transit is a way for a community to reduce its carbon output even as it absorbs greater numbers of people.

The benefits to local government don’t stop there. The Innovative Finance and Asset Concession Grant Program seeks to give ambitious and forward-thinking local leaders the project capacity they may currently lack. Can this prove the concept and lead to new kinds of partnerships, more dynamic and innovative thinking across a range of service areas, and more transit-oriented development? As these projects compel otherwise disparate departments and agencies to collaborate, perhaps new efficiencies, opportunities, and ways of doing business can be unlocked even after TIFIA-funded projects are delivered.

In this scenario, the $10 bill is not only more visible—more people will be racing to pick it up and put it to use.

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How local governments can put their assets to work

May 30, 2024