China’s upcoming 14th Five Year Plan is likely to emphasize investments in digitalization to promote the country’s competitiveness in the new general-purpose technologies expected to drive economic progress during the next decade. In this blog, inspired by a recent paper by Indermit Gill, Wolfgang Fengler, and Kenan Karakulah and utilizing the perspectives of our colleague Anwar Aridi, we look at the consequences of accelerated digital development on social and economic outcomes, an issue that has not received enough attention in China.

Europe 4.0, a new World Bank report on Europe‘s digital transformation published this week offers a point of reference. The report develops a framework to assess Europe’s competitive position and the impact of digitalization on economic competitiveness, market inclusion, and regional convergence. We apply the same framework to China and argue that China’s strengths so far are in technologies that are mostly good for inclusion and convergence. But the focus of China’s policymakers is on areas that are likely to worsen inequality. This should of concern because China’s social welfare system is much less well prepared than Europe’s.

The Europe 4.0 framework distinguishes between the effects on competitiveness, inclusion, and spatial concentration of the three types of technologies that constitute the digital economy:

- Transactional technologies such as e-commerce platforms and global networks, which lower information asymmetries and provide digital infrastructure to improve the matching of market supply and demand.

- Informational technologies such as cloud computing, big data analytics, business management software and artificial intelligence (AI), which leverage the falling costs of computing power, improving access to digital infrastructure and exponential growth of data to offer new services.

- Operational technologies such as smart robots, 3D printing and the Internet of Things (IoT), which lower the costs of production by integrating data with industrial equipment.

Transactional technologies are likely to improve market inclusion and regional convergence as they lower barriers to entry of new businesses, increase transparency of prices, and improve geographic access. There is emerging evidence that the development of e-commerce is associated with higher employment, faster growth in incomes, increased entrepreneurship, reduced migration outflows, higher gender equity, and reduced poverty.

Informational technologies also have a positive impact on market inclusion as they lower costs of access to new business technologies (such as “software as a service,” SaaS) or cloud computing, and help level the playing field between large and small companies. That said, information technologies may decrease geographic convergence as firms in the less developed regions lack the critical management skills, human capital, and infrastructure to access new services.

Finally, operational technologies, such as smart robots or AI-managed machines, often call for significant upfront investments, high levels of skills and management practices, and a well-developed infrastructure, which tends to favor large firms and more economically advanced regions. As a result, operational technologies may harm both market inclusion and regional convergence. A growing number of research studies (including here, here, and here) argue that over the past decades automatization and robotization have contributed to the falling labor share in GDP, increasing inequality, and the hollowing out of middle-class occupations and incomes.

How does China score?

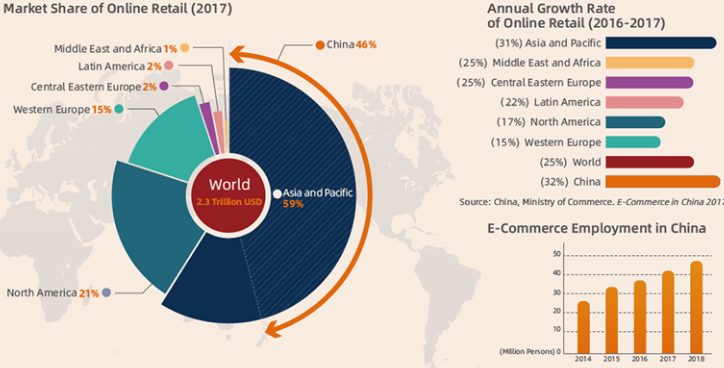

China is one of the global leaders in transactional technologies thanks to the large size of its internet platforms, wide use of e-commerce, and top-notch logistical infrastructure (in China, packages purchased online are usually delivered with 24 hours). In 2018, jobs related to e-commerce represented more than 5 percent of total employment. China also has by far the largest online market in the world, which in 2017 represented almost half of the world’s total online retail sales (Figure 1). Growth in e-commerce seems to have also contributed to stronger market inclusion and geographic convergence, as illustrated by the success of Alibaba’s Taobao Villages. AliResearch, Alibaba’s internal think tank, estimates that over a 12-month period until June 2019, Taobao villages helped create almost 7 million jobs in rural areas and generated more than 700 billion renminbi or more than $100 billion in total sales. E-commerce in Taobao villages is associated with higher wages and greater participation of women, and was a critical source of income in rural areas during the COVID-19 lockdown in early 2020.

Figure 1. China has the largest and the fastest growing e-commerce market in the world

Source: World Bank, 2019

China also does well on informational technologies, but restrictions on the use of data limit the country’s potential. China has already built a significant capacity in data centers and AI processing capacity and has become the world’s second largest market in cloud computing. China stores about one-fifth of the world’s data and—given its leadership in data collection technologies—its share in global data, the new “oil” of the world’s economy, is likely to continue to increase. However, China’s restrictive regulations on data flows and localization of data (which needs to be stored entirely within the country) and underdeveloped data standards impede China from turning its technological advantages into the desired competitive edge internationally. One way forward for China would be to adopt data protection standards modeled on the European Union’s data protection regulatory framework. The draft Personal Information Protection Law makes progress in this direction but remains significantly less specific than the European standard. China should also consider removing restrictions on data flows and localization.

China’s achievements in transactional and informational technologies are largely thanks to its private entrepreneurs. Public services are only beginning to leverage the benefits of digitalization, hampered by gaps in the integration of public databases such as those for social assistance, pollution control, or surveillance of infectious diseases. Addressing these gaps could spread the benefits more widely. To do this, China has to invest more in human capital, especially in rural areas that considerably lag their coastal peers, remove restrictions on market access in the service sector and further improve the investment climate, and improve the protection of intellectual property rights, including by replicating recent business environment reforms from Beijing and Shanghai across the rest of China. China’s anti-monopoly regulations will need to be updated to address the risk of emerging network monopolies.

Related Books

China’s biggest weakness today is in operational technologies such as smart robots, 3D printing, and IoT-connected equipment, where China is still largely dependent on inputs from Europe and the United States. China’s future productivity growth, especially in manufacturing, will need to rely increasingly on operational technologies and its leaders are consequently focused on closing the gap. However, this will likely lead to a greater concentration of value-added production in the more advanced coastal regions and deepen the productivity gap between the leading and the lagging firms within the same sector, which is already larger than in developed economies. As a result, the large urban-rural inequalities in incomes and the quality of life may increase even more. China needs to reinvigorate efforts to diffuse digital technologies from the market leaders to the laggards, accelerate labor market reforms (by further reforming the hukou system for example), and beef up China’s welfare system, which is far behind its global peers as well as Europe and the United States. China spends only about 1 percent of GDP on social assistance compared with the 8 percent average for the OECD countries.

China is well-positioned in informational technologies, thanks to the strengths of its internet platforms and the size of its domestic data pool. Greater transparency would help leverage these advantages for public service delivery. The convergence toward Europe’s data protection standard and improved protection of intellectual property rights would turn them into assets for global competitiveness. China’s concerted efforts to develop domestic capabilities in operational technologies are likely to reduce the remaining gap with Europe and the U.S. in the coming years. But if China wants to ensure the resulting digital dividends are widely shared, it will need to prioritize both market-oriented reforms to accelerate the diffusion of technologies and social welfare reforms to protect its workers from the labor market impacts of digitalization.

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

China 4.0: Sharing the dividends of digitalization

November 10, 2020