Editor’s Note: As the economies of the U.S. and China both struggle under the global recession, what is the future of the U.S.-China economic relationship and how will both countries respond to invigorate economic growth? In testimony to the U.S.-China Economic and Security Review Commission, Wing Thye Woo details challenges for both economies and proposes effective policy responses.

Watch video of the testimony » (Woo’s discussion begins at 2:00:00 minutes)

The unexpected depth and global nature of the current recession

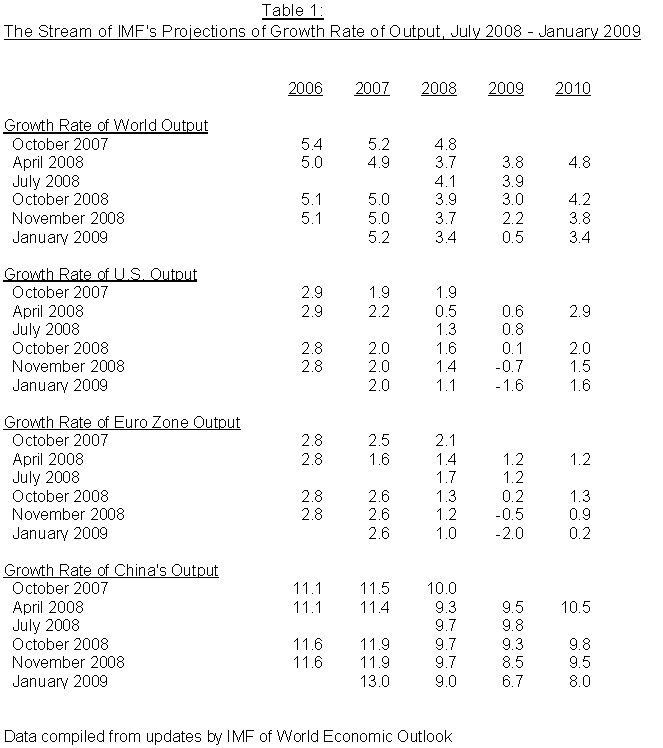

China’s economic situation in 2009 does not look good. The 9.0 percent GDP growth rate in 2008 was not representative of the annualized quarter-to-quarter (q-o-q) growth rate of 2.6 percent in the fourth quarter of 2008. Despite Premier Wen Jiabao’s prediction in Davos at the end of January 2009 that China’s growth would be 8 percent in 2009, the IMF’s January 2009 projection was 6.7 percent, which was down from its November 2008 projection of 8.5 percent. The February 2009 estimate of the number of jobs lost by migrant workers was 20 million, which was double the estimate of December 2008; and an additional 6 to 7 million rural residents were expected to join the migrant work force. The factory-gate price index fell 3.3 percent in January 2009 and is expected to fall 6.3 percent in February 2009. The pace of China’s growth slowdown has consistently exceeded the expectations of the Chinese government and most outside analysts.

The dramatic drop in level of economic activity in China is also seen across the world; the q-o-q growth rate in 2009:4Q was -12.7 percent in Japan; -3.8 percent in the U.S.; -2.1 percent in Germany; 1.8 percent in Italy; -1.5 percent in UK; and -1.5 percent in the Euro Zone. The overall growth in 2009 has been forecasted to be -2.3 percent for the U.S.; -3.4 percent for Japan; -2.7 percent for the Euro Zone (Citigroup, January 22, 2009); and 0.5 percent for the World Output (IMF, January 28, 2009). The unanticipated nature of the decline in China is also shared by other countries, as evidenced in Table 1 by the IMF’s continual downward revision of its projected 2009 growth rates for different countries, e.g. the Euro Zone growth rate in 2009 was expected to be 1.2 percent in the July 2008 projection but -2.2 percent in the January 2009 projection.

What caused the output decline in China and elsewhere?

A sizzling growth of 13 percent was produced for the 17th Congress of the Communist Party of China (CPC) in October 2007, which consolidated the political leadership of President Hu Jintao. It was therefore to be expected that inflation fighting became the primary policy focus and economic technocrats switched from accommodative enforcement to rigid enforcement of the credit quotas that every bank was subject to, and initiated a faster rate of yuan appreciation. The q-o-q GDP growth rate went from 10.8 percent in the fourth quarter of 2007 to 7.3 percent in the first quarter or 2008; 11.8 in the second quarter of 2008 and 6.2 percent in the third quarter of 2008. The slowdown in the first three quarters of 2009 is attributable primarily to macroeconomic and exchange rate policies and other domestic factors because there was no sign of a slowdown in export growth in the first three quarters of 2008, and the year-to-year (y-o-y) export growth rate in October was 19 percent which was consistent the monthly growth rates in the second and third quarters of 2008.

Then export growth (y-o-y) plunged to -2.2 percent in 2008:11M; -2.8 percent in 2008:12M; and -17.5 percent in 2009:1M (while the yuan-dollar exchange rate was unchanged). The precipitous drop (y-o-y) in industrial production from the double digit level in January-September (11.4 percent in 2008:9M) to 8.2 percent in 2008:10M, 5.4 percent in 2008:11M, and 5.7 percent in 2008:12M, and the large jump in unemployment of migrant workers was no doubt the consequences of the negative shock from China’s export market. In short, China’s present economic crisis resulted from a policy-induced slowdown that has been greatly exacerbated by an unexpectedly deep economic collapse in US, EU, and Japan.

The deepening US recession is caused by the generalised credit crunch generated by the implosion of the US financial system that was initiated by the bursting of the housing bubble in 6 which led to the subprime mortgage market melting down in 2007. The housing bubble was only the most prominent feature of a more generalized overvaluation of financial assets. This “irrational exuberance” displayed by investors produced by a number of interacting factors: the choice of CPI (and not a price index that included asset prices) not as the paramount guide to guide monetary policymaking, the Panglossian attitude of the economics profession that asset markets are most rational in its use of information (the “efficient markets” hypothesis), negligence by the financial regulatory bodies (e.g. the blind eye toward reports about the Madoff Ponzi scheme), inadequate supervision of new financial instruments (e.g. subprime mortgage bonds), and the complicity of the rating agencies in understating risks.

The front page report in The New York Times of December 26, 2008, “Dollar Shift: Chinese Pockets Filled as Americans’ Emptied”, reported that the claim by some analysts that the US housing bubble was able to continue only because China prevented the long term interest rate from rising by continually investing its large trade surpluses into Freddie Mac and Fannie Mae bonds. I reject this claim that the flow of Chinese financial opiate through its chronic trade surpluses is a cause of the US financial crisis that is significant enough to be ranked together with erroneous money target, faulty bond rating, incompetent financial oversight, and complacency toward financial innovations. Pogo’s verdict of “We Have Met The Enemy and He Is Us” is a more convincing explanation.

For someone who believes that the US financial crisis cannot be solved without staunching the intravenous flow of Chinese financial opiate through the trade channel, he will have to insist that the $787 billion stimulus package of the US Treasury, the expanded financial lifelines of the Federal Reserve, and the reorganization of the Securities and Exchange Commission will not work until the Obama administration also implements one of the following two proposals that have floating around in Washington for some a number of years: impose a 27.5 percent tariff on all imports from China, and force China to appreciate the yuan by 40 percent. (A first step to implementing either measure is to declare China guilty of currency manipulation.)

However, even if Pogo is wrong (i.e. I am wrong in rejecting Chinese trade imbalances as a necessary factor in causing the US financial crisis), I believe that starting a trade war in the middle of a global recession will worsen, not improve, the prospects for economic recovery in the US.

China’s dilemma: short-run political expediency versus long-term economic efficiency

In November 2008, China announced a two-year stimulus package of 4 trillion yuan ($586 billion), which is about 7 percent of GDP per year. It is clear that China will increase the stimulus when necessary. My opinion is that, unless the global economy weakens significantly, China’s growth in 2009 is likely to lie closer to Premier Wen’s 8 percent target than to the IMF’s projection of 6.7 percent, say, 7.5 percent in 2009 and 2010. The state-owned banks (SOBs) will be happy to obey the command to increase lending because they cannot now be held responsible for future nonperforming loans. The local governments and the state-owned enterprises (SOEs) can now satisfy more of their voracious hunger for investment motivated by the soft-budget constraint situation where the profits would be privatized and the losses socialized. The stimulus package will work very well because of the collusion between the managers of the SOBs and SOEs to transfer public assets to themselves.

Also, under the cover of economic emergency, the local governments will now ignore the recently-strengthened laws on environmental protection, worker safety, and medical insurance in order to encourage investment. The price of the 7.5 percent growth in the midst of a global recession will be paid later by the recapitalization of the SOBs and a more depleted natural environment.

The challenges to generating high sustainable growth in China

China’s economy has been like a speeding car for almost 30 years. The high-probability failures that could cause the car to crash in the near future could be classified under three categories (1) hardware failure, (2) software failure, and (3) power supply failure; see Woo (2007).

A hardware failure refers to the breakdown of an economic mechanism, a development that is analogous to the collapse of the chassis of the car. Probable hardware failures are (1) a banking crisis that causes a credit crunch that, in turn, dislocates production economy-wide, and (2) a budget crisis that necessitates reductions in important infrastructure and social expenditure (and also possibly generates high inflation, and balance of payments difficulties as well).

A software failure refers to a flaw in governance that creates frequent widespread social disorders that disrupt production economy-wide and discourage private investment. This situation is similar to a car crash that resulted from a fight among the people inside the speeding car. Software failures could come from (1) the present high-growth strategy creating so much inequality, and corruption that, in turn, generates severe social unrest which dislocates economic activities; and (2) the state not being responsive enough to rising social expectations, hence causing social disorder.

A power supply failure refers to the economy being stopped because it hits either a natural limit or an externally-imposed limit, a situation that is akin to the car running out of gas or having its ignition key pulled out by an outsider. Examples of power supply failures are (1) an environmental collapse, e.g. climate change; and (2) a collapse in China’s exports because of a trade war

The Chinese leadership is moderately confident that it could prevent and respond appropriately to most hardware failures because it knows that the technical solutions can be learned quite quickly from previous hardware failures in other countries. As long the technocrats are well-educated and the politicians are relatively non-ideological, stealing with one’s eyes is an effective strategy to handling hardware failures.

A good clue as to what the most likely precipitating factors are is found in the discussions of the 6th Plenum of the 16th Central Committee of the Communist Party of China (CPC) that concluded on October 11, 2006. The 6th Plenum passed a resolution to commit the CPC to establish a Harmonious Society by 2020. The proposed harmonious socialist society would encompass a democratic society under the rule of law; a society based on equality and justice; and a society in which humans live in harmony with nature. The obvious implication from this commitment is that the present major social, economic and political trends within China might not lead to a harmonious society or, at least, not lead to a harmonious society fast enough. The difficulty is that software failures and power supply failures are harder for the leadership to handle because their solutions are politically more difficult, often rely on the cooperation of other countries, and require scientific knowledge that is not yet developed.

The need to improve governance to prevent software failures in China

China’s strategy of incremental reform combined with the fact that institution building is a time-consuming process meant that many of its regulatory institutions are either absent or ineffective. The most well-known recent regulatory failures occur in the food and pharmaceutical sectors, e.g. misuse of chemicals to lower production costs has resulted in the addition of poisonous substitutes into toothpaste, cough medicine, and animal feed; the application of lead paint to children toys; and the over-employment of antifungals and antibacterials in fish farming. There have also been significant regulatory failures in the protection of labor, e.g. wage arrears and forced labor of kidnapped children in the brick kilns of Shanxi and Henan provinces.

Inadequate institutions of governance are not the only cause of social tensions in China, however. The present economic development strategy, despite its ability to generate high growth, also generates high social tensions because, in the last ten years, it has had great difficulties in reducing extreme poverty further and in improving significantly the rural-urban income distribution and the regional income distribution. In the 1999-2005 period, the proportion of rural population receiving an income of $0.50 a day actually increased from 1.9 percent in 1998 to 2.8 percent in 2005. In a recent study, the Asian Development Bank that China is probably the most unequal country in Asia today, with a Gini coefficient of 0.473 in 2004 and the combined income of the richest 20 percent being 11.4 times the combined income of the poorest 20 percent.

Doing more of the same economic policies today will not produce the same salubrious results generated in the early phases of economic reform because the development problems have changed. In the first phase of economic development, the provision of more jobs was enough to lower poverty significantly. At the present, many of the poor people need an infusion of assistance (e.g. empowering them with human capital through education and health interventions) first in order to be able to take up the job opportunities. The weakening of China’s trickling-down mechanism does not bode well for future social stability.

The incidence of public disorder, labeled “social incidents,” has risen steadily from 8,700 in 1993 to 32,500 in 1999 and then to 74,000 in 2004; with the average number of persons in a mass incident rising from 8 in 1993 to 50 in 2004. Clearly, the number of mass incidents would have been lower if China had better governance. There would have been more pre-emptive efforts at conflict mediation by the government, more programs to increase human capital formation in the rural areas, and less abuse of power by government officials if the government’s actions had been monitored closely by an independent mechanism, and the government had also been held more accountable for its performance.

The experiences from the developed countries show that three elements are important in improving governance: democratic institutions, a free press, and an independent judiciary. The challenge to preventing a software failure in China is whether the CPC could rise to the demands of the Harmonious Society objectives and transform itself into a social democratic party.

China’s present development strategy is environmentally unsustainable

The present mode of economic development has given China the dirtiest air in the world, is polluting more and more of the water resources, and, is, possibly, changing the climate pattern within China. The reality is that CPC’s new objective of living in harmony with nature is not a choice because the Maoist adage of “man conquering nature” is just as unrealistic as creating prosperity through central planning.

Water shortage appears to pose the most immediate environmental threat to China’s continued high growth. Presently, China uses 67 to 75 percent of the 800 to 900 billion cubic meters of water available annually, and present trends in water consumption would project the usage rate in 2030 to be 78 to 100 percent. The present water situation is actually already fairly critical because of the uneven distribution of water and the lower than normal rainfall in the past fifteen years. Right now, “[about] 400 of China’s 660 cities face water shortages, with 110 of them severely short.”[1] The extended period of semi-drought in northern China combined with the economic and population growth have caused more and more water to be pumped from the aquifers, leading the water table to drop three to six meters a year.

The desert is expanding (possibly, at an accelerating pace), and man appears to be the chief culprit through over-cultivation, overgrazing, deforestation and poor irrigation practices. One direct upshot is a great increase in the frequency of major sandstorms that play “havoc with aviation in northern China for weeks, cripples high-tech manufacturing and worsens respiratory problems as far downstream as Japan, the Korean peninsula and even the western United States.”[2]

While northern China has been getting drier and experiencing desertification, nature as if in compensation (or in mockery) has been blasting southern China with heavier rains, causing heavy floods which have brought considerable deaths and property damage almost every summer since 1998.[3] The sad possibility is that the northern droughts and southern floods may not be independent events but a combination caused by pollution that originates in China. I will have more to say about this possibility later.

Clearly, without water, growth cannot endure. And in response, the government begun implementation in 2002 of Mao Zedong’s 1952 proposal that three canals be built to bring water from the south to the north: an eastern coastal canal from Jiangsu to Shandong and Tianjin, a central canal from Hubei to Beijing and Tianjin, and a western route from Tibet to the northwestern provinces, and each canal will be over a thousand miles long.[4] Construction of the eastern canal (which would be built upon a part of the existing Grand Canal) started in 2002, and the central canal in 2003. Work on the western canal is scheduled to begin in 2010 upon completion of the first stage of the central canal.

This massive construction project will not only be technically challenging but also extremely sensitive politically and fraught with environmental risks. The central canal will have to tunnel through the foot of the huge dyke that contains the elevated Yellow River, and the western canal will have to transport water through regions susceptible to freezing. The western canal has generated a lively controversy. Some scientists are contending that it “would cause more ecological damage than good”[5] because it “could cause dramatic climate changes … [and] the changed flow and water temperature would lead to a rapid decline in fish and other aquatic species.”[6]

The fact is that water conservation could go a long way toward addressing the water shortage problem because currently a tremendous amount of the water is just wasted, e.g. only 50 percent of China’s industrial water is recycled compared to 80 percent in the industrialized countries,[7] and China consumes 3,860 cubic meters of water to produce $10,000 of GDP compared to the world average of 965 cubic meters.[8] The most important reason for this inefficient use of water lies in the fact that “China’s farmers, factories and householders enjoy some of the cheapest water in the world”[9] even though China’s per capita endowment of water is a quarter of the world average.[10]

There is, however, the unhappy possibility that neither the price mechanism nor the three canals can solve China’s water problem and make its growth sustainable unless the present mode of economic development is drastically amended. There is now persuasive evidence that China’s voluminous emission of black carbon (particles of incompletely combusted carbon) has contributed significantly to the shift to a climate pattern that produces northern droughts and southern floods of increasing intensity.[11] So, until China reduces its emission of black carbon significantly, it means that (a) China’s massive reforestation program will not succeed in reducing sandstorms in the north because trees cannot survive if the amount of rainfall is declining over time; and (b) the number of south-north canals will have to be increased over time in order to meet the demand for water in northern China;

Defusing a power supply failure: tensions created by the exchange rate and trade imbalances

China has been accused exchange rate manipulation that has caused large U.S. trade deficits, which have reduced U.S. welfare by increasing unemployment and reducing wages. In addition, the strong claims by some observers that the prolonged large trade imbalances would sooner or later cause a rocketing of inflation in China almost make it a moral imperative for the United States to use tariffs to force a 40 percent yuan appreciation for China’s own good. The facts are however contrary to the above claims, and the do-gooder instinct is misguided; see Woo (2008).

The alleged negative effects on U.S. labor from the trade imbalances are greatly exaggerated. The average unemployment rate in 1999-06 was 5 percent compared to 6 percent in 1991-1998; and the total compensation (including benefits) for blue-collar workers rose in the 1991-2006 period. In order for the take-home pay of the blue-collar to increase substantially, it is important that the cost of healthcare be brought under control. Beside accelerated globalization, accelerated technological innovation was another important trend in this period. The latter produced large productivity gains that enabled labor income to rise despite the greater competition from imports and immigrant labor. The negative consequence of quickened technological progress is that it has caused more frequent job turnovers, and this has increased the anxiety of US worker greatly because US social safety nets are the least adequate within the OECD. The real source for the anxieties that have given rise to the present U.S. obsession with yuan appreciation is not the large trade imbalances but the large amount of structural adjustment necessitated by the acceleration of economic globalization and of labor-saving technological progress. Dollar depreciation and trade barriers will slow down the process of structural adjustment but will not stop it because the other main driver (quite possibly, the bigger driver) of structural adjustment in the United States is technological progress.

The claim that China’s swelling balance of payments surplus had caused the People’s Bank of China (PBC) to lose some control of credit growth is wrong. Chinese banks face credit quotas, and credit growth could not have stayed high in 2003-2007 without continual upward adjustments of the credit quotas by the PBC. The reason is not technical inability to control money growth but the political reality of factional politics before the CPC congress in October 2007. In other words, even if the Chinese balance of payments surplus had not increased secularly during the 2003-07 period, the PBC would have engineered the observed money growth in this period.

The claim that a 40 percent appreciation of the Renminbi (RMB) against the US$ would reduce the U.S. global trade deficit represents the triumph of hope over experience. When the average Yen-US$ exchange rate fell from 239 in 1985 to 128 in 1988, the U.S. global current account deficit only fell from 2.1 percent to 1.7 percent of GDP because Japanese companies started investing abroad and exported to the U.S. from there. For similar reasons, a large yuan appreciation would succeed in reducing the bilateral US-China trade imbalance but it would not reduce the U.S global trade deficits significantly because the US would now switch its import supplier from China toward other Asian and Latin American countries. The outcome would be a disgruntled China and a US that is not any happier than before. It is instructive to recall that when the U.S. global trade deficit fell only slightly despite the huge Yen appreciation, Japan-bashing continued under a new guise: the additional demand that Japan must remove its “structural impediments” to import.

China’s current account surplus exists because its dysfunctional financial system cannot intermediate the growing savings into investments. The private savings rate is high because China does not have the variety of financial institutions that would, one, pool risks by providing medical insurance, pension insurance, and unemployment insurance; and, two, transform savings into education loans, housing loans, and other types of investment loans. The backward financial system in China has made the private savings rate in China 7.0 to 12.2 percentage points higher than in the U.S.

The optimum solution to reducing the friction in U.S.-China trade relations is a policy package that emphasizes multilateral actions to achieve several important objectives. It is bad economics and bad politics to dwell on adjustment by only one region (China), induce the adjustment by employing only one policy instrument (RMB appreciation), and focus only one policy target (external imbalance).

What should the United States do? Congress should accelerate the reduction in fiscal imbalance; strengthen social safety nets and programs that upgrade the skills of younger workers; and make healthcare insurance coverage independent of individual employers. In addition to improving the TAA program, the establishment of wage insurance is an excellent way to bring U.S. social safety nets more in line with the type of structural adjustments driven by globalization and technological changes. Occupational obsolescence created by the latter should not be accommodated by establishing extensive skill-upgrading programs (e.g. training loans, apprentice stipends) and improving the formal education system especially at the grade school and high school levels.

What should China do? The obvious short-run policy package has three components. First, the appreciation of the yuan appreciation begun in July 2005 should be resumed after the current global crisis is over. Second, state expenditure (e.g. rural infrastructure investments, and rural health programs) should be accentuated to soak up the excess savings, with an emphasis on import-intensive investments (e.g. buying airplanes and sending students abroad).

It is now common to hear calls for China to rebalance its growth path by reducing investment and increasing consumption. This notion of consumption-led growth is an oxymoron because growth requires expansion of production and this cannot be achieved by lowering investment. The correct rebalancing is to increase consumption at the expense of the trade surplus and not at the expense of domestic capital accumulation. A government-induced increase in consumption that lowers investment will maintain full usage of the existing output capacity but it will diminish the expansion of output capacity, causing a lower GDP growth rate and, hence, a slower absorption of China’s surplus labor. Furthermore, China still has a long way to go before its technological level reaches that of the G-7; and technological upgrading requires investing in more modern capital equipment. So a policy that increases consumption and decreases investment is not only a slow-growth policy, it is also a slow technological upgrading policy.

Consumption could be increased without lowering investment by, one, the state providing an integrated health insurance system, a comprehensive pension system, and an extensive scholarship program; and, two, the financial system providing more sophisticated financial products like education and housing loans, and various types of insurance schemes, and stopping its discrimination against private investors. The establishment of a modern financial system requires the appearance and growth of competitive domestic private banks. As China is required by its WTO accession agreement to allow foreign banks to compete against its SOBs on an equal basis by 2007, it would be akin to self-loathing not to allow the formation of truly private banks of domestic origin.

What should the United States and China do collaboratively? A recent survey by the Pew Research Center found that there has been a dramatic decline in support for free trade within the United States and the major developed countries. With the United States weakening in its resolve to protect the multilateral free trade system, it is the time for China to show that it is a responsible stakeholder by joining in the stewardship of the multilateral free trade system, from which it had received immense benefits. With China so far playing a passive role in pushing the Doha Round forward; by default, Brazil and India have assumed the leadership of the developing economies camp in the trade negotiations. According to Susan Schwab, the U.S. Trade Representative, at the G-4 (the United States, the EU, Brazil, and India) meeting in Potsdam in June 2007, Brazil and India retreated from their earlier offers to reduce their manufacturing tariffs in return for cuts in agricultural subsides by the developed economies because of “their fear of growing Chinese imports.”[12] The failed Potsdam talks hurt the many developing economies that were agricultural exporters.

The reality is that Brazil is now attempting to bypass multilateral trade liberalization by entering into FTA negotiations with the EU. A growing number of nations like Brazil “are increasingly wary of a multilateral deal because it would mandate tariff cuts, exposing them more deeply to low-cost competition from China. Instead, they are seeking bilateral deals with rich countries that are tailored to the two parties’ needs.”[13] China and the United States must now work together to provide leadership to prevent the unraveling of multilateral free trade. It is not possible for China to become harmonious society in a non-harmonious world. For its own sake as well as for the world’s, China must help to build a harmonious world, and the existing world powers should not misinterpret this as a power play by China.

The US and China at the G-20 meeting in London: hanging together or hanging separately?

The present global recession certainly makes it clear that large countries like the US and China should focus not just on stabilizing themselves but also on stabilizing the global economic system in order to produce rapid national recovery. China and the US should not only use their fiscal stimulus to stabilize themselves directly (and hence stabilize the rest of the world indirectly), China should also use its large foreign exchange reserves and the US should also use its dollar-creation power to help stabilize other regions directly in order to stabilize themselves indirectly. Both two sets of stabilizing actions should be enacted because they are mutually-reinforcing not mutually exclusive.

At the G-20 meeting in London on April 2, 2009, China and the U.S. should focus the discussion on the global coordination of fiscal stimulus and monetary loosening, global avoidance of beggar-thy-neighbor policies of export promotion and import restrictions, global harmonization of regulation governing financial institutions and accounting practices, and the feasibility of the U.S. Federal Reserve broadening its temporary network of bilateral swap lines to other well-managed emerging economies. An ad hoc Global Financial Crisis Secretariat (GFCS) should be established to undertake global coordination on these matters, and be temporarily housed as an autonomous unit (in the manner of the World Bank) within the office of the UN Secretary-General. Simultaneity in expansionary macroeconomic policies is GFCS’s most important objective because it prevents deterioration in the trade balances from rendering each country’s expansionary policies unsustainable.

China and US should also support the establishment of a GFCS working group on the reform of the IMF: how much to increase its resources to allow it to fight global financial fires, how wide to increase its jurisdiction to authorize it to improve regulation of financial markets, and how radically to restructure its ownership to give it the legitimacy to impose its will on prostrate economies. While an improved IMF is highly desirable, both the US and China should recognize that the better first line of Asian defense against financial contagion would be a greatly enhanced swap facility, the Asian Financial Facility (AFF), because Asia collectively now has enough reserves to fend off unwarranted speculative attacks on a subset of its members. It must be emphasized that the core mission of the AFF is to combat financial contagion and not to finance balance of payments adjustment caused by economic mismanagement.

An AFF is necessary because it is simply impossible (certainly, inefficient) to increase the size of the IMF enough to enable it to have in-depth expertise on most of the countries to be able to respond optimally in a timely manner to each national crisis. Even if the improved technical competence of the IMF is not doomed to disappoint the emerging economies, the emerging economies would be disappointed by the long time required for an improved IMF to appear. The negotiations on meaningful IMF reforms would inevitably be cantankerous and hence protracted.

Right now, East Asia has a thin network of swap lines to defend their currencies. It would be desirable to hasten the evolution of the existing swap facility into the AFF by two actions. First, the existing swap facility specifies that a cumulative drawing that exceeds 20 percent of a country’s quota would require the country to accept IMF supervision. This “flight-to-IMF” clause should be removed because painful memories of 1997-98 make it politically suicidal for any East Asian leader to do so. Second, because the primary purpose of the AFF is to reduce the cost of bad luck and not of bad economic policies, the removal of the “flight-to-IMF” clause requires that the swap facility establish a surveillance mechanism to pre-qualify its members for emergency loans. Without this surveillance mechanism, the Asian Financial Facility would not attain a meaningful size because no member would be willing to risk committing a large part of its reserves to the facility.

Why should the G-20 support a GFCS? The IMF simply lacks legitimacy and credibility in the eyes of East Asia. If need be, the assignment of global financial regulation to an expanded BIS would be a better alternative. The IMF should forgo its dream of jurisdiction-expansion and become instead a more specialized agency that undertakes macroeconomic surveillance for the world, and balance of payments assistance for the emerging economies. The UN is the global organization with the most legitimacy, and its temporary custody of the GFCS would, one, be a good signal by the G-20 of their genuine desire to make multilateralism work; and, two, be a collective statement that it is time for the national allocation of global responsibilities to be reconfigured.

Why should the US support an AFF? The US and the rest of the interested world would be members of the AFF just as they are now influential members of the Asian Development Bank. In dealing with Asia, the US should rely less on the hard power of a formal dominant role in global leadership, and more on the soft power of US example, like helping Asia do what’s best for Asia (which is an excellent start to the US re-engagement with Asia). The AFF would expand over time to be an APEC-level institution; and be a good partner to the IMF because “two heads are better than one” in analyzing unexpected quickly-evolving crises and in preventing their contagion.

The bottom line for the April 2 meeting is that the focus should be on fighting global recession and not on reforming the international financial architecture; and the bottom line for beyond April 2 is that the better way to improve the supply of global public goods is not to simply increase the size of the existing providers but to increase the number of providers while seeking to improve the performance of existing ones. The establishment of the GFSC will enable simultaneous implementation of macroeconomic stimulus, and harmonized regulation of financial markets. The US support for AFF will be a much-needed change toward an inclusive US approach that is diversified in modality to handle each specific multilateral issue. If the G-20 can act decisively on April 2 on these well-defined economic tasks, the world can then have more faith that enlightened self interests will also accomplish the much more arduous task of containing environmental contagion from global climate change.

References

Menon, Surabi, James Hansen, Larissa Nazarenko, and Yunfeng Luo, 2002, “Climate Effects of Black Carbon in China and India,” Science, Vol. 297, 27 September, pp. 2250-2253.

National Development and Reform Commission, 2007, China’s National Climate Change Programme, June.

Woo, Wing Thye, 2007, “The Challenges of Governance Structure, Trade Disputes and Natural Environment to China’s Growth,” Comparative Economic Studies, Volume 40, Issue 4, December, pp. 572-602.

Woo, Wing Thye, 2008, “Understanding the Sources of Friction in U.S.-China Trade Relations: The Exchange Rate Debate Diverts Attention Away from Optimum Adjustment,” Asian Economic Papers, Vol. 7 No. 3, Fall, pp. 65-99.

[1] “China may be left high and dry,” The Straits Times, January 3, 2004.

[2] “Billion of Trees Planted, and Nary a Dent in the Desert,” The New York Times, April 11, 2004

[3] The National Development and Reform Commission (2007) reported: “The regional distribution of precipitation shows that the decrease in annual precipitation was significant in most of northern China, eastern part of the northwest, and northeastern China, averaging 20~40 mm/10a, with decrease in northern China being most severe; while precipitation significantly increased in southern China and southwestern China, averaging 20~60 mm/10a … The frequency and intensity of extreme climate/weather events throughout China have experienced obvious changes during the last 50 years. Drought in northern and northeastern China, and flood in the middle and lower reaches of the Yangtze River and southeastern China have become more severe.”

[4] “Ambitious canal network aims to meet growing needs,” South China Morning Post, November 27, 2002.

[5] “China Water Plan Sows Discord,” Wall Street Journal, October 20, 2006.

[6] “Chinese water plan opens rift between science, state,” American-Statesman, September 10, 2006.

[7] “China may be left high and dry,” The Straits Times, January 3, 2004.

[8] “Alert sounded over looming water shortage,” The Straits Times, June 10, 2004.

[9] “Water wastage will soon leave China high and dry,” South China Morning Post, March 8, 2006.

[10] “Alert sounded over looming water shortage,” The Straits Times, June 10, 2004.

[11] Menon, Hansen, Nazarenko, and Luo (2002).

[12] “Schwab surprised by stance of India and Brazil,” Financial Times, 22 June 2007; and “China’s shadow looms over Doha failure,” Financial Times, 22 June 2007.

[13] “Brazil, Others Push Outside Doha For Trade Pacts,” The Wall Street Journal, 5 July 2007.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

{kind=link}

Commentary

TestimonyChina’s Short-term and Long-term Economic Goals and Prospects

February 17, 2009