This analysis is part of The Leonard D. Schaeffer Initiative for Innovation in Health Policy, which is a partnership between the Center for Health Policy at Brookings and the USC Schaeffer Center for Health Policy & Economics. The Initiative aims to inform the national health care debate with rigorous, evidence-based analysis leading to practical recommendations using the collaborative strengths of USC and Brookings.

One of the core functions of health insurance is to protect people against financial ruin and ensure that they get the care they need if they get seriously ill. To help ensure that insurance plans met that standard, the Affordable Care Act (ACA) required plans to limit enrollees’ annual out-of-pocket spending and barred plans from placing annual or lifetime limits on the total amount of care they would cover.

These protections against catastrophic costs apply to almost all private insurance plans, including the plans held by the roughly 156 million people who get their coverage through an employer. A provision added Thursday night to American Health Care Act (AHCA), the health care legislation currently being debated in the House of Representatives, could jeopardize those protections—not just for people with individual market plans, but also for those with employer coverage.

Specifically, the Thursday’s manager’s amendment would modify the “essential health benefit” standards that govern what types of services must be covered by individual and small group market insurance plans. The intent of the amendment is reportedly to eliminate the federal benefit standards that currently exist and instead allow each state to define its own list of essential health benefits. While some have suggested that the drafting of the amendment makes its actual impact unclear, this blog post examines the consequences if the amendment achieved its reported intent.

Much analysis of potential changes to essential health benefits has focused on the potentially severe consequences that could befall a state’s individual health insurance market in the absence of effective essential health benefit requirements. However, weakening essential health benefit standards could also have important negative consequences for the coverage offered by employers of all sizes because it would weaken the ACA’s guarantee of protection against catastrophic costs. That is because the ACA’s ban on annual and lifetime limits and its requirement that plans limit enrollees’ annual out-of-pocket spending only apply to spending on essential health benefits. Thus, as the definition of essential health benefits narrows, the scope of the ACA’s guarantee of protection against catastrophic costs shrinks as well. In the absence of any essential health benefit standards at all, these protections would effectively disappear because they would apply to an empty set of health benefits.

In practice, the House proposal appears likely to seriously weaken the definition of essential health benefits and thereby seriously weaken the ACA’s guarantee of protection against catastrophic costs

In practice, the House proposal appears likely to seriously weaken the definition of essential health benefits and thereby seriously weaken the ACA’s guarantee of protection against catastrophic costs. In light of the patterns of state benefit regulation that existed prior to the ACA, it appears plausible that many states will set essential health benefit standards that are considerably laxer than those that are in place under the ACA. In addition, large employers may have the option to pick which state’s essential health benefits requirements they wish to abide by for the purposes of these provisions; this would likely have the effect of virtually eliminating the catastrophic protections with respect to large employers since employers could choose to pick whichever state set the laxest standards. The same outcome would be likely to occur for all private insurance policies if insurers were permitted to sell plans across state lines, as the Administration has suggested enacting through separate legislation.

The remainder of this blog post discusses these issues in greater detail.

The Affordable Care Act’s Protections Against Catastrophic Health Care Costs

Health care spending varies widely across individuals. While most of the population faces relatively moderate health costs in any particular year, a minority of the population is seriously ill and faces very large expenses. For example, people in the top one percent of health care spending in 2014 incurred expenses exceeding $100,000 in that year. One of the core purposes of health insurance is to cover those catastrophic expenses, thereby ensuring that seriously ill people can access these services continuing to meet their other financial needs. That protection is financed through the premiums paid by those lucky enough to remain healthy.

The ACA introduced a pair of reforms to help ensure that private insurance plans provided this type of protection against catastrophic costs. Both had significant impacts on plan designs, not just in the individual health insurance market, but also in employer coverage. The first of these reforms was a requirement that plans limit enrollees’ annual out-of-pocket spending on essential health benefits. This provision took effect in 2014 and applies to almost all private insurance policies, whether offered on the individual market or through an employer.[1] For 2017, the out-of-pocket maximum can be no more than $7,150 for single coverage and no more than $14,300 for family coverage.

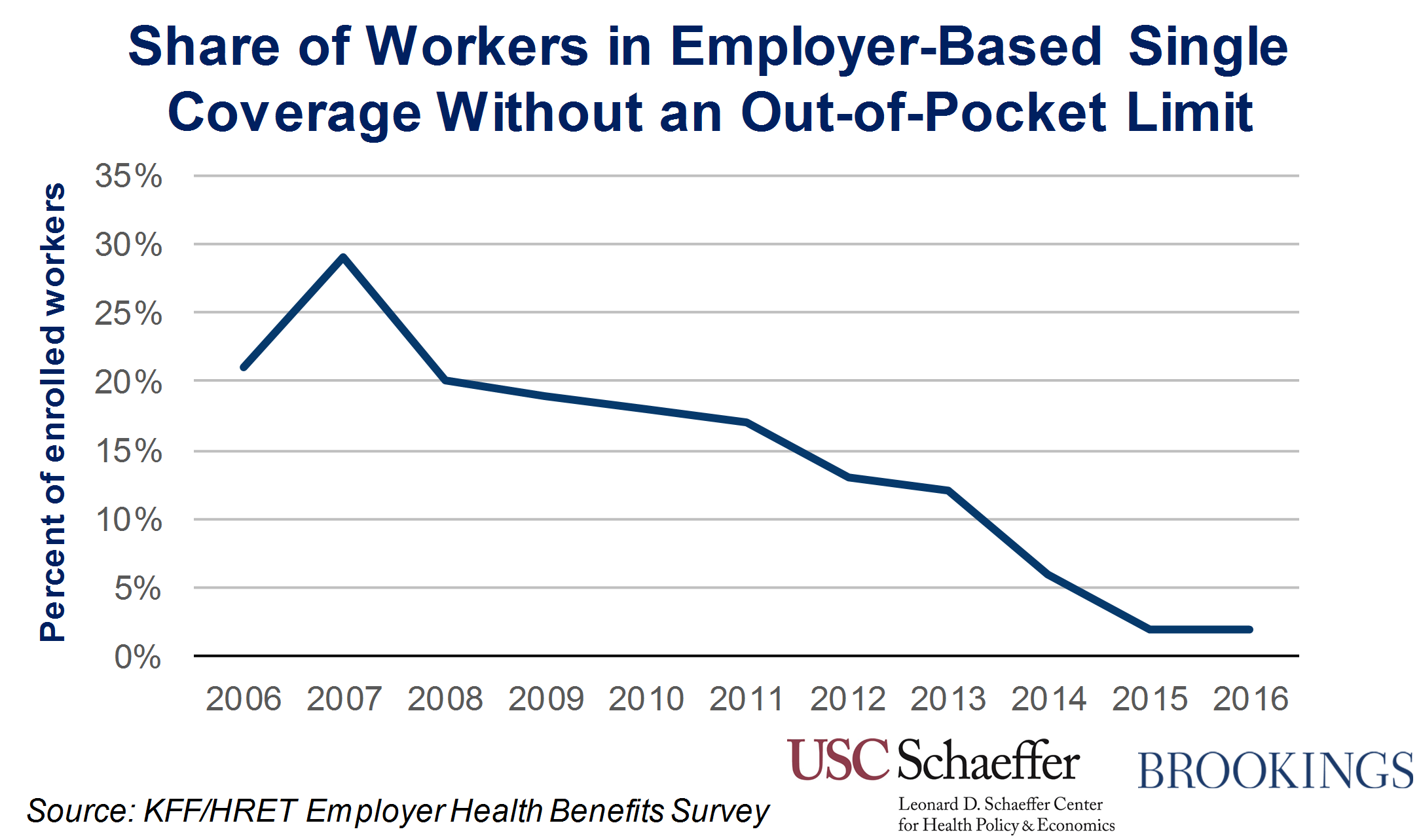

Since the ACA became law, the share of people in employer-based single coverage whose plans lack a limit on out-of-pocket spending has fallen precipitously, from 18 percent in 2010 to just 2 percent in 2016, according to the Kaiser Family Foundation and Health Research and Education Trust’s Employer Health Benefits Survey. The sharp decline in 2014 is likely primarily attributable to the new requirement, and much of the pre-2014 decline likely reflects efforts by insurers and employers to prepare for the beginning of the requirement in 2014. On the basis of these data, the Council of Economic Advisers estimated in December that 22 million more people with employer coverage had out-of-pocket limits in 2016 than if the prevalence of out-of-pocket limits had stayed at its 2010 level.[2]

The second set of reforms was a bar on insurers imposing annual or lifetime limits on the amount of essential health benefits they cover. This provision also applied to almost all private insurance plans.[3] Such limits were typically set at relatively high levels, so the probability of reaching those limits was very small. However, people who were unlucky enough to do so faced financial ruin.

My Brookings colleagues Loren Adler and Paul Ginsburg recently reviewed evidence on the prevalence of lifetime limits in employer coverage before enactment of the ACA. A majority of employer plans appears to have included such limits, with data from the Employer Health Benefits Survey indicating that 59 percent of enrollees in employer coverage were in plans that featured a lifetime limit in 2009. Using these data, Adler and Ginsburg estimated that 109 million people with private health insurance would have a lifetime limit today without this provision of the ACA. Their analysis also provides estimates of the number of people who would have lifetime limits in each state today but for that provision.

Data on the prevalence of annual limits is more limited. However, in regulations implementing the ACA’s annual limit requirements, the Departments of Treasury, Health and Human Services, and Labor reported estimates from a survey by the benefits consultancy firm Mercer. That survey found that around 8 percent of individuals enrolled in plans offered by large employers had annual limits, and around 14 percent of individuals enrolled in plans offered by smaller employer had annual limits.

The Link Between the ACA’s Protections Against Catastrophic Costs and Essential Health Benefits

It may seem surprising that changes to essential health benefits could have important effects on plans offered by employers, particularly large employers. Indeed, the most prominent function of the essential health benefits standards is to define what services individual and small group policies must cover. That role is particularly important in the individual health insurance market. As many analysts have noted, without those requirements, insurers would likely decline to cover categories of care needed by sicker enrollees (or charge a very high premium for such coverage). As a result, the only available plans would either offer very skimpy coverage or have very high premiums.

Related Books

However, the essential health benefits standards also play an important role in defining the scope of the ACA’s protections against catastrophic costs. Specifically, the out-of-pocket limit requirement applies only to cost sharing “with respect to essential health benefits covered under the plan”; plans are not required to cap out-of-pocket spending for services that are not essential health benefits. Similarly, the annual and lifetime limit requirements do not apply to “covered benefits that are not essential health benefits.”[4]

As a result, if the definition of essential health benefits shrinks, the scope of the spending that is eligible for these protections shrinks as well. Indeed, if the essential health benefits standards were eliminated entirely, then these protections against catastrophic costs would become literally meaningless since no spending would be subject to the protections. To take a concrete example, suppose that a state modified essential health benefits requirements so that maternity care was no longer an essential health benefit. Plans could then require an enrollee to pay an unlimited amount out-of-pocket toward the cost of a delivery. Plans could also limit the total amount of delivery-related costs they would cover in any year or over a person’s lifetime.

Likely Consequences of the Essential Health Benefits Changes in the House Bill

The manager’s amendment filed Thursday night is reportedly intended to eliminate the ACA’s federal essential health benefit requirements and instead allow each state to determine its own essential health benefits package. As noted previously, some have suggested that the drafting of the amendment makes its actual effect unclear. The discussion below proceeds under the assumption that the effect of the provision will in fact match the reported intent. Under this assumption, the degree to which this provision would affect the ACA’s protections against catastrophic costs depends on a few key factors.

The first factor is how states use their authority to determine essential health benefits. In states that set few or no standards, the out-of-pocket limit and annual and lifetime limit requirements would, for the reasons described above, become essentially meaningless. In states that maintained relatively stringent standards, there might be comparatively little effect on the integrity of the protections against catastrophic costs, although this would depend on the other considerations discussed below.

Experience from before the ACA implies that, in practice, many states would set standards much weaker than the existing federal standard. Prior to implementation of the ACA’s essential health benefit standards, an estimated 62 percent of individual market enrollees lacked coverage for maternity services, 34 percent lacked coverage for substance abuse services, 18 percent lacked coverage for mental health services, and 9 percent lacked prescription drug coverage. Consistent with the view that many states would set weak standards, the Congressional Budget Office has indicated that, in scoring this type of proposal, it would likely assume that regulatory approaches would “vary widely from state to state” and that “some states might not impose any regulations” on benefit designs.

The second factor is how employers that that offer large group and self-insured plans would be treated under this new regime. Current rules implicitly allow these employers to adopt the definition of essential health benefits that applies in any state they choose when determining their obligations with respect to the out-of-pocket limit requirement and the ban on annual and lifetime limits. If this approach were continued under this new regime, which seems plausible, then the catastrophic protections would be governed by the definition of essential health benefits in the states with the laxest standards, at least for large employers. In this case, the provision in the House bill would render the catastrophic protections essentially meaningless, at least as they apply to plans offered by large employers.

A final consideration is whether insurers might ultimately be permitted to sell plans across state lines, as the Administration has supported in the past. In that case, it is likely that employers of all sizes would be permitted to apply the essential health benefits standards that existed in the states with the laxest standards for the purposes of determining the scope of the ACA’s protections against catastrophic costs. As above, the consequence would be the complete or near complete elimination of the ACA’s protections against catastrophic health care costs. (While not the focus of this piece, allowing insurance across state lines would also magnify the consequences of devolving essential health benefits to the states for the individual health insurance market. As in the employer context, allowing sales across state lines would mean that the standards of the state with the laxest standards would end up applying nationwide.)

Conclusion

The ACA’s requirement that plans limit enrollees’ annual out-of-pocket spending and its ban on annual and lifetime limits have meaningfully improved the degree of financial protection offered by private insurance policies, including those offered by employers of all sizes. Because these protections only apply to services that are considered essential health benefits, the House’s proposal to devolve responsibility for defining essential health benefits to the states would have major implications for these protections.

For the reasons discussed above, there is strong reason to believe that, in practice, the definition of essential health benefits that applied to the catastrophic protections would be far weaker under the House proposal than under current law, seriously undermining these protections. These potential adverse effects on people with employer coverage, in addition to the potentially damaging effects of such changes on the individual health insurance market, are thus an important reason that policymakers should be wary of the House proposal with respect to essential health benefits.

[1] The exception is grandfathered health plans, which are exempt from this requirement. The number of such plans is steadily dwindling over time.

[2] I was Chief Economist at the Council of Economic Advisers at the time this estimate was prepared.

[3] The exception is grandfathered individual market policies, which are exempt from the annual limit requirements, but not the lifetime limit requirements.[4] As noted above, unlike individual market and small group plans, self-insured and large employer plans are not required to cover the essential health benefits package, although they typically do cover most such services. For these large employers, the out-of-pocket limit and annual and lifetime limit requirements only apply with respect to the essential health benefits that are actually covered by the plan.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

New changes to essential benefits in GOP health bill could jeopardize protections against catastrophic costs, even for people with job-based coverage

March 24, 2017