This analysis is part of The Leonard D. Schaeffer Initiative for Innovation in Health Policy, which is a partnership between the Center for Health Policy at Brookings and the USC Schaeffer Center for Health Policy & Economics. The Initiative aims to inform the national health care debate with rigorous, evidence-based analysis leading to practical recommendations using the collaborative strengths of USC and Brookings.

The Centers for Medicare and Medicaid Services (CMS) recently published final data on the number of people who used HealthCare.gov to sign up for health insurance coverage through the Affordable Care Act’s (ACA) Marketplaces during the 2017 open enrollment period. These data support two important conclusions about the state of the Marketplaces and their near-term future.

First, comparing enrollment changes across states implies that Marketplace premium increases had little if any impact on Marketplace sign-ups, providing strong evidence against claims that these increases would send the individual market into a “death spiral.” Although there was a small decline in Marketplace sign-ups relative to 2016 open enrollment, it appears to reflect factors other than higher premiums, possibly including uncertainty caused by the ongoing legislative debate over the ACA and the new Administration’s decision to curtail outreach activities.

Second, while the small decline in sign-ups will have negative consequences for the people who would otherwise have been insured, the impact on the individual market risk pool will likely be minor. It therefore remains likely that insurers’ individual market business will return to a roughly break-even or slightly profitable position in 2017, absent other policy changes.

Final sign-up data show premium increases had little or no impact on HealthCare.gov enrollment

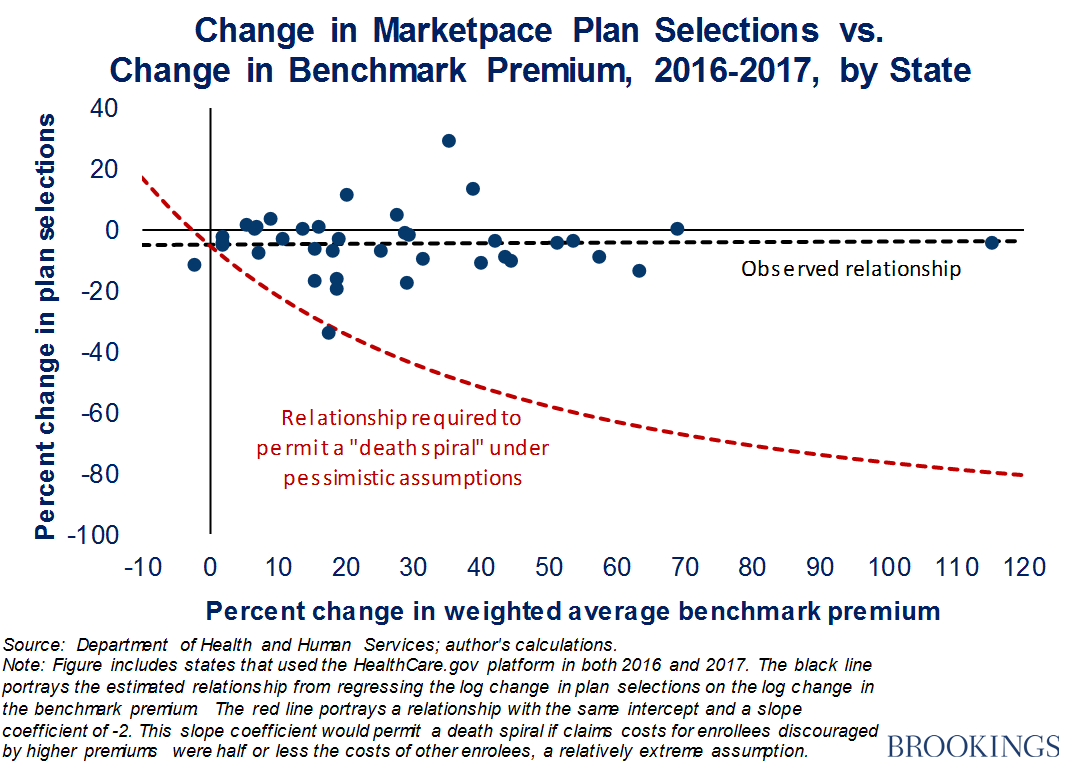

The run-up to this year’s open enrollment season saw widespread predictions that higher premiums for individual market coverage—the Department of Health and Human Services estimated that the premium for the “benchmark” Marketplace plan would rise by 22 percent on average for 2017—would lead to large declines in individual market enrollment.[1] Some analysts speculated that enrollment losses would be so large and so skewed toward healthier individuals that individual market claims costs would rise dramatically, triggering a “death spiral” of further premium increases and enrollment declines that would culminate in the collapse of the individual market.

However, data on final HealthCare.gov sign-ups provide strong evidence that premium increases did not cause dramatic enrollment declines, much less spark a death spiral. The chart plots the percent change in the number of people signing up for Marketplace coverage during open enrollment against the percent change in the weighted average benchmark premium for each state using HealthCare.gov. As shown by the black dashed line, there was essentially no relationship between premium changes and sign-up changes, which implies that premium changes had little or no effect on sign-ups. By contrast, for the individual market to have faced a death spiral, premium increases would have needed to cause large reductions in enrollment, akin to the relationship depicted by the red dashed line. (This analysis updates an analysis published by President Obama’s Council of Economic Advisers [CEA] in early January. I served as CEA’s Chief Economist until the middle of January.)

While these data do not capture changes in individual market enrollment outside the Marketplace, data for the individual market as a whole are likely to paint a broadly similar picture when they become available. Off-Marketplace enrollees would generally be expected to respond to higher premiums in much the same way as on-Marketplace enrollees who are ineligible for the premium tax credit. The complete lack of a relationship between premiums and Marketplace enrollment indicates that any effect of higher premiums on the enrollment decisions of unsubsidized Marketplace enrollees must have been relatively small.[2] Furthermore, off-Marketplace enrollment only accounts for around one-third of enrollment ACA-compliant plans, so any response that does exist would apply to a comparatively small portion of the market, limiting the implications for the market as a whole.[3]

As argued in detail in the CEA analysis cited above, it was predictable that premium changes would have only a limited impact on individual market enrollment based on information that was available at the outset of the 2017 open enrollment period. The ACA’s design and pre-ACA research on consumer behavior provided one basis for such a prediction. Around two-thirds of individual market enrollees are eligible for tax credits that rise dollar-for-dollar when premiums in their area rise, which insulates them against the effects of higher premiums. And for enrollees who are not eligible for tax credits, pre-ACA research on how consumers’ insurance enrollment decisions depend on premiums implied that enrollment would decline only modestly when premiums rose. Similarly, the observed relationship between premium changes and enrollment growth during the ACA’s first few years also implied that any adverse effects of premium increases on enrollment—whether on the Marketplace or in the individual market as a whole—would be limited.

Related Content

The finding that premium changes had little effect on HealthCare.gov sign-ups also implies that factors other than premiums are responsible for the slight decline in sign-ups from 2016 to 2017. While fully analyzing other potential factors is beyond the scope of this piece, some observers have suggested that the Trump administration’s decision to curtail advertising and other outreach activities, as well as its decision to signal that it might weaken enforcement of the individual mandate, reduced enrollment during the final weeks of open enrollment. Consumer confusion or discouragement spurred by the ongoing ACA repeal debate could also plausibly have weighed on enrollment.

The fact that Marketplace sign-ups were running roughly in line with their 2016 pace as of the middle of January provides suggestive evidence that the decline in sign-ups was somehow related to the beginning of the new Administration. In addition, final data from several states that operate their own Marketplaces suggest that they may have seen stronger enrollment performance than the HealthCare.gov states, with either meaningful increases or smaller decreases in enrollment relative to 2016. Since State-Based Marketplaces (SBMs) oversee their own outreach activities, if SBMs as a whole did see stronger enrollment, this would support the view that the Trump administration’s steps to curtail outreach to consumers depressed enrollment.

Lower enrollment will harm the lost enrollees, but only slightly damage the risk pool

Whatever the underlying cause of the slight decline in HealthCare.gov sign-ups relative to 2016, it will undoubtedly have negative consequences for the individuals who would otherwise have had health insurance coverage during 2017. There is strong evidence that having health insurance improves access to care, financial security, and health and well-being – benefits that these individuals will no longer receive. But the enrollment decline will likely have only minor effects on the individual market risk pool and therefore create only a slight headwind to insurers’ efforts to stem their recent individual market losses.

Related Books

The extent to which lower enrollment will affect the individual market risk pool depends upon how the claims costs of the lost enrollees compare to the claims costs of the remaining enrollees. Prior evidence on the relationship between enrollment growth and claims costs permits some educated guesses about this comparison. For example, the relationship between growth in enrollment in the ACA-compliant individual market from 2014-2015 and growth in per member per month claims implies that claims costs for incremental enrollees were about 85 percent of those for incumbent enrollees.[4] A similar calculation based on estimates from research examining implementation of Massachusetts health reform, the closest historical precedent for the reforms implemented in the ACA, implies that costs for incremental enrollees were around 73 percent of those for incumbent enrollees.[5]

Applying these estimates in this context implies that the 5 percent decline in HealthCare.gov sign-ups from 2016-2017 will translate into a roughly 1 percent increase in individual market claims costs, assuming the same enrollment decline is replicated throughout these states’ individual markets.[6] For comparison, the premium increases implemented for 2017, together with other steps taken by insurers and the Obama administration, appear to have put insurers on track to improve their individual market margins by 10- 15 percent of premiums in 2017, on average, after accounting for normal medical trend and the final step in the phasedown of the ACA’s transitional reinsurance program.[7] The additional upward cost pressure from slightly lower enrollment in 2017, while unfortunate and potentially avoidable, will only slightly set back that progress. Indeed, the CEA analysis concluded that individual market premiums were on track to reach a roughly sustainable level in 2017. That conclusion remains reasonable in light of these data.

Of course, policy changes by Congress or the Administration could cause much more serious damage to the individual health insurance market and the health care system as a whole. The Congressional Budget Office estimated that the partial ACA repeal legislation being considered by Congress would cause coverage losses of 18 million in 2018 and 32 million by 2026 and that the accompanying deterioration in the individual market risk pool would increase individual market premiums by 20-25 percent in 2018 and around 100 percent by 2026. An analysis of this legislation by Linda Blumberg, Matthew Buettgens, and John Holahan of the Urban Institute reached similar conclusions. Steps by the Administration to weaken enforcement of the individual mandate or curtail consumer outreach efforts for the entirety of next year’s open enrollment (rather than just the final few weeks, as was the case this year) could also have significant negative consequences for individual market enrollment, the risk pool, and premiums.

[1] The “benchmark” premium is the premium for the second-lowest-cost plan in the silver coverage tier. This premium is the basis for determining the size of the premium tax credit to which an individual is entitled.

[2] It is not possible to estimate the effect of higher premiums on the enrollment decisions of unsubsidized Marketplace enrollees using the same approach used to estimate the effect of higher premiums on overall Marketplace enrollment. When premiums rise, some enrollees who were previously ineligible for the premium tax credit become eligible, so the number of unsubsidized Marketplace enrollees will decline even if no enrollee drops coverage. As a result, the correlation between changes in premiums and changes in unsubsidized Marketplace enrollment will overstate—potentially substantially—the actual effect of premiums increases on enrollment for this group. Notwithstanding this caveat, unreported analysis using data through late December shows only a moderate negative correlation between changes in premiums and changes in unsubsidized enrollment, bolstering the case that the true enrollment response among this group was relatively small.

[3] CMS’ reports for the reinsurance and risk adjustment program imply that enrollment in ACA-compliant policies averaged around 13.7 million during 2015. CMS’ quarterly effectuated enrollment reports imply that effectuated Marketplace enrollment averaged around 9.6 million during 2015, 70 percent of total ACA-compliant enrollment. This fraction is unlikely to have changed substantially since 2015.

[4] This calculation uses data collected for the ACA’s transitional reinsurance program and published by the Centers for Medicare and Medicaid Services. Using these data, I ran a state-level regression of the log change in per member per month claims on the log change in total member months. The slope coefficient from this regression was -0.15. If that regression reflects a causal relationship, then one plus the slope coefficient (the 85 percent figure reported in the main text) corresponds to the claims cost of marginal enrollees relative to inframarginal enrollees.

[5] Hackmann, Kolstad, and Kowalski (2015) report that Massachusetts health reform caused a 32.0 log point change in individual market enrollment and a corresponding 8.7 log point reduction in average individual market claims costs. These estimates imply that the slope of a log-log relationship between enrollment and claims costs would be -0.27; as in the preceding footnote, one plus this amount (the 73 percent figure reported in the main text) corresponds to the claims cost of marginal enrollees relative to inframarginal enrollees.

[6] The 5 percent only includes states that used the HealthCare.gov platform for both 2016 and 2017.

[7] As noted above, the average benchmark premium is estimated to have increased by an average of 22 percent nationwide for 2017. The corresponding increase in premium revenue will be partially offset by the final step in the phasedown of the ACA’s transitional reinsurance program, which the CEA analysis suggested would withdraw support equivalent to around 7 percent of premiums, and the normal increase in medical costs, which would be expected to amount to around 4 percent of premiums. Together, this implies a net improvement in insurers’ margins of around 11 percent of premium revenue, before considering any effects of steps by insurers to shift toward lower-cost plan designs and reduce administrative expenses or regulatory improvements implemented by the Obama Administration for 2017. The CEA analysis provides a longer discussion of these additional potential sources of improvement in insurer margins.

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

New data on sign-ups through the ACA’s marketplaces should lay “death spiral” claims to rest

February 8, 2017