Studies in this week’s Hutchins Roundup find that banks responded to the tightening of regulations after the financial crisis by reducing the supply of credit, many Americans would agree to delay claiming Social Security benefits if offered a lump-sum payment, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Banks respond to stricter supervision by reducing their supply of credit

Bank stress tests and supervisory guidance have been used by U.S supervisors in the past five years to inhibit excessive risk taking or prevent excessive growth in large banks’ credit risk exposure. Paul Calem of the Philadelphia Fed and Ricardo Correa and Seung Jung Lee of the Federal Reserve Board find that these two instruments have reduced the supply of credit. In particular, the 2011 stress test reduced the share of jumbo mortgage originations and approval rates at stress-tested banks. In addition, the 2014 supervisory guidance – written communication from the banking regulatory agencies on safe and sound operation – reduced bank lending to corporations with poor credit.

Many Americans would agree to delay Social Security benefits in exchange for a lump-sum payment

At present, Social Security benefits are provided as a lifelong benefit stream as early as age 62 or can be delayed up to age 70. Although waiting is often the economically wiser alternative, today fewer than 2 percent of recipients wait till age 70. Raimond Maurer of Goethe University Frankfurt and Olivia Mitchell of the University of Pennsylvania find in a survey of Americans between ages 50 and 70 that if offered a lump sum of $60,000 for delaying their benefits and not required to work, the number of people who would defer taking benefits climbs by 20 percentage points, compared to the status quo. If they were offered the same lump sum for delaying but were also required to work part-time, the number of people who would delay raises by about 9 percentage points.

Roughly three quarters of growth comes from innovation by incumbent firms, not start-ups.

Using data on all non-farm US businesses during 1976–1986 and 2003–2013, Daniel Garcia-Macia of the IMF, Chang-Tai Hsieh of the University of Chicago, and Peter Klenow of Stanford conclude that most of the total productivity growth has been from incumbent firms rather than from new entrants. They also show that most growth comes from quality improvements rather than from the introduction of new products. Incumbents’ improvements to their own products loom larger than improvements to incumbents’ products by other firms, a process known as creative destruction. Firms improving on existing products made by other firms contribute just about a quarter of growth, with the remainder mostly due to own innovation by incumbent firms, they find.

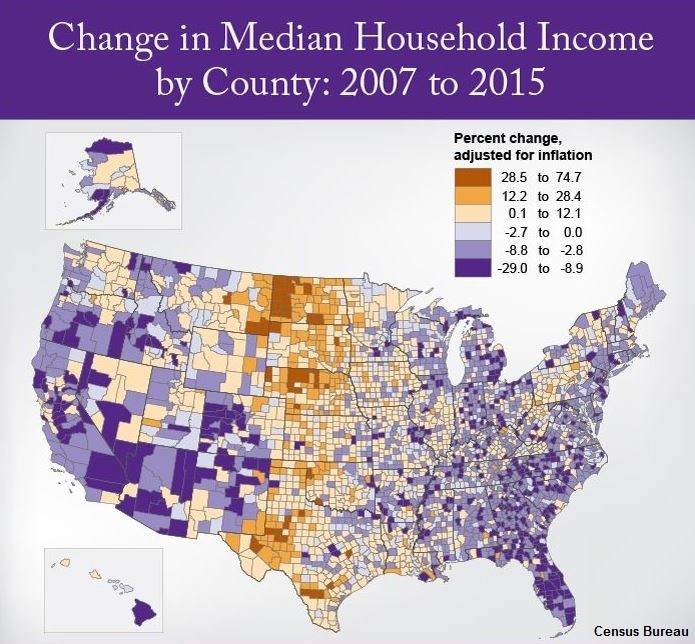

Chart of the week: Recent declines in the median household income were concentrated in the East and West

Quote of the week: “[I]t is … no secret that I’m quite skeptical with regard to Eurosystem government bond purchases,” says President of the Deutsche Bundesbank Jens Weidmann.

“Although such purchases aren’t prohibited per se and they can loosen the monetary policy stance, they are blurring the boundaries between monetary and fiscal policy. And this is especially problematic in a currency union with a single monetary policy and largely autonomous economic and fiscal policies. Euro-area central banks are now the largest creditors of their member states. All governments ultimately pay the same interest rate on the debt in central banks’ balance sheets, regardless of the country’s creditworthiness. Currently, as the Eurosystem’s deposit rate is negative, they all receive money for that part of their debt. What’s more: the larger the part of the debt that central banks withdraw from the market, the less markets will exert their disciplining forces sanctioning unhealthy public finances with higher risk-premia. This is all the more worrisome as the low-interest-rate environment offers few incentives for governments to consolidate their budgets. Fiscal policy in the euro area has been loosened again noticeably over the past few years. What governments are saving in interest payments isn’t being put towards the urgent goal of reducing debt, but instead is being spent to a significant extent. Germany is no exception here, by the way. Of course, this is not only due to diminished market discipline, but also to a lack of rigor in applying the fiscal rules… This fiscal environment could lead to a situation where monetary policy comes under political pressure to make high levels of debt sustainable through low interest rates. This, however, could put price stability at risk. I fear that the danger of fiscal policy becoming too comfortable with the current low-interest-rate environment increases with the time these favorable financing conditions exist.”

Related Content

Related Books

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Bank supervision, Social Security, and more

December 21, 2016