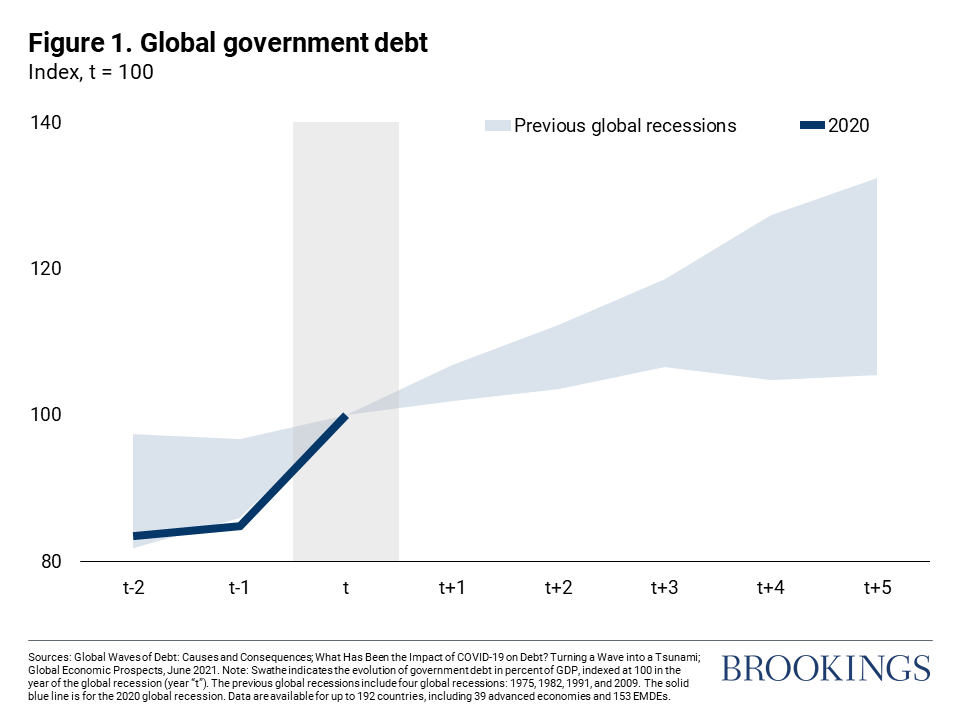

Global government debt surged to nearly 100 percent of GDP during the global recession of 2020, as the COVID-19 pandemic triggered a collapse in output and governments provided unprecedented fiscal support. As the global economy recovers and fiscal support is withdrawn, a key question is whether government debt (relative to GDP) will stabilize and start to decrease. In a new study, we answer this question by analyzing the evolution of government debt after previous recessions.

Government debt: often increases after global recessions

Historically, global government debt has increased after every global recession over the past six decades. Between 1960 and 2019, there were four global recessions: 1975, 1982, 1991, and 2009. Global government debt rose by a cumulative 4-15 percentage points of GDP over the five years following these global recessions—by 4 percentage points of GDP over 1975-80, 15 percentage points over 1982-87, 9 percentage points over 1991-96, and 4 percentage points over 2009-14 (Figure 1).

Government debt also tended to be higher after recessions in a majority of countries. On average, in the five years after a global recession, two-thirds of countries had the same or higher debt levels. A slightly larger share of advanced economies saw higher levels of debt after recessions than emerging market and developing economies (EMDEs), while around three-quarters of low-income countries (LICs) had higher debt after recessions.

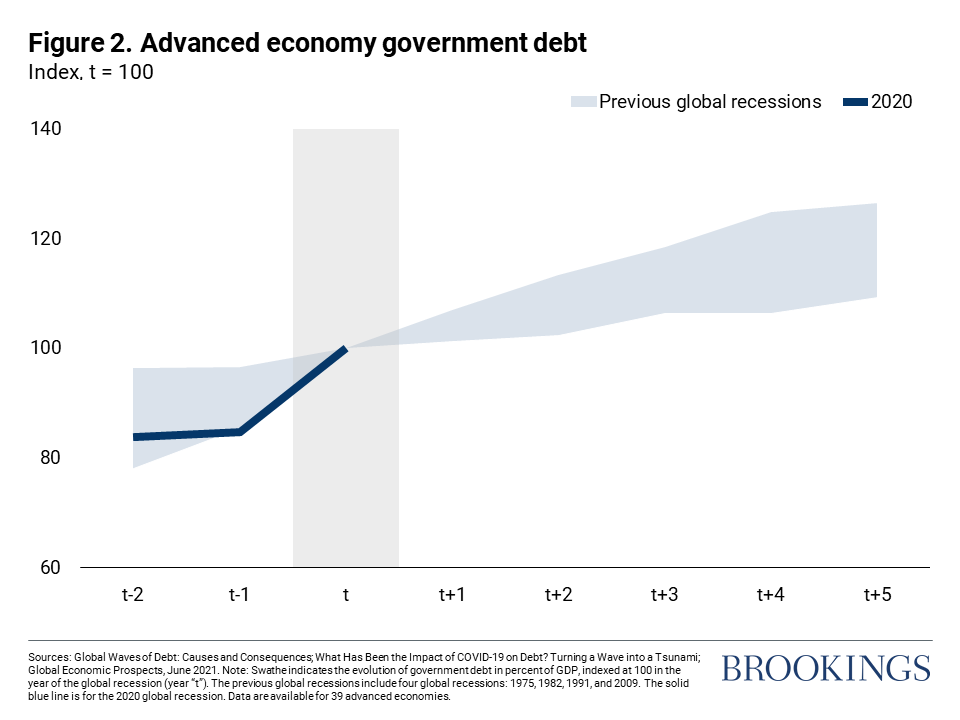

Advanced economy debt has seen a consistent jump in the five years after every global recession, with an increase of 3-14 percentage points after the global recessions prior to 2020 (Figure 2). The last three recessions all saw an increase in advanced economy debt of more than 10 percent of GDP.

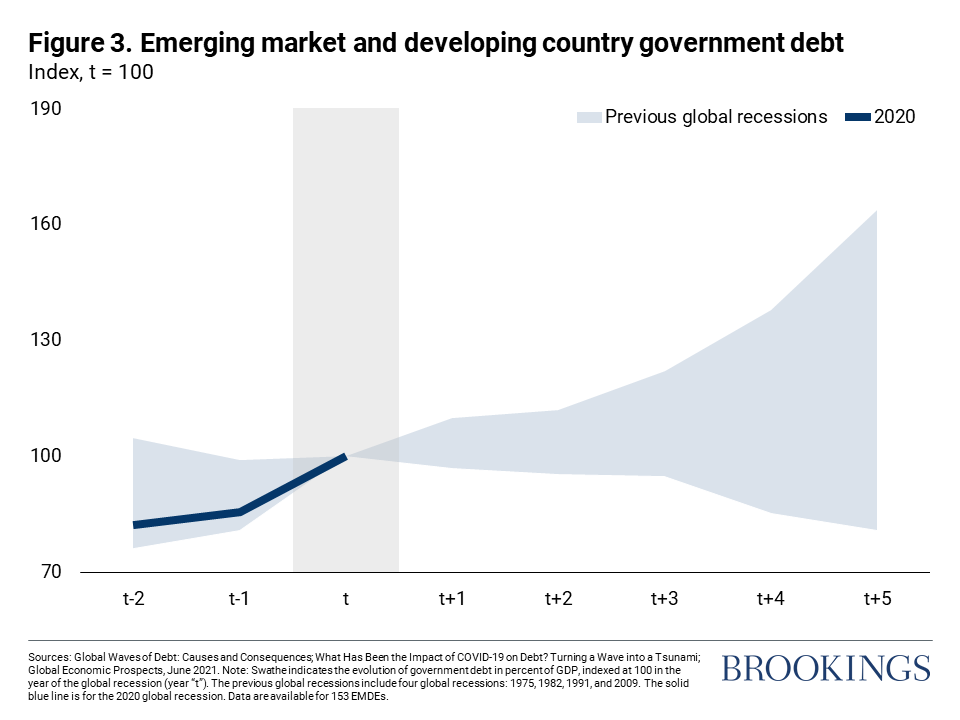

In contrast, the evolution of government debt in EMDEs has been more erratic (Figure 3). Government debt in EMDEs excluding China saw small declines in the five years after the 1991 and 2009 recessions. For the 1991 recession, debt rose in the immediate aftermath of the recession but then decreased rapidly as growth recovered. While in the 2009 recession government debt saw a modest increase during the recession but stabilized thereafter, as EMDEs were less affected and recovered more rapidly from the global financial crisis than advanced economies.

Regional dimensions: a mixed picture but not for everyone

Regionally, the evolution of government debt after global recessions was more varied. Almost all regions saw an increase in debt following the first two recessions, with particularly large increases in East Asia and the Pacific (EAP), Latin America and the Caribbean (LAC), and sub-Saharan Africa (SSA). EAP and LAC saw an unwinding of this debt in the period after the 1991 recession as debt was reduced, including due to the provision of debt relief (via the issuance of Brady bonds), while debt in SSA rose further as many countries did not receive debt relief until the late 1990s.

Debt was broadly stable in most regions following the 2009 recession, which mainly affected advanced economies. Overall, all regions other than SSA saw at least one global recession episode in which government debt declined. In SSA, however, government debt has increased following each previous recession, and debt only declined during the late 1990s and 2000s as a result of the Heavily Indebted Poor Countries Initiative and Multilateral Debt Relief Initiative. SSA has the largest number of LICs, and more than half of LICs are in debt distress or at high risk of debt distress.

Hopes and realities: no time for complacency

In the medium term, some expect that global government debt stocks will stabilize at current levels as a result of the post-pandemic rebound in growth and withdrawal of fiscal support measures. The expected stabilization in debt-to-GDP ratios may alleviate some concerns about elevated debt levels at present.

If such a stabilization materialized, however, it would be a significant departure from debt developments in the aftermath of previous recessions, particularly in the case of advanced economies and countries in SSA. Furthermore, forecasts of government debt tend to suffer from optimism bias: actual government debt to GDP ratios have been shown to be about 10 percentage points of GDP higher after five years than initially forecast, on average.

In light of this historical record, and given large financing gaps and significant investment needs, including facilitating the energy transition, a stabilization in debt levels looks optimistic. Even if debt does stabilize, it remains at exceptionally elevated levels by historical standards and may rise if current low interest rates do not persist.

What are the implications of these observations for policymakers? It is critical to avoid complacency among policymakers who may have optimistic views about debt prospects in the near term. Some policymakers in EMDEs may be tempted to rely on growth alone to lower debt while some others hope that low interest rates would help keep debt service manageable. Policymakers should hope for the best but prepare for the worst as a new monetary policy tightening cycle gets underway in advanced economies.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Does government debt increase after global recessions?

December 17, 2021