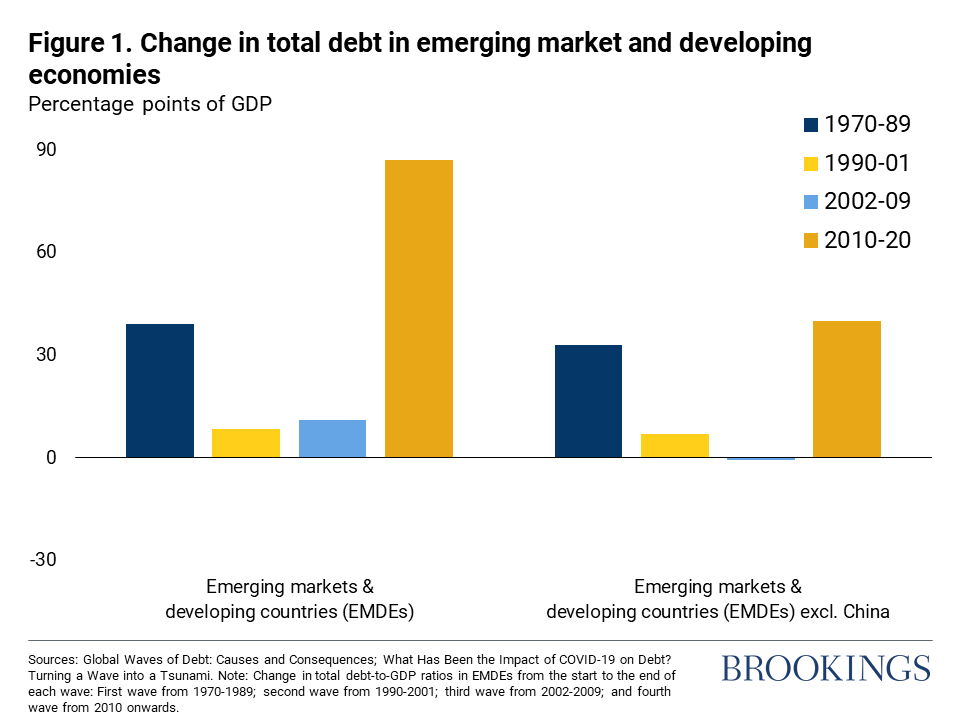

Starting in 2010, a new wave of debt accumulation—the “fourth wave” of debt—had been underway in emerging market and developing economies (EMDEs, Figure 1). With the sharp increase in debt during the COVID-19 pandemic, the fourth wave of debt has turned into a tsunami and become even more dangerous. The tsunami of debt has amplified the difficulty of resolving debt not just because of record debt levels but also because of significant changes in the structure of debt markets.

Sharp and broad-based increase in debt

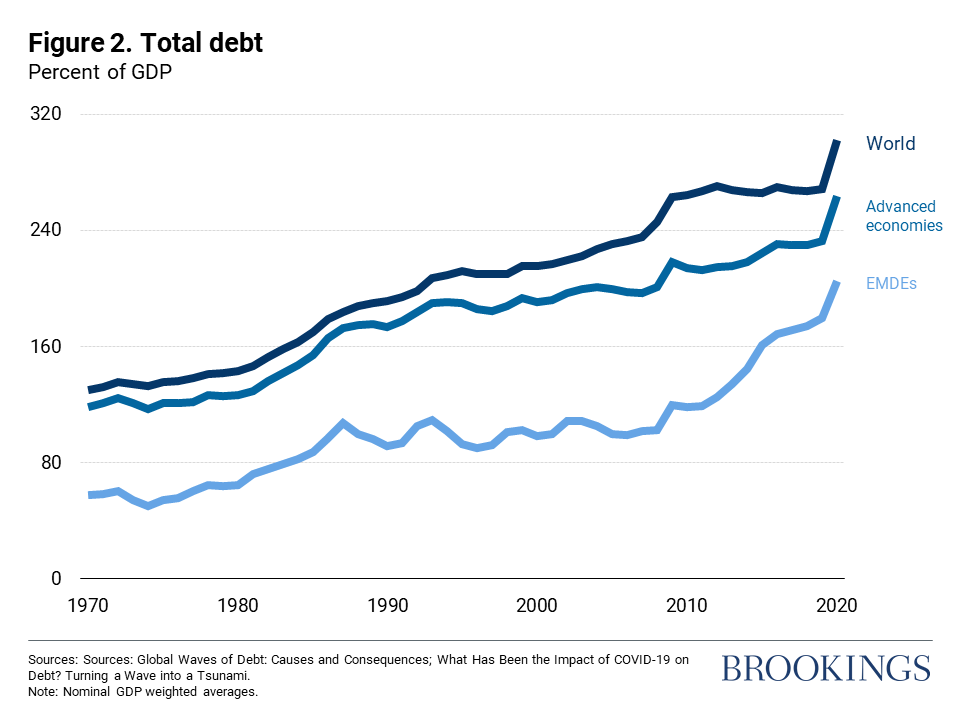

In 2020, total global debt rose by 30 percentage points of GDP, to 263 percent of GDP—the largest single-year increase since at least 1970 (Figure 2). This increase was broad-based, evident across government and private debt, domestic and external debt, and the majority of countries. In EMDEs, total debt went over 200 percent of GDP, and in advanced economies, total debt exceeded 300 percent of GDP in 2020.

As output plummeted in the worst global recession since World War II and governments enacted unprecedented fiscal support measures, global government debt registered its fastest single-year jump to roughly 100 percent of GDP, its highest level in half a century. The increase was near-universal. Government debt rose in almost nine-tenths of countries and at its fastest pace in half a century in around one-quarter of countries.

Private debt also rose at a record pace and to an unprecedented high in 2020 as output collapsed, lockdowns closed businesses, and fiscal, monetary, and regulatory policy measures supported credit extension. Globally, it jumped by 15 percentage points of GDP to 165 percent of GDP in 2020, its highest level since records started in 1970. Similar to government debt, the jump in private debt was broad-based, affecting more than four-fifths of countries.

The bulk of the increase in total debt in 2020 was accounted for by rising domestic debt. In advanced economies, rising domestic debt accounted for about one-half of the increase in total debt in 2020; in EMDEs, for nine-tenths; and globally for three-fifths. In advanced economies, less than one-half of total debt (and less than one-third of private debt) is domestic whereas, in EMDEs, total debt remains predominantly domestic (85 percent of total debt), especially for private debt, which is nine-tenths domestic. Global external debt also rose by 12 percentage points of GDP in 2020, to 114 percent of GDP in 2020, and, as a result, the stock of external debt at the global level now exceeds its 2010 level, after a decade of decline.

Larger risks

Thanks to exceptional monetary policy support, borrowing costs have fallen to record low levels. Low global interest rates can make additional debt-financed government support seem attractive, especially when growth rates are expected to be above interest rates. However, rapid debt accumulation, triggered by fiscal support measures, still entails significant risks. There is no guarantee that any future economic shock will lower interest rates.

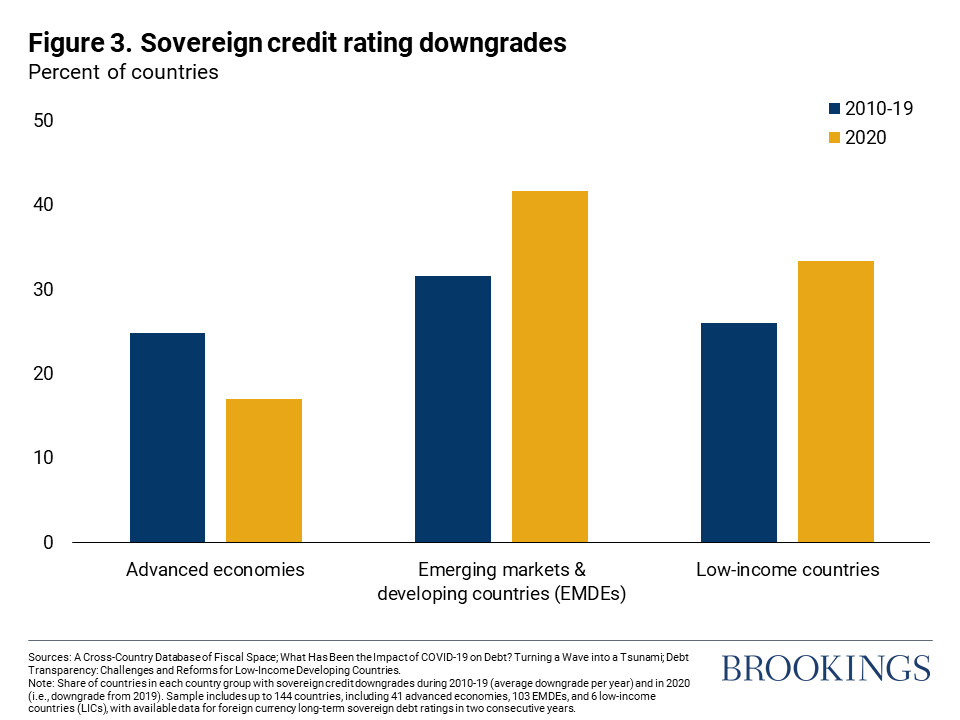

In addition, EMDEs face a risk of sudden stops of capital flows, especially if they have other vulnerabilities like sizeable foreign currency debt, overvalued exchange rates, and financial system fragilities. This is also recognized in sovereign risk ratings: The fraction of EMDEs that experienced sovereign credit downgrades in 2020 was larger than that over the 2010-19 period, whereas in advanced economies it was smaller (Figure 3).

Risks associated with rapid debt accumulation have been magnified because of the likely adverse impact of some policy interventions on policy frameworks. Many governments have heavily encouraged credit extension and eased regulatory policies since the beginning of the pandemic. These necessary measures prevented a credit crunch. However, private sector liabilities could eventually migrate onto government balance sheets, either in a financial crisis or, indirectly, in a protracted period of low growth.

Similarly, unprecedented monetary policy support measures were necessary due to the magnitude of the pandemic shocks. However, these policies may also sow the seeds of solvency problems that may become apparent once global interest rates begin to rise from historically low levels. The sharp increase in debt in a short period and looser fiscal controls also heighten the risk that not all of the debt was used for productive purposes.

New policy challenges

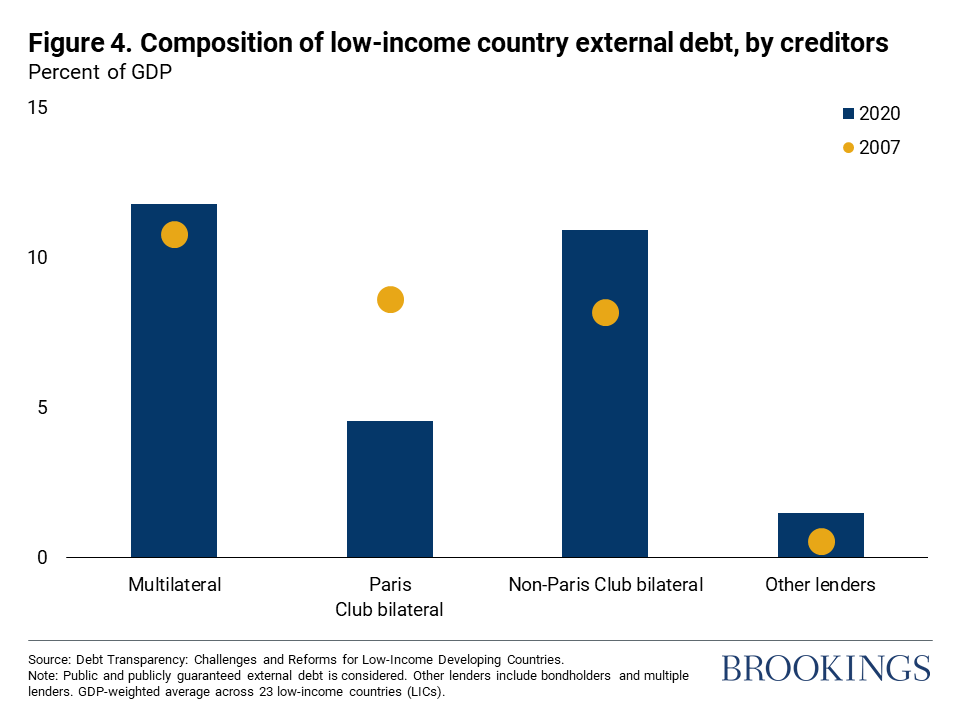

For countries that get into debt distress, achieving a successful resolution may be more difficult than it was in the past. Specifically, future debt restructurings will likely be more complicated because of a more fragmented creditor base than in the past and a lack of transparency in debt reporting. The importance of bilateral non-Paris Club lenders has increased significantly over the past decade (Figure 4). The increasing number of private creditors and range of financial instruments further complicates debt resolution. The growing diversity of creditors and complexity of debt instruments has been associated with greater uncertainty about the level and composition of debt, as not all creditors are bound by a single set of reporting standards and loan terms are often confidential.

In several dimensions, the playing field is currently tilted in favor of creditors and discourages prompt and comprehensive debt resolution. While 91 percent of sovereign bond issuance since 2014 has included collective action clauses that facilitate restructuring, a large legacy stock without such clauses remains: about 50 percent of outstanding international debt does not include collective action clauses. In the past, delays in resolving high debt were associated with weaker output and investment growth, raising the prospect that even slower debt resolution could lead to a lost decade of growth in some countries already facing significant debt problems. In addition to sovereign debt, the rise of private debt, especially during the pandemic, highlights the importance of effective resolution frameworks to mitigate the risk of private debt overhang.

Urgent action needed

The challenges of resolving record-high debt point to the urgency to act on the parts of both national policymakers and the global community. National policymakers will need to improve policy frameworks to make debt sustainable, as well as to consider the best approaches to resolving debt if it becomes unsustainable. The global community needs to act rapidly and forcefully to ensure that this debt tsunami does not end with a string of debt crises in EMDEs, as earlier waves did.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Debt tsunami of the pandemic

December 17, 2021