The COVID-19 pandemic touched most businesses across Central Europe, but some were affected more than others. Countries implemented diverse policies to alleviate the shock to firms. In response to the first wave of COVID-19, sizable fiscal programs were deployed, amounting to 11.7 percent of GDP in Poland, 6.7 percent in Bulgaria, and 5.4 percent in Romania. All countries implemented lending and credit guarantee schemes. However, as shown in Table 1, the policy mix varied across countries. Poland implemented policies to support the self-employed and workers through wage subsidies, Bulgaria reduced VAT on selected goods and services, and Romanian firms had access to loan subsidies and debt moratoria.

Table 1. COVID-19 support programs for private firms in Bulgaria, Poland, and Romania

| Bulgaria | Poland | Romania | |

| Debt moratorium | ✓ |

✓

|

|

| Social security contributions |

✓

|

||

| CIT / PIT deferrals |

✓

|

✓ | ✓ |

| VAT deferrals |

✓

|

||

| Wage subsidies | ✓ | ||

| Financing for self-employed |

✓

|

✓ | |

| Grants and subsidies | ✓ | ✓ | |

| Direct lending | ✓ | ✓ | ✓ |

| Loan guarantees | ✓ | ✓ | ✓ |

The targeting across different types of firms also varied. Poland emphasized support for micro and small firms, as opposed to Bulgaria and Romania that prioritized support to medium and large firms. Most policies were time-bound, and governments eventually continued to support specific industries that remained subject to COVID-19 restrictions.

NOT ALL EARLY SUPPORT WAS BROAD

At the onset of the pandemic, countries were advised to follow the “quick and broad” approach, i.e., provide firms with immediate, indiscriminate, and easy access, and then taper and target support over time. This broad approach appears to have been adopted in Poland, but not as much followed in Romania and Bulgaria. In Poland, almost 80 percent of firms reported benefiting from a public program by fall 2020, compared to only 47 percent in Romania and 30 percent in Bulgaria. By 2021 (Wave 3 of the survey), only 26 percent of firms surveyed across all three countries reported receiving support since the last interview.

Early public support reached the most affected firms

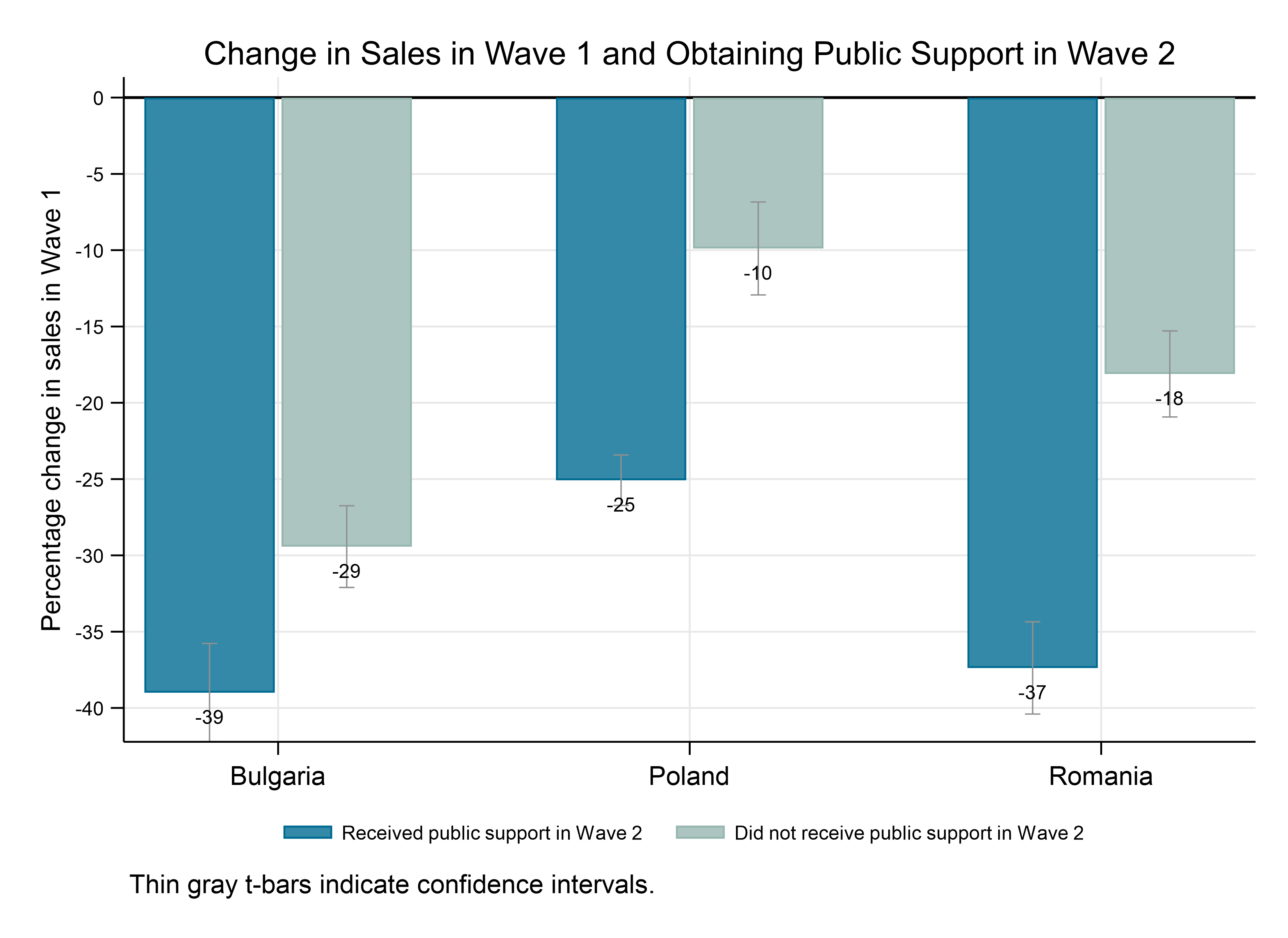

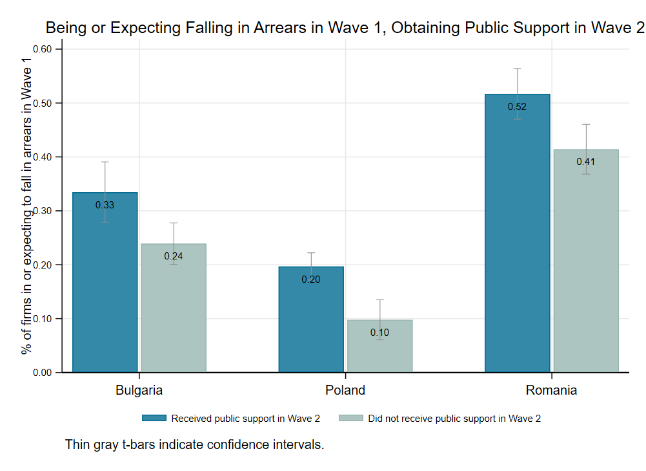

In all three countries, we found that firms that accessed public support experienced a greater drop in sales than those that did not when comparing Waves 1 and 2 (Figure 1). Similarly, firms that had already fallen or expected to fall into arrears were more likely to seek and access public support, especially in Poland and Romania (Figure 2). This suggests that initial country strategies reached the most affected firms. However, by early 2021 (Wave 3) only Poland was supporting firms with significantly lower sales, indicating stronger targeting of distressed firms than in Bulgaria and Romania.

Figure 1. Change in sales and public support

Source: COVID-19 Business Pulse Survey Dashboard.

Note: Wave 1 surveys were implemented in May and June 2020 in all three countries. Wave 2 took place in September and October of 2020 in Poland, and November and December of 2020 in Bulgaria and Romania.

Figure 2. Being in or expectation of falling in arrears and public support

Source: COVID-19 Business Pulse Survey Dashboard.

Note: Wave 1 surveys were implemented in May and June 2020 in all three countries. Wave 2 took place in September and October of 2020 in Poland, and November and December of 2020 in Bulgaria and Romania.

TARGETING SMALL AND YOUNG DISTRESSED FIRMS REMAINS CHALLENGING

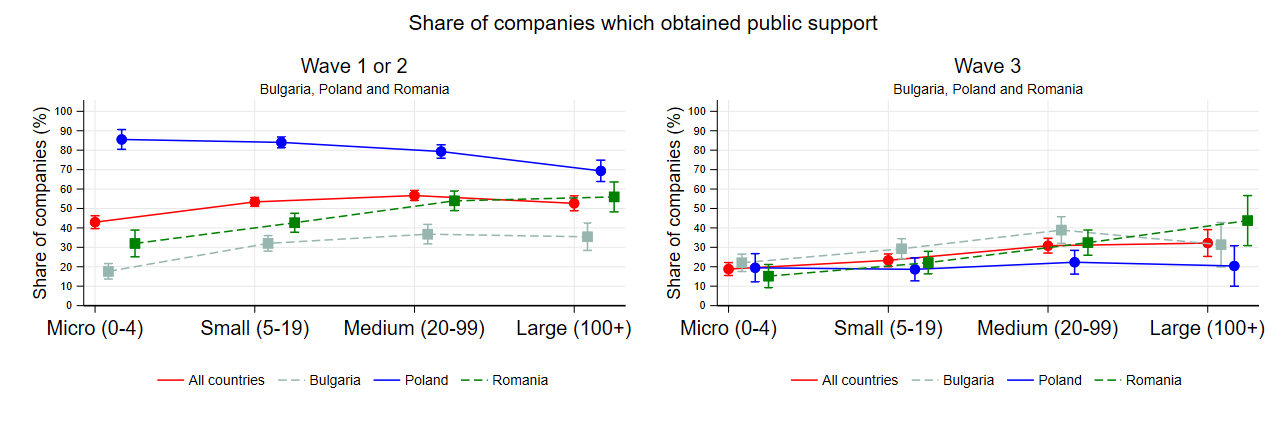

As indicated in our first blog, the pandemic shock disproportionately hit smaller and younger firms. In Poland, micro and small firms accessed support slightly more frequently than larger firms (Figure 3, Left). Conversely, in Bulgaria and Romania, larger companies were more likely to receive support than micro-companies across all three survey waves. In contrast, we observe no significant differences between young and mature firms in terms of their access to public support.

Figure 3. Share of companies that obtained public support in Waves 1 and 2 (left) and Wave 3 (right)

Source: COVID-19 Business Pulse Survey Dashboard.

Note: Wave 3 took place in February and March of 2021 in Poland, and May and June of 2021 in Bulgaria and Romania.

SUPPORT ROLLOUT MERITS ATTENTION

Three reasons stand out when investigating why firms did not avail themselves of available public support: complexity, transparency, and awareness. In Romania and Bulgaria, as many as 29 and 14 percent of firms that did not receive support complained about cumbersome applications. In Bulgaria and Romania, 10 and 4 percent of firms respectively reported not having the right connections to access support, whereas 17 percent of Romanian firms that did not receive support were unaware of its availability.

KEY POLICY TAKEAWAYS

- From indiscriminate to targeted policies of viable firms: Initially, given limited information, supporting affected firms rapidly and indiscriminately was essential. As the crisis continues and fiscal space narrows, it becomes critical to target viable firms in distress—with attention to smaller and younger firms.

- Simplified and transparent procedures: Key aspects directly addressable by policymakers include the simplicity of the application process, the transparency of selection procedures, and the speed with which support is disbursed. This can be facilitated by leveraging existing firm data and digital services for screening, application, selection, and delivery of support.

- Clear and targeted communication: Merely making support available is insufficient if firms are unaware of its existence, warranting clear and targeted communications to potential beneficiaries.

Related Content

Authors

Commentary

How COVID-19 policy responses differed in Central Europe

October 11, 2021