This is the first blog in a series using a survey of firms to assess COVID-19’s impact on sales, firm responses, public policy efforts, and future outlooks with a focus on uncertainty and financial risks.

Slam in sales, but signs of recovery

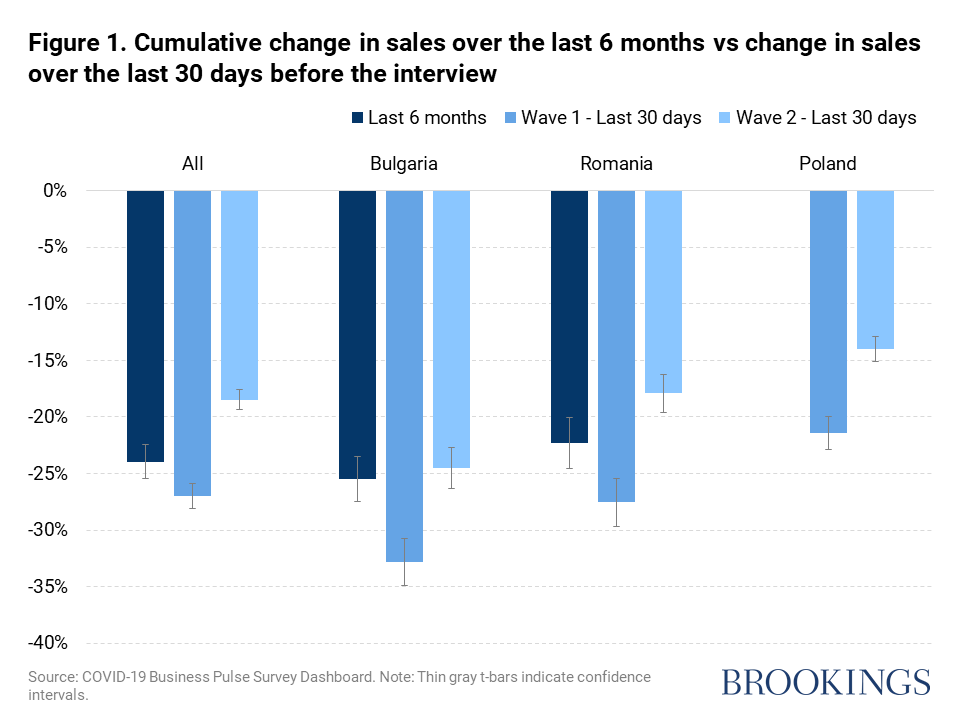

What was COVID-19’s damage in Bulgaria, Poland, and Romania? The first six months of the pandemic claimed a quarter of total sales on average (Figure 1). Firms reported a major drop in sales during the first wave averaging between 21 percent in Poland to 31 percent in Bulgaria. Some of the losses were recovered by the end of 2020 and early 2021 (Figure 1), but will this nascent rebound be sustained and how long will it take to bounce back to pre-pandemic levels? Upcoming survey waves will provide insights on this but there are reasons to be cautious about the recovery given that the second wave indicates firms were reverting to their pre-pandemic trajectories.

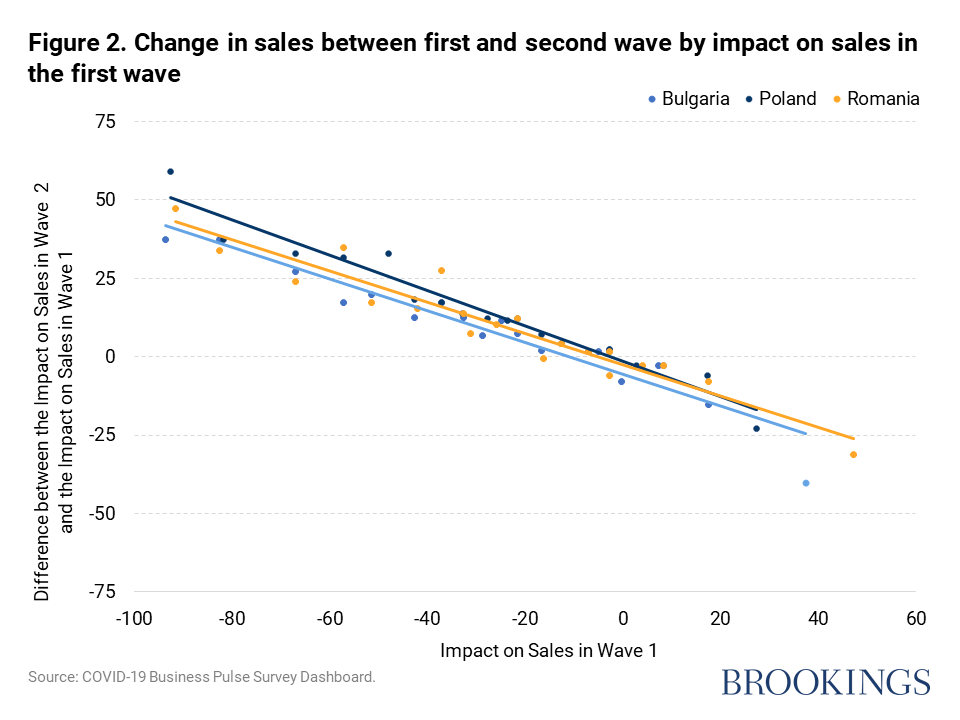

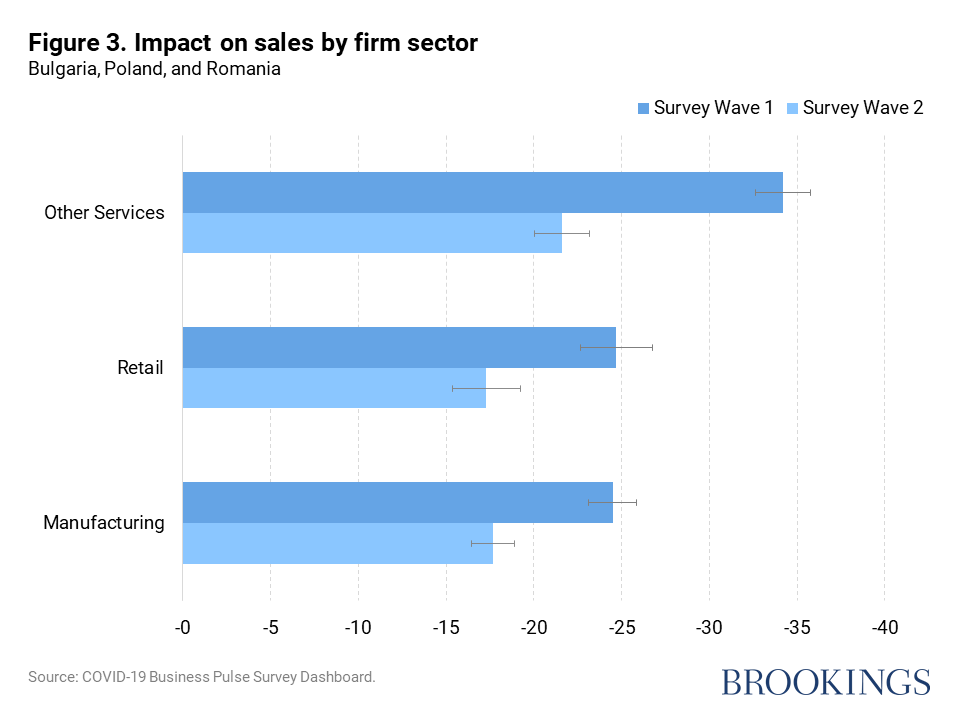

Who suffered most? Looking at countries and sectors, we find (Figure 2) firms that experienced the highest drop in sales in the first phase of the pandemic were also the ones that recovered most as the crisis unfolded, once the short-term shock and initial lockdowns receded (Figure 2). This pattern is consistent across the three countries. However, comparing across countries, we find that Polish firms recovered faster than ones in Bulgaria and Romania for every level of initial sales drop (Figure 2 the navy blue line representing the results of Polish firms lies above the lines of Romania and Bulgaria). This inverse relationship between recovery and sales losses is preserved when comparing firms by sector (Figure 3). The lockdown clearly affected businesses in different sectors heterogeneously, with those in the hospitality sector being especially affected versus professional services that could continue with work being done from home. The service sector stands out as being both the most affected but also the sector experiencing the highest rebound during the second wave (almost 13 percentage points vs. 7 percentage points for retail and manufacturing).

Watch the small and young firms

Going beyond aggregate analysis, at a country and sectoral level, we find that there are some firms that were especially affected. We find that firms of all sizes suffered significant losses in sales, but the magnitude of the shock changes linearly with size: The drop for micro-firms (0-4 employees) was twice as large as the drop for the largest firms (100+ employees) . Similarly, we find significant differences correlated with the age of firms. The youngest firms underwent the biggest drop in sales (40 percent) while established firms (10 years or older) shared a similar drop in sales, around 26 percent. We also find that these two dimensions are correlated but independent in explaining firms’ exposure to the COVID-19 shock, i.e., the smallest and youngest firms were the most critically affected by the pandemic.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Same shock, different impacts: The impact of COVID-19 on firms in Central Europe

June 17, 2021