Last week, the African Economic History Network published “The Fiscal State in Africa: Evidence from a century of growth,” a working paper in which the authors examine African countries’ ability to raise revenues from taxes and other sources in order to support the provision of public services and development. To do so, the authors construct a comprehensive new dataset of tax and revenue collection for 41 African polities from 1900 to 2015, including direct and indirect taxes, resource and trade taxes, and non-tax state revenue.

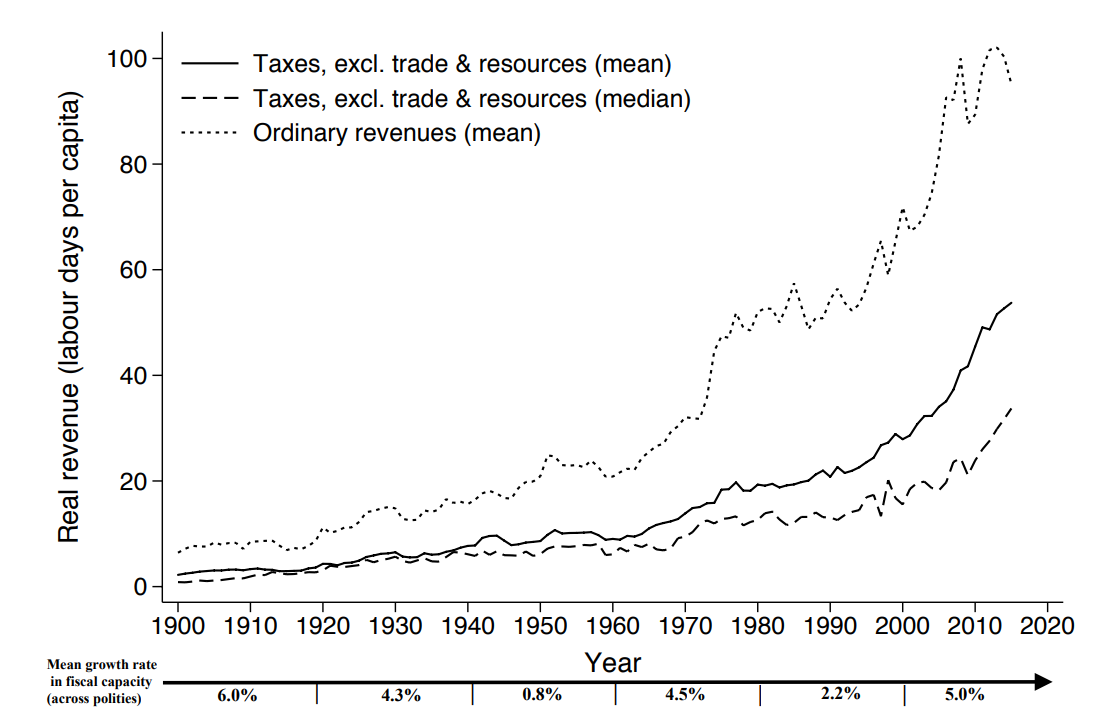

The authors find that many African countries have substantially increased their capacity for revenue collection over this time period. Figure 1 shows that normalized fiscal capacity, as measured by the mean and median of non-trade and resource taxes across countries, and total ordinary revenues, which include all sources of revenue, were more than 11 times larger in 2000 than in 1900. This growth has not always been stable: In recent times, the period of 1980-2000 stands out as one in which revenue collection capacity stagnated, with a mean growth rate of only 2.2 percent over these two decades, and with zero or even negative growth in many countries. The authors argue that the perception of “state weakness” in Africa originates from this time period and that this perception neglects to consider periods of strong revenue collection growth in the decades before and after this period.

Figure 1. Average real revenue levels across African countries, 1900-2015

Source: Thilo Albers, Morten Jerven and Marvin Suesse. The Fiscal State in Africa: Evidence from a century of growth. African Economic History Network Working Paper. 2020.

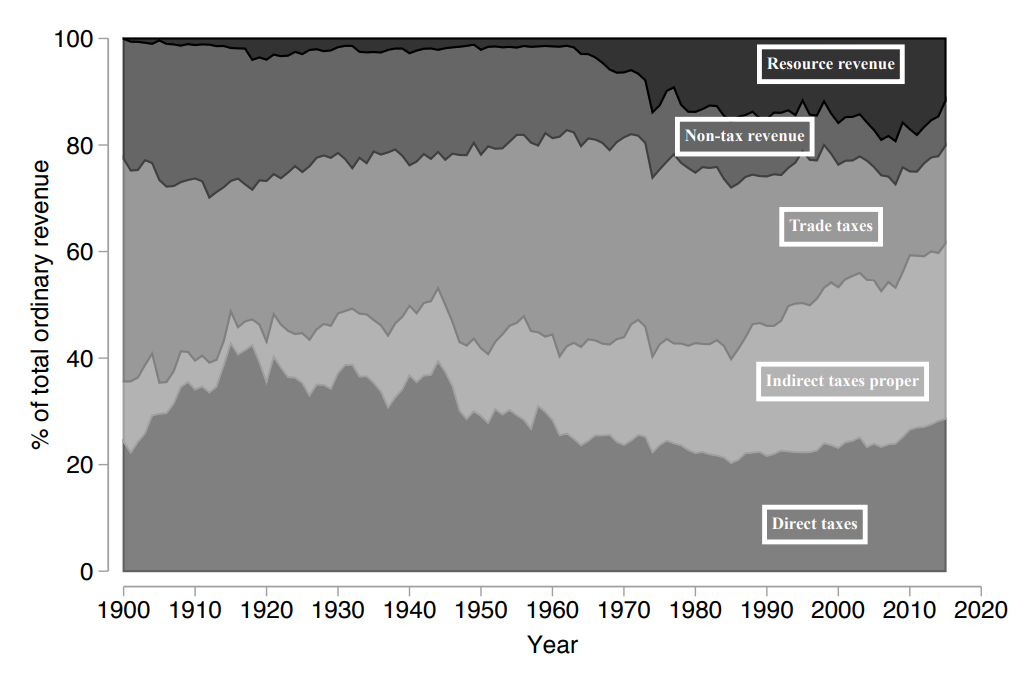

Figure 2 shows the composition of revenues collected by African countries between 1900 and 2015. Notably, resource revenues and indirect taxes have increased substantially as a percent of total ordinary revenues in the post-colonial period. In contrast, non-tax revenue, trade taxes, and direct taxes have all declined as a percent of total revenue since around 1970, although collection of direct taxes has slightly recovered in the past two decades. On average, direct and indirect taxes contributed the majority of total ordinary revenues in 2015, at around 60 percent of all revenues. The authors argue that this finding runs counter to a common narrative that African countries have low capacity to raise these “hard-to-collect” taxes.

Figure 2. Composition of revenue in African countries, 1900-2015

Source: Thilo Albers, Morten Jerven and Marvin Suesse. The Fiscal State in Africa: Evidence from a century of growth. African Economic History Network Working Paper. 2020.

The authors note that there is significant heterogeneity in fiscal capacity across African countries and time periods. By analyzing historical trends in revenue collection, they find strong growth in fiscal capacity in times when there was insufficient trade to be taxed—such as during the two world wars—and low growth in fiscal capacity during periods when alternative finance was available through aid and debt. Their analysis of country-specific trends has less clear results: They find that democratic institutions increase fiscal capacity only within ethnically homogenous societies, that interstate warfare only increased fiscal capacity for colonial states, and that high government turnover reduces fiscal capacity. Additionally, the authors’ country-specific analysis confirms that access to alternative revenue sources, including debt and aid, is associated with lower growth in fiscal capacity. At the same time, however, the authors also find that resource income does not generally lead to lower fiscal capacity. Overall, the authors state that these findings provide unique insight into the development of African states and their abilities to raise taxes.

Related Books

For more on taxation in Africa, see “Taxing mobile phone transactions in Africa: Lessons from Kenya” by Njuguna Ndung’u and “Tax to finance the SDGs, but not to undermine them” by Wilson Prichard and others. For more on domestic resource mobilization, see “Approaches for better resource mobilization to finance Africa’s Sustainable Development Goals” by Brahima Coulibaly.

Note: The working paper includes all African countries excluding Cabo Verde, Comoros, Djibouti, Equatorial Guinea, Eritrea, Ethiopia, Liberia, Libya, Mauritius, Sao Tome and Principe, Seychelles, Somalia, and South Sudan. Forty-one countries are included in the balanced sample; 46 are included in the full sample. Figures included here use the balanced sample of 41 countries.

Related Content

Commentary

Figures of the week: Taxation in Africa over the last century

October 15, 2020