The Hutchins Center held an event on this topic on December 5, 2023.

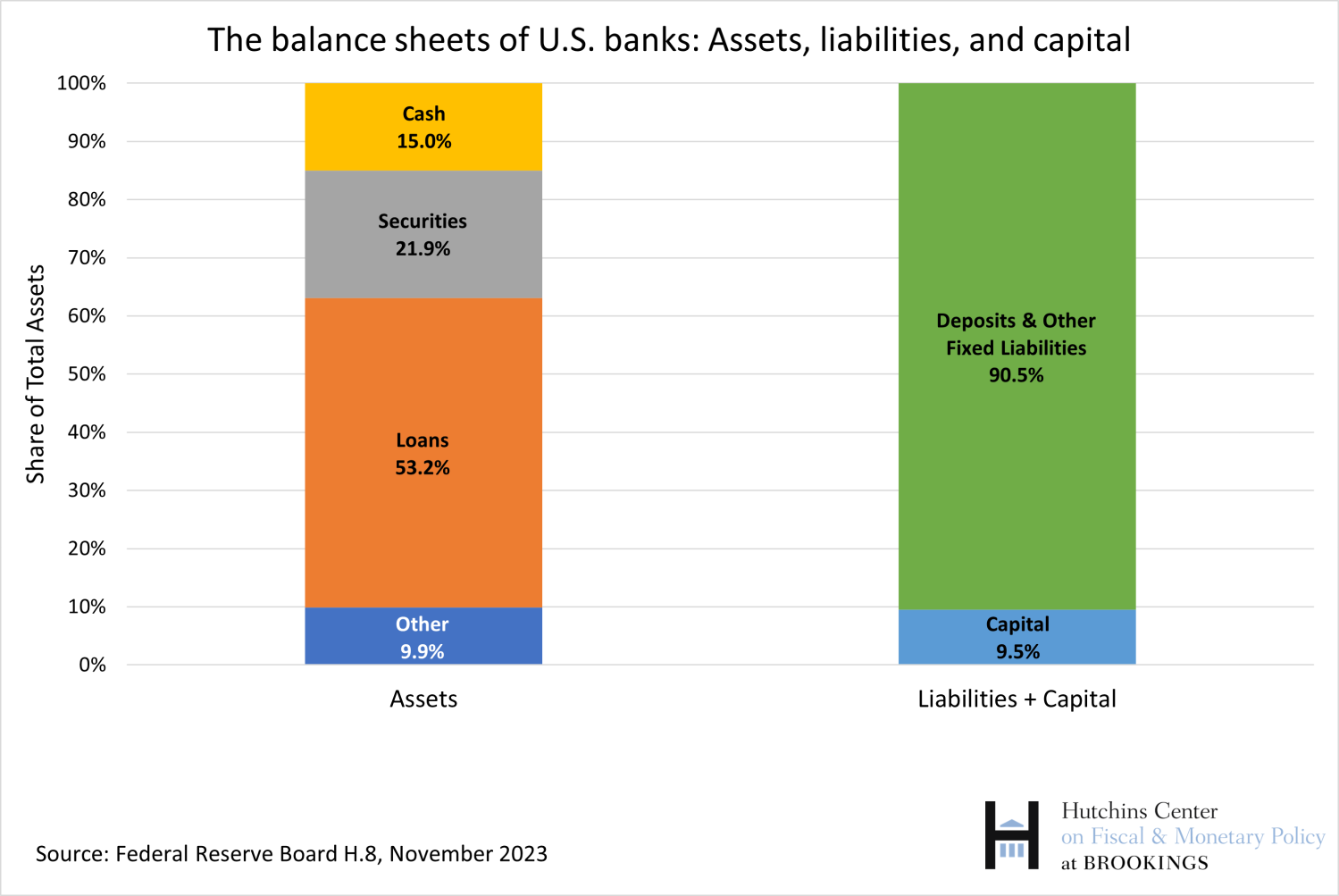

Bank capital is a measure of bank shareholders’ investment in the business. In contrast to deposits or money a bank has borrowed, capital does not have to be paid back. A bank that has sufficient capital can cover customers’ deposits even if the loans it has made aren’t repaid or if its investments drop in value. In other words, it is a cushion or buffer that protects a bank from insolvency—and, thus, reduces the risk that a bank failure triggers system-wide financial instability. As the chart below illustrates, capital is the difference between a bank’s assets (left) and its liabilities (right).

Who decides how much capital banks must hold?

Banks decide for themselves, but regulators all over the world require banks to hold a certain amount of capital—calculated as a percentage of their assets—so they are less likely to fail, seek a government rescue, or trigger a financial crisis. If a bank has too little capital, managers may be tempted to take imprudent risks because their shareholders have little to lose if things go wrong and will profit handsomely if things go well. Because capital bears more risk, capital is more expensive for banks than raising funds by taking deposits or borrowing money. So banks want to have just enough capital to satisfy regulators, credit rating agencies, creditors, and shareholders, but no more. In general, the more capital a bank has to have, the lower its profits. Because banks are required to have a set amount of capital for every loan or security they hold, requiring them to hold more capital can make them charge more for some loans. How much more is a subject of debate. But if banks have too little capital to absorb the risks they take, they can, in bad times, trigger economy-wide financial instability. It is clear now that many big banks had too little capital going into the Global Financial Crisis in 2007. Since then, U.S. regulators have increased the minimum amount of capital that banks are required to have. Regulators are now proposing further increases in required capital (known as the “Basel III Endgame”), to the dismay of many big banks who are lobbying aggressively against the proposal.

What is the Basel Committee?

The Basel Committee on Banking Supervision—so named because it meets in Basel, Switzerland—was established in 1974 to enhance financial stability by improving the quality of bank supervision. It is the primary global standard-setter for the prudential regulation of banks, but it has no legal authority to impose the minimum standards to which the Committee agrees. Adopting rules is the responsibility of the governments of the 26 countries (plus the European Union and Hong Kong) who comprise the committee. The U.S. is represented on the Basel Committee by the Federal Reserve Board in Washington, the New York Federal Reserve Bank, the Office of the Comptroller of the Currency (OCC), and the Federal Deposit Insurance Corporation (FDIC).

What is the Basel III Endgame?

Basel III is a set of measures developed by the Basel Committee in the years following the global financial crisis of 2007-09. The measures, rolled out over several years, aim to strengthen the regulation, supervision, and risk management of banks. The final set of rules has been dubbed the “Basel III Endgame.” These rules focus on the amount of capital that banks must have against the credit, operational, and market riskiness of their business. In July 2023, the Fed, OCC, and FDIC published for comment proposed changes to bank capital rules in the U.S. that are intended to be aligned with the Basel III standards.

What is risk-based capital?

Since the 1980s, regulators have required banks that make riskier loans or investments to hold more capital than banks with less risky portfolios. To do otherwise, the reasoning went, would make no distinction between a bank that made loans to major corporations and bought super-safe U.S. Treasury bonds and a bank that lent to risky ventures or made high loan-to-value mortgages. Banks adjust the dollar measure of their assets to calculate “risk-weighted assets”—a higher number if a bank’s portfolio is deemed risky—and then apply the capital-requirement percentage to that measure. The formula for assigning risks to various types of assets can influence the cost and availability of credit to various types of borrowers. The risk weight for U.S. government bonds is zero because they are considered very safe; banks don’t have to hold capital against that asset. The risk weights for loans to small businesses and homeowners are higher.

What are U.S. regulators proposing?

Many of the changes are quite technical, and this post will touch on only some elements. The proposal fills 316 pages of small type in the Federal Register. (An accompanying and less controversial proposal that would tweak rules for the very biggest banks is another 18 pages.) Few people besides regulators, executives of banks that would be affected, and their lawyers understand the details.

Regulators say the net effect of the proposal would be to increase the required highest-grade capital (essentially shareholders’ equity plus retained profits) by about 16% on average, with a bigger increase imposed on the biggest banks. Put differently, the largest banks would have to hold an additional 2 percentage points of capital, or an additional $2 of capital for every $100 of risk-weighted assets. The proposal would change both the numerator and the denominator in the capital/risk-weighted assets calculation.

Among the major changes, the regulators would:

- Apply the stiffest risk-based capital approach to more banks, those with $100 billion or more of assets, up from the current threshold of $700 billion. Some 37 large banks in the U.S. would be covered; they hold more than three-quarters of all bank assets in the U.S. Community banks and smaller regional banks wouldn’t be affected.

- Reduce the ability of banks to use their own models for calculating capital requirements for loans and instead require them to use a standard measure.

- Require banks to have more capital for risks posed by trading activities and by operations; require them to use standard models instead of internal ones to gauge these risks. These elements account for the bulk of the proposed increase in required capital.

- Require any bank with assets of $100 billion or more to reflect in their capital calculations any gains and losses in portfolios deemed “available for sale,” as opposed to securities the bank plans to hold until maturity.

Even among the regulators, there is some opposition to the proposals. The Federal Reserve Board voted 4-2 to support them, and Federal Reserve Chair Jerome Powell voted in favor of putting them out for comment, but expressed some reservations. The vote on the FDIC board was 3-2. On both boards, the “no” votes were from Republicans.

What is operational risk?

A substantial portion of the proposed increase in capital is targeted at banks’ operational risks. Operational risk refers to the risk of loss from inadequate or failed internal processes, people, and systems, or from external events, including rogue traders, fraud, and big fines for violating anti-money laundering or other laws. Under current rules, only the biggest banks are required to have capital against operational risk; the proposal would raise the requirement for the largest banks and extend it to more banks. Operational risk in the proposal is measured by a “business indicator” based on the size, complexity, and specifics of a bank’s lending, investing, and financing activities and by its history of operations-related losses. “Banking organizations with higher overall business volume are larger and more complex, which likely results in exposure to higher operational risk,” the regulators add. “Higher business volumes present more opportunities for operational risk to manifest. In addition, the complexities associated with a higher business volume can give rise to gaps or other deficiencies in internal controls that result in operational losses. Therefore, higher overall business volume would correlate with higher operational risk capital requirements under the proposal.” The impact will be greatest on banks that have large businesses outside conventional lending, such as wealth management and other fee-generating businesses.

Proponents say the changes would give banks an incentive to mitigate these risks. But Fed Governor Christopher Waller says that the regular stress tests that the Fed conducts are sufficient incentive to reduce operational risks, and that the proposal would require banks to earmark twice as much capital for operational risks than required by the stress tests. And FDIC Vice Chair Travis Hill says, “Operational risk is an amorphous concept, a catch-all category that encompasses a large and highly variable set of risks, ranging from fraud to bad behavior to overzealous enforcement agencies to cyber attacks to asteroids.” (Both Waller and Hill voted against the proposal.) The Bank Policy Institute, a research and advocacy group for big banks, argues against penalizing banks for past operations-related losses and says the new rules would disadvantage banks with business models that rely heavily on fees.

Which parts of the banking business would be hit hardest by the new rules?

Because of the operational and market risk provisions of the proposal, much of what is driving the increase in the big banks’ required capital are activities outside of simple deposits-and-loans banking, such as trading, market-making, wealth management, and investment banking. Thus, banks with large such operations will be hit harder than those with business models more concentrated on lending.

Specific parts of the proposal will affect particular industries. For instance, companies in the renewable energy business say that the proposed increase in the amount of capital banks are required to hold for certain types of lending to their firms (in the form of “tax equity investments”) will dilute the effectiveness of tax incentives for projects aimed at reducing global warming.

What are the major arguments in favor of the regulators’ proposal to increase capital?

The basic argument is that capital is the ultimate protection against bank failures and government bailouts when those failures threaten financial stability. Given the shortcomings of supervision, proponents say that current capital standards don’t adequately address the risks that banks are taking. The regulators say that the changes “would better reflect the risks of these banking organizations’ exposures” and “enhance the consistency of requirements across large banking organizations and facilitate more effective supervisory and market assessments of capital adequacy.” Banks with too little capital may be reluctant to make loans to small businesses and other risky borrowers.

Economists Stephen Cecchetti and Kermit Schoenholtz describe higher capital as “an ounce of prevention” against bank failures. “Prevention,” they write, “means that regulations should limit incentives to risk-taking while also requiring that institutions build in shock absorbers.” Given the shortcomings of supervision and the tendency of policymakers to rescue failing banks, they argue, capital and liquidity requirements should be “sufficiently rigorous.” When regulators required banks to have more capital after the Global Financial Crisis, some banks protested that this would hurt their businesses and constrain lending. That didn’t happen. Cecchetti and Schoenholtz wrote in 2020: “[H]igher capital requirements have not hurt banks, they have not hurt borrowers, and, if there was any macroeconomic impact, it was probably offset by monetary and fiscal policy. In other words, it is difficult to find any social costs associated with increasing capital requirements and improving the resilience of the financial system.”

Michael Barr, the Fed’s vice chair for (bank) supervision, argues:

“[R]egulatory requirements, including capital requirements, must be aligned with actual risk so that banks bear the responsibility for their own risk-taking. The proposal takes an important step toward better aligning capital requirements with risk, both for the specific risks in play this spring [the March 2023 collapse of Silicon Valley Bank and First Republican Bank], and for a much broader set of risks that banks face…

“Capital requirements are… crucial to our mission of safety and soundness and financial stability. Neither regulators nor bank managers can anticipate all risks, or how risks may be amplified and propagated. Events over the past few months have only reinforced the need for humility about our understanding of the causes and consequences of financial stress, and for an approach to capital regulation that makes banks resilient to both familiar and unanticipated risks.”

Barr said the impact of higher capital standards would be “modest” and offset by the “greater resilience” of the banking system which, he said, would contribute to economic growth. Because the bulk of the added capital requirements fall not on lending but on operational and trading activities, Barr estimates that the cost to banks of funding the average lending portfolio (and thus the potential hit to borrowers) would rise by only 0.03 percentage point. Better Markets argues that “appropriately capitalized banks are strong enough to continue providing credit through the economic cycle, in good times and bad, which keeps the economy growing, creates jobs, and reduces the depth, length, and cost of recessions that large bank failures usually cause.”

At a November 2023 hearing, Sen. Sherrod Brown (D-Ohio), who chairs the Senate Banking Committee, said, “Of course, we know the complaints that are coming—in fact, they started before we even saw the proposal. The industry has relentlessly attacked it with the same old tired arguments. Compliance will cost too much, we won’t be competitive, we already have enough capital, we won’t be able to lend to small business. We’ve heard it all before. Let’s be clear: The largest banks will need to re-direct a tiny fraction of their enormous profits over a period of several years to get to the new capital levels. Every single bank that would be impacted by this proposal has the capacity to comply with the new capital levels and extend credit to small businesses and working-class and middle-class families—all while remaining wildly profitable.”

What are the major arguments against the proposal?

Critics say it is overkill, will discourage lending, and will push lending and other activities outside the regulated banking system to less regulated institutions to whom the new capital requirements don’t apply.

When Fed Governor Waller voted against the proposal in July, he expressed concern that it would “increase the cost of credit and impede market functioning without clear benefits to the resiliency of the financial system.” He challenged the conceptual approach that the proposal’s authors took:

“An important question… is why do banks need to sideline separate buckets of operational risk, credit risk, and market risk capital when those risks are unlikely to manifest at the same time? It is similar to asking individuals to establish separate emergency funds for shocks to their income, such as losing their job, and shocks to their expenses, like a fire in their house or their car breaking down. Households understand it is exceedingly unlikely that they will experience a month where all these shocks hit simultaneously, so their emergency funds are less than the sum of those individual expected expenses.”

Randall Quarles, Barr’s predecessor as Fed vice chair, argues that the banking system is already adequately capitalized. He also says that the proposal will drive business out of the regulated banking system to unregulated parts of the system which are less transparent, have smaller capital cushions, and generally aren’t eligible for routine loans from the Fed in a liquidity crunch.

Bank trade associations have been aggressively criticizing the proposals. Recognizing that they won’t win much support by complaining that it will make it harder for them to make money, they argue that it will hurt borrowers and the overall economy. The Financial Services Forum, comprised of chief executives of the nation’s eight largest banks, has a website (americanscantaffordit.com) that deems the proposals “another bill Americans can’t afford.” The Bank Policy Institute has been pumping out policy briefs criticizing every aspect of the proposals and launched a website called stopbaselendgame.com. A centrist political action committee called Center Forward (which doesn’t disclose its donors) ran a TV commercial during a Sunday NFL game attacking the capital proposals.

The banks’ campaign has had some success. In the Senate, 38 Republicans, including all Republican members of the Banking Committee, signed a letter to the regulators in which they said: “[T]hese large increases in capital have not been shown to be evidentially based as the Federal Reserve, FDIC, and OCC have failed to provide proper analysis or data to justify their merits, particularly around the costs they will impose throughout all sectors of the economy. In fact, we have heard widespread concerns regarding the negative impacts that Basel III could have not only on affordable housing but on mortgage lending writ large, small business lending, and consumer lending… Moreover, the proposal disproportionately harms companies that are not publicly listed, who happen to be middle market, private entities, and our millions of small businesses across the country. Each of these potential consequences would have major ramifications alone, but taken in totality, they pose significant harm throughout the economy, particularly in the face of current economic headwinds and tightening credit conditions.”

Some Democrats also have voiced concerns. Rep. Jim Himes (D-CT) told the regulators at a hearing: “The first line of your testimony today was that our banking system is sound and resilient. So a lot of us are struggling to see the clear need for additional capital.” Sen. Mark Warner (D-VA) noted that banks respond to every regulation with cries that it will lead to less lending, but added, “That Chicken Little approach really lessens your cause when this may actually be the time…” He also speculated that tightening capital requirements for banks could push more lending to financial institutions outside the regulatory perimeter.

How would the new capital rules affect mortgages?

The risk weights assigned to some mortgages in the proposal exceed those in the Basel Committee standards. Banks would have to set aside more capital the higher the loan-to-value ratio of the mortgage. They also would have to set aside capital, under the operational risk provision, for mortgages sold to Fannie Mae and Freddie Mac. When the Fed released the proposals, Fed Vice Chair Barr said, “We want to ensure that the proposal does not unduly affect mortgage lending, including mortgages to under-served borrowers.” And Better Markets, a bank critic, notes that banks have been reducing mortgage lending for decades under existing capital rules. But Laurie Goodman and Jun Zhu of the Urban Institute have written: “[The] level of capital that banks would be required… to hold against mortgage loans held in portfolio is excessive, at all LTV [loan-to-value] levels and is likely to further discourage bank mortgage lending. The impact on lending to LMI [low and moderate income] borrowers and communities and to borrowers of color is particularly perverse in the face of efforts by the bank regulators and other government agencies to encourage banks to increase their lending to precisely these borrowers and communities.”

Do the changes address the problems posed by Silicon Valley Bank?

The Basel III standards pre-date the March 2023 failure of Silicon Valley Bank (SVB). SVB, which had assets of about $200 billion, relied heavily on uninsured deposits, which fled very swiftly, and held a portfolio of bonds that sank in value when market interest rates rose. The proposed capital rules require banks to have capital to account for the risks that loans won’t be repaid, for operational risks, and for trading risks. They don’t directly address the risks to banks posed by rapid increases in market interest rates or inadequate liquidity that were the primary cause of SVB’s woes (along with supervisory failures). But the primary reason that uninsured depositors pulled their money out of SVB is that they feared they wouldn’t get all their money out because the bank was insolvent—which is another way of saying it didn’t have enough capital.

The proposal also would require any bank with assets of $100 billion or more to reflect in their capital calculations any gains and losses in portfolios deemed “available for sale” as opposed to securities the bank plans to hold until maturity. Current rules require that calculation only for bigger banks.

The Fed is expected to propose some new rules on bank liquidity early in 2024.

What happens next?

Regulators had planned to take comments until the end of November 2023, but banks asked for more time, complaining about a lack of transparency and the absence of data justifying the details. In response, regulators extended the comment period until January 16, 2024. “We have already heard concerns that the proposed risk-based capital treatment for mortgage lending, tax credit investments, trading activities, and operational risk might overestimate the risk of these activities,” Fed Vice Chair Barr told Congress in mid-November. “We welcome all comments that provide the agencies with additional data and perspectives to help ensure the rules accurately reflect risk.”

Revisions to the proposal, particularly the operational risk and mortgage-lending provisions, are very likely. Gov. Waller said at an American Enterprise Institute event that he might support the proposals if the operational risk provisions were scaled back. At a March 2024 House hearing, fielding questions from Republicans critical of the proposal, Fed Chair Powell said, “I do expect that there will be broad and material changes to the proposal. I’ll add that I’m confident that the final product will be one that does have broad support, both at the Fed and in the broader world.”

Once the rules are final, changes will be phased in over three years.

Author

Related Content

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

What is bank capital? What is the Basel III Endgame?

March 7, 2024