This post was most recently updated on January 27, 2022.

In response to the economic impact of the COVID-19 pandemic, the Federal Reserve cut short-term interest rates to zero on March 15, 2020 and restarted its large-scale asset purchases (more commonly known as quantitative easing, or QE). From June 2020 to October 2021, the Fed bought $80 billion of Treasury securities and $40 billion of agency mortgage-backed securities (MBS) each month. As the economy rebounded in late 2021, Fed officials began slowing—or tapering—the pace of its bond purchases. The bond purchases are slated to end in early March 2022.

Why does the Fed buy long-term debt securities?

Quantitative easing helps the economy by reducing long-term interest rates (making business and mortgage borrowing cheaper) and by signaling the Fed’s intention to keep using monetary policy to support the economy. The Fed turns to QE when short-term interest rates fall nearly to zero and the economy still needs help.

By buying U.S. government debt and mortgage-backed securities, the Fed reduces the supply of these bonds in the broader market. Private investors who desire to hold these securities will then bid up the prices of the remaining supply, lowering their yield. This is called the “portfolio balance” effect. This mechanism is particularly important when the Fed purchases longer-term securities during periods of crisis. Even when short-term rates have fallen to zero, long-term rates often remain above this effective lower bound, providing more space for purchases to stimulate the economy.

Lower Treasury yields are a benchmark for other private sector interest rates, such as corporate bonds and mortgages. With low rates, households are more likely to take out mortgage or car loans, and businesses are more likely to invest in equipment and hiring workers. Lower interest rates are also associated with higher asset prices, increasing the wealth of households and thus driving spending.

Bond purchases can impact market expectations about the future path of monetary policy. QE is seen as a signal from the Fed that it intends to keep interest rates low for some time. Overall, the large-scale asset purchases that took place during and after the global financial crisis had powerful effects on lowering 10-year Treasury yields.

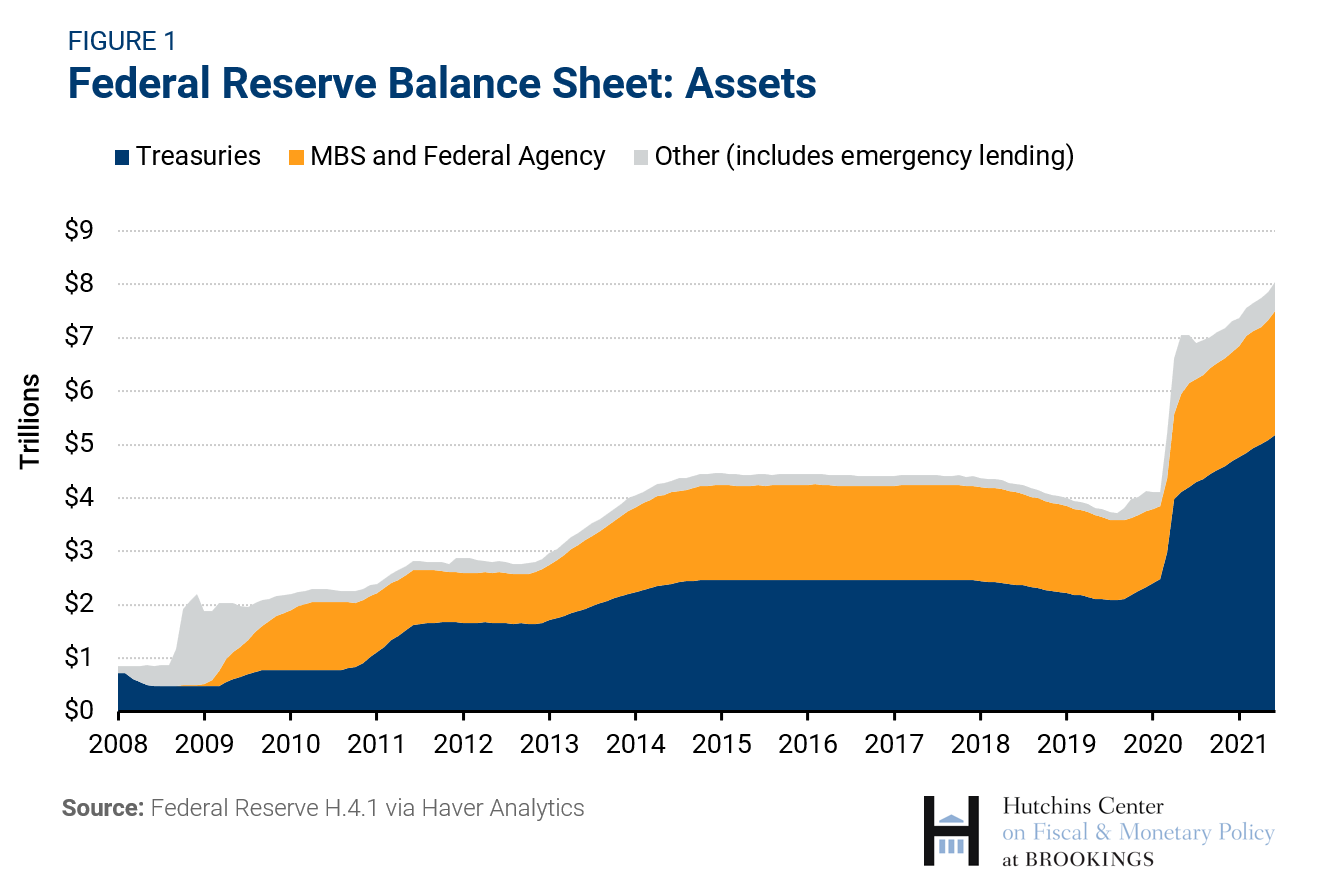

Figure 1 shows the expansion of the Fed’s asset portfolio since 2008.

In the two years following the onset of the pandemic in early 2020, the Fed bought over $4.5 trillion in Treasury and mortgage-backed securities. These bond purchases differed in composition from the Fed’s earlier QE programs. While previous rounds of QE primarily involved the purchase of longer-term securities, during the pandemic, the Fed purchased Treasuries across a broader range of maturities. This was driven by the Fed’s original goal of calming a distressed Treasury market in March and April 2020.

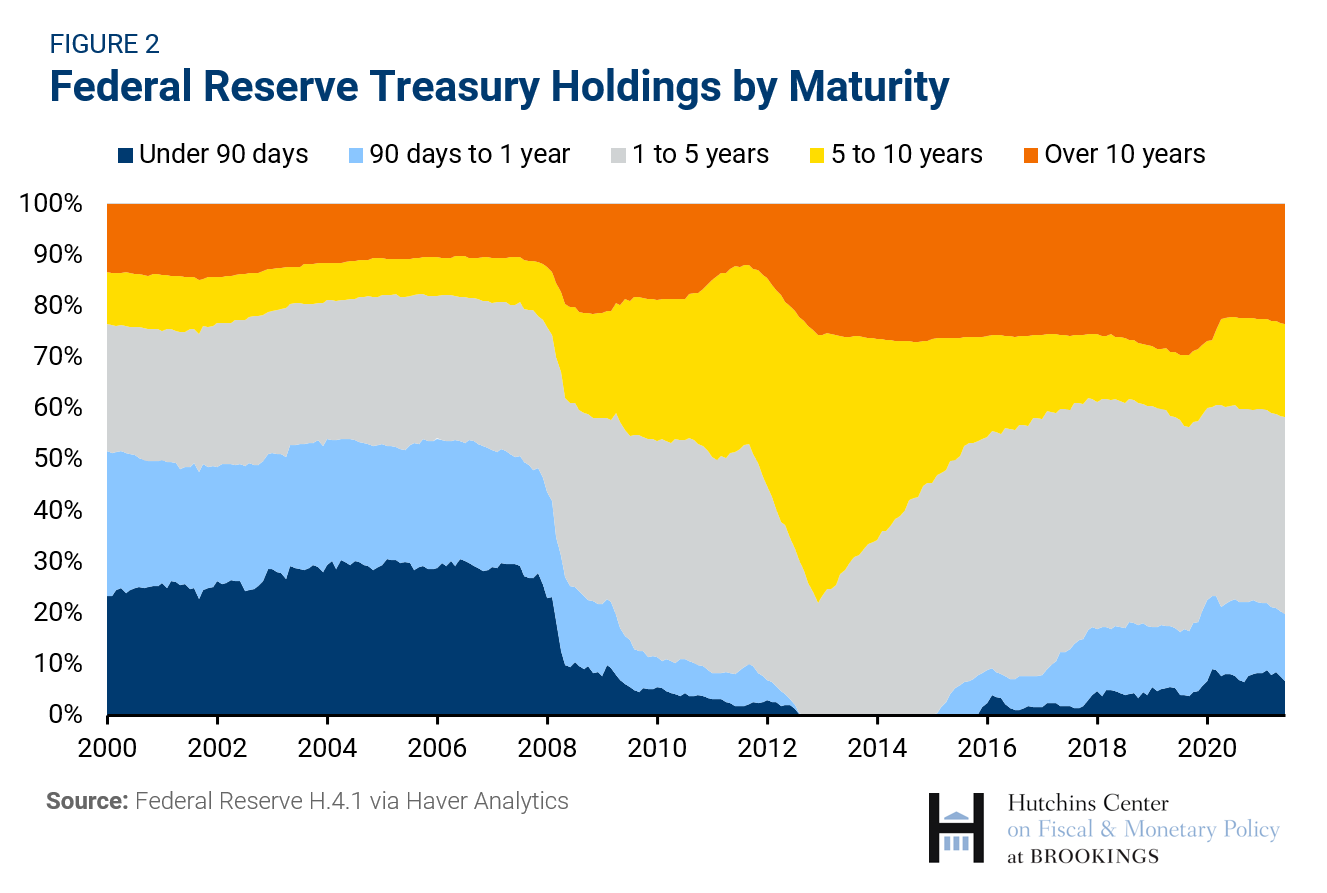

Figure 2 shows the changing composition of the Fed’s Treasury holdings since 2000.

What is tapering?

Tapering is the gradual slowing of the pace of the Federal Reserve’s large-scale asset purchases. Tapering does not refer to an outright reduction of the Fed’s balance sheet, only to a reduction in the pace of its expansion.

The Fed’s motivation for tapering is to slowly remove the monetary stimulus it has been providing the economy. Specifically, according to guidance the Fed issued in December 2020, tapering was to begin once the economy had made “substantial further progress” toward its goals of maximum employment and price stability.

The U.S. economy recovered rapidly from the pandemic in 2021, with strong economic growth, employment gains, and elevated levels of inflation throughout the year. At its November 2021 meeting, the Fed’s policy setting committee, the Federal Open Market Committee (FOMC), decided its taper test had been met. The Fed began reducing the monthly pace of its Treasury purchases by $10 billion and its MBS purchases by $5 billion in November and December. The Fed doubled the pace of tapering at its December 2021 meeting, and Fed Chair Jerome Powell confirmed in January 2022 that the plan is to end asset purchases in early March 2022. This is a faster pace of tapering than occurred under Fed Chair Janet Yellen, when purchases were slowed over a 10-month period between December 2013 and October 2014. This time is different, Powell said at his January 2022 press conference: “The balance sheet is much bigger. It has a shorter duration than the last time. And the economy is much stronger and inflation is much higher.”

The Fed has made clear that tapering will precede any increase in its target for short-term interest rates. So tapering not only reduces the amount of QE, it is also seen as a forewarning of tighter monetary policy to come, as was observed in the aftermath of the Great Recession. The combination of projected reductions in asset purchases and the possibility of higher rates in 2013 led to a period of high volatility and rising rates in the bond market—an episode that became known as the taper tantrum.

What was the taper tantrum?

In response to the global financial crisis, the Fed began purchasing Treasury securities and mortgage-backed securities in 2009. There were three rounds of purchases dubbed QE1, QE2, and QE3. The first two were for pre-announced totals. The third, launched in September 2012, was open-ended; the Fed said it would keep buying bonds until labor market conditions improved.

In Congressional testimony on May 21, 2013, Fed Chair Ben Bernanke gave the first public signal that a taper was on the horizon. “If we see continued improvement and we have confidence that it is going to be sustained, then we could, in the next few meetings, take a step down in our pace of purchases,” he said.

Bernanke’s words, apparently surprising the markets, set off an increase in market interest rates known as the taper tantrum. The bond market pushed 10-year Treasury yields up slightly, from 1.94 percent on May 21 to 2.03 percent on May 22, 2013. Following the June FOMC meeting, Bernanke elaborated on the plan for tapering, and yields rose more substantially, eventually hitting 2.96 percent on September 10. This occurred despite efforts by Bernanke and other FOMC members to emphasize that any reduction in asset purchases would be gradual and that an increase in the Fed’s target for short-term rates was not imminent.

The impacts of the taper tantrum on the U.S. economy were relatively mild, with the economy growing at a rate of 2.6 percent in 2013 (on a Q4/Q4 basis) despite fiscal as well as monetary tightening. But it had greater effects on financial markets abroad where the increase in Treasury yields drove capital outflows and currency depreciations, especially in emerging markets such as Brazil, India, Indonesia, South Africa, and Turkey.

In December 2013, the Fed began to taper, reducing the pace of asset purchases from $85 billion per month to $75 billion per month. Purchases were reduced by a further $10 billion at each subsequent meeting (in February 2014, Janet Yellen took over as Fed Chair). The asset purchase program ended in October 2014, and the Fed began shrinking the balance sheet in October 2017.

How will tapering influence long-term interest rates?

Tapering can impact long-term interest rates through both its direct effects on bond markets and the signal it provides about the Fed’s future policy intentions.

Since tapering refers to the slowing of the Fed’s bond purchases rather than the reduction of its holdings, the Fed’s balance sheet is still growing, and thus the Fed is providing monetary stimulus to the economy. This could restrain any upward pressure on long-term rates from the Fed’s tapering. There is evidence to support this idea: a 2013 study by Fed economists found that the size of the balance sheet is more important than the pace of purchases in lowering long-term yields.

However, long-term rates also reflect market expectations about the course of short-term rates. Since tapering can signal to markets that the Fed is shifting to a less accommodative policy stance in the future, this could lead to a rise in long-term rates, as occurred during the taper tantrum.

The minutes of the July 2021 FOMC meeting indicate that the Fed’s internal models prioritize the stock view of asset purchases. “In the staff’s standard empirical modeling framework, the effect of asset purchases on financial and economic conditions occurred primarily via their influence on the expected path of private-sector holdings of longer-term assets […] Changes in the flow of asset purchases could also influence yields, but this influence would likely be modest outside of periods of stressed financial market conditions.”

The Fed has taken steps to communicate this rationale to the public. In its November 2021 FOMC statement, the Fed added a reference to its “holdings of securities” in describing the effects of its asset purchases. According to the meeting minutes, this language was intended to “make clear that, even after net increases in the SOMA portfolio ceased, the Federal Reserve’s elevated securities holdings would continue to support accommodative financial conditions.”

What will tapering mean for the timing of Fed rate hikes?

Distinguishing short-term interest rate policy from tapering has been a communication challenge for the Fed dating back to the taper tantrum. In 2021, the FOMC repeatedly indicated that tapering would precede any consideration of rate hikes. At his press conference following the November 2021 FOMC meeting, Fed Chair Jerome Powell emphasized this distinction, saying: “Our decision today to begin tapering our asset purchases does not imply any direct signal regarding our interest rate policy. We continue to articulate a different and more stringent test for the economic conditions that would need to be met before raising the federal funds rate.”

The Fed’s test for raising the funds rate, first introduced in the September 2020 FOMC statement, encompassed three conditions. Specifically, the Fed would not raise rates until “labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.” At the November 2021 press conference, Powell expressed the FOMC’s view that the first criterion had not been met, saying “there is still ground to cover to reach maximum employment.”

As inflation proved higher and more persistent in late 2021 than expected, the Fed moved to tighten policy sooner than it had planned. In Senate testimony on November 30, Powell said: “The economy is very strong and inflationary pressures are high, and it is therefore appropriate in my view to consider wrapping up the taper of our asset purchases… perhaps a few months sooner.” Markets interpreted Powell’s comments as a hawkish turn for the Fed, with short-term bond yields rising in anticipation of earlier than previously expected rate hikes.

The December 2021 Summary of Economic Projections (SEP) showed that the median participant in attendance forecasted three quarter-point increases in the federal funds rate in 2022. After its January 2022 meeting, the FOMC updated its forward guidance, saying it will “soon be appropriate” to raise the federal funds rate. The Fed is widely expected to do so at its March 15-16, 2022 meeting.

What happens after the Fed stops buying Treasury and mortgage-backed securities?

At some point after tapering is complete, the Fed is planning to gradually reduce the size of its balance sheet by letting maturing securities “run off” the balance sheet without replacing them, as it did from October 2017 until September 2019.

In January 2022, the Fed said that it plans to “significantly” reduce its balance sheet “over time in a predictable manner primarily by adjusting the amounts reinvested of principal payments received from securities held” as opposed to selling bonds from its portfolio, but did not provide any more specifics as to the size, pace, or composition of these reductions. However, the Fed did say that in the “longer run,” it plans to hold primarily Treasury securities rather than mortgage-backed securities, because it seeks to minimize its role in allocating credit to different sectors of the economy.

At his January press conference, Powell emphasized that the balance sheet reduction would only start after the Fed began raising rates, and that the federal funds rate would remain the Fed’s primary policy tool. He described the balance sheet shrinkage as a process that would be “running in the background” alongside the Fed’s rate hikes.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

What does the Federal Reserve mean when it talks about tapering?

July 15, 2021