Abstract

This paper explores the relationship between slow structural transformation and the growth of the informal sector in francophone Africa, where formal firms and labor-intensive manufacturing have not grown as they did in Asia. We offer a set of explanations associated with the growth of the informal sector. At the same time we consider why formal-sector jobs remain limited, including high formal-sector wages relative to productivity, an unwelcoming business climate, and rent-seeking. High factor costs and policies that concentrate rents into a small number of hands reduce the incentives for modern, international firms to invest, which would provide an engine of modernization for the economy. Those who can neither afford the high input costs nor gain access to rents end up in the less productive informal sector, which necessarily absorbs the large number of new entrants into the labor force. The paper concludes with recommendations for policies that could accelerate structural transformation in francophone Africa.

INTRODUCTION

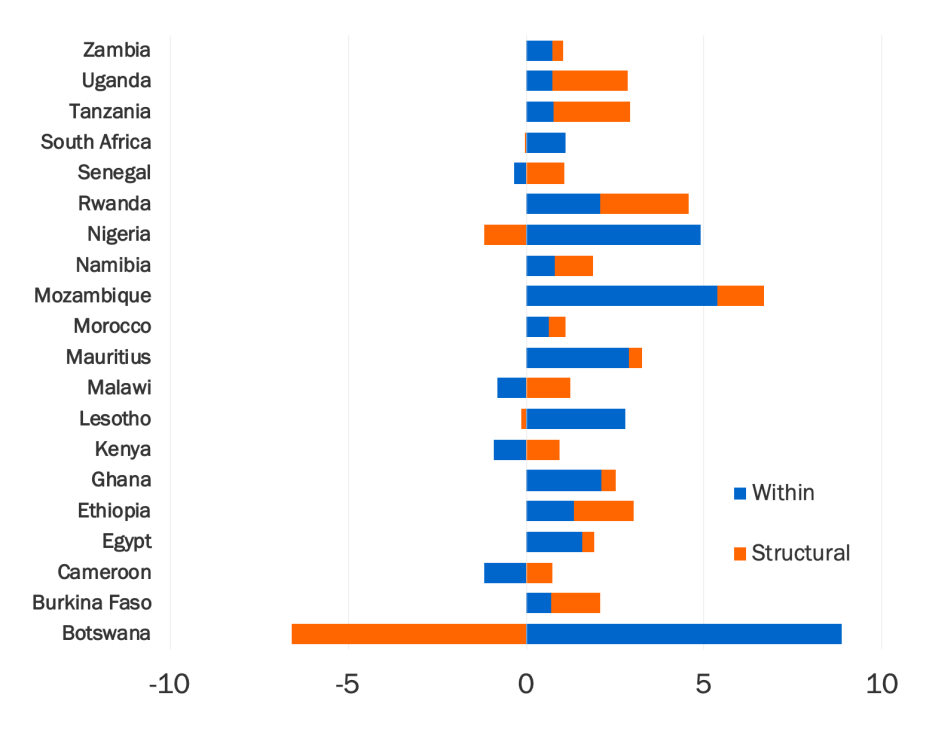

In many developing countries, rapid economic growth and poverty reduction have been the result of successful structural transformation—the shift of production from low to higher productivity sectors, mainly agriculture to manufacturing (Rodrik 2016). In African countries, unlike in Asia, there is little growth attributable to “between-sector” reallocation over the quarter century from 1990-2015; then again, as McMillan et al. 2014 point out, the sub-period of 2000-2010 saw an increase in the contribution of structural transformation to growth in Africa. For most countries in our sample (Benin, Burkina Faso, Cameroon, Senegal), the “within-sector” component of productivity growth is consistently higher than the “between-sector.” For resource-rich countries like Nigeria and Mozambique, growth has been very high but very little structural transformation has occurred over the long run.

Figure 1. Structural change decomposition 1990-2010s

Source: Authors calculation from Penn World Tables (Groningen Growth and Development Center, 2019a).

The transformation that has occurred is a rapid rise in the share of the services sector. Yet, this sector’s productivity is relatively low. One reason is that the service sector is dominated by small, informal firms. In fact, informal firms are the dominant employer in sub-Saharan Africa, accounting for half the value added in the continent, but, notably, these firms are much less productive than formal ones in the same sector.

This paper explores the relationship between slow structural transformation in Africa and the growth of the informal sector. The main reason for the former is that formal firms and labor-intensive manufacturing have not grown as they did in Asia. Several explanations have been put forward for this difference in the development trajectories of the two continents. McMillan et al. (2014) summarize and corroborate the main ones as: (i) many Asian countries, including China, Korea, and Taiwan, continued to protect their import-competing industries while preparing their exporting firms to enter world markets; (ii) these countries followed an undervalued exchange rate policy that favored tradable sectors, whereas many African countries have had overvalued exchange rates for long periods; (iii) many African countries are also natural resource exporters which, due to the Dutch disease, dampens the competitiveness of their manufactured exports.

In this paper, we offer a set of complementary explanations for the growth of the informal sector and lack of structural transformation in Africa: First, the high cost of inputs (electricity, wages, finance) as well as high taxes on businesses make it difficult for most firms to compete in international markets. Second, the few formal firms that survive do so under protection, which generates rents that are allocated to a limited number of beneficiaries. Those who cannot afford the high input costs nor gain access to rents end up in the informal sector, which necessarily absorbs the large number of new entrants into the labor force.

While comprehensive data on the informal sector is lacking, its growth can be inferred from the rise of the service sector. Table 1 shows that the counterpart of the declining share of agriculture in employment in Senegal, for instance, does not show up as a rise in manufacturing’s share but rather as an increase in the share of services. Benjamin and Mbaye (2012) distinguish between large informal firms and small ones because their behavior and obstacles to investment differ markedly. While the vast majority of informal firms are very small, large informal firms play a major role in certain sub-sectors, such as food imports, pharmaceuticals, cement, construction, trucking, and other services. As detailed in case studies in Benjamin and Mbaye (2012), interviews and surveys in West Africa reveal that large informal firms, in particular, usually have fragile structures. They have sizeable sales and a large number of temporary workers but are run like a family firm insofar as they have a small number of permanent employees, no specialized departments—such as human resources or finance—and seldom survive the death of the owner or a falling-out with political patrons. A firm that chooses to be informal in a country with weak regulatory enforcement can become quite large and, as we show below, may have strong incentives to do so.

Indeed, both formal and informal firms need relationships of trust to secure inputs, get credit, and market their products. When formal institutions fail to provide effective property rights, informal firms can, to some extent, internalize these relationships of trust if they are large enough. Sometimes, becoming “large enough” can take the form of informal religious and ethnic networks. These networks can substitute for official institutions that, in developed countries, support arms-length trading in the formal sector (Golub and Hansen-Lewis 2012).

Table 1. Household survey employment estimates in Senegal (percent)

| Sector | Formal/Informal | 2011 | 2015 |

| Agriculture | Formal | 0.8 | 0.3 |

| Informal | 55.1 | 36.1 | |

| Industry | Formal | 2.8 | 1.3 |

| Informal | 10.7 | 7.8 | |

| Trade | Formal | 1.2 | 1.9 |

| Informal | 16.5 | 18.0 | |

| Other services | Formal | 2.5 | 5.6 |

| Informal | 10.3 | 29.0 | |

| Total | Formal | 7.4 | 9.1 |

| Informal | 92.6 | 90.9 |

Source: Senegal Statistical Agency (ANSD 2011, 2015) and authors’ calculations.

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).