Executive summary

President Joe Biden and President Donald Trump will be America’s two presidential candidates in 2024 and their approaches to economic competition with China will prominently feature in the 2024 presidential debate. They each have a body of work over their first term in office to evaluate the results of their policies toward China. On the surface, their approaches are similar. Both presidents view themselves as “self-strengtheners,” leaders who prioritize bolstering America’s economic prosperity. Trump adopted tariffs on Chinese imports and Biden upheld them. There also are some rhetorical through lines in how the Trump and Biden administrations have talked about economic competition with China.

Beyond these superficial similarities, however, the two leaders have differing visions for how to strengthen America’s economic competitiveness vis-à-vis China. Trump favors a protectionist approach of ratcheting up tariffs on China to compel Beijing to make concessions, including by increasing purchases of American products to shrink the bilateral trade deficit. Trump also supports efforts that incentivize multinational companies to exit China and return to the United States, or at a minimum, shift supply chains outside of China. Biden advocates working with allies and investing at home to put America on a stronger economic footing to outcompete China.

As the 2024 election season ramps up and Trump and Biden renew their debate over U.S.-China trade issues, it is worth examining the choices both leaders have made and what results those choices have generated. Based on available data, Biden’s approach has delivered greater relative gains, leading to an expansion of America’s lead in the overall economic size compared to China. Trump’s term, by contrast, was defined by a trade war that came at a heavy cost to the American economy, leading eventually to a U.S.-China phase-one trade agreement that underdelivered on its promise.

Trump’s approach to China trade

When he first ran for president in 2016, Trump warned, “We can’t continue to allow China to rape our country.” He explained that America’s manufacturing sector was being hollowed out and workers were losing jobs because China was engaged in the “greatest theft in the history of the world.” He assured voters that he would draw upon his negotiating skills to get a fairer deal for American workers. He centered his approach to China around trade.

Trump sought to compel China to significantly increase its purchases of American products and make structural changes to its state-led economic model. Trump believed these outcomes would erase America’s trade deficit, boost American manufacturing, and create abundant jobs for American workers.

Early in his term, Trump laid out a four-part plan to secure Chinese trade concessions: declare China a currency manipulator; confront China on intellectual property and forced technology transfer issues; press China to end export subsidies and improve labor and environmental standards; and lower America’s corporate tax rates to attract investment into America’s manufacturing sector. When those efforts failed to move Beijing, Trump announced plans to impose tariffs on more than $550 billion of Chinese products, and China retaliated with tariffs on more than $185 billion of U.S. goods. Over his four years in office, the objects of Trump’s ire in relation to economic competition with China fluctuated between the trade deficit, Huawei, TikTok, and other issues that he would often introduce via his Twitter account. U.S.-China trade negotiations proceeded in fits and starts, reflecting in part Trump’s personalistic direction of the process.

The ensuing trade war cost the U.S. economy nearly 300,000 jobs. The tariffs served as a regressive tax on imported goods that were primarily borne by American consumers. Research from the Federal Reserve Bank of New York and Columbia University found that U.S. companies lost at least $1.7 trillion in stock value from U.S. tariffs on Chinese imports.

Trump succeeded in bringing down the bilateral trade deficit with China. America’s deficit with China totaled $311 billion in 2020, down sharply from its peak of $419 billion in 2018. However, Trump’s China tariffs did not lower America’s overall trade deficit. Instead, the U.S. global trade deficit over the four years of Trump’s presidency soared. The combined U.S. goods and services trade deficit spiked to $679 billion in 2020, compared to $481 billion in 2016, immediately prior to Trump’s inauguration. In other words, America’s trade deficit hit a record high under Trump’s watch, increasing about 21 percent.

The deficit soared under Trump because it is a function of macroeconomic factors, namely how much a country spends and saves. By enacting significant tax cuts and running a large budget deficit, Trump essentially guaranteed an expansion in America’s overall trade deficit. Put differently, the United States spent more than it produced during Trump’s time in office, resulting in the rising trade deficit.

Trump’s tariffs on China reduced imports directly from China but led to a large increase in imports from economies adjacent to China in global value chains, such as Vietnam, Mexico, Thailand, South Korea, Malaysia, and others. Placing tariffs on China diverted trade flows but did not lead to large-scale import substitution with domestically produced goods.

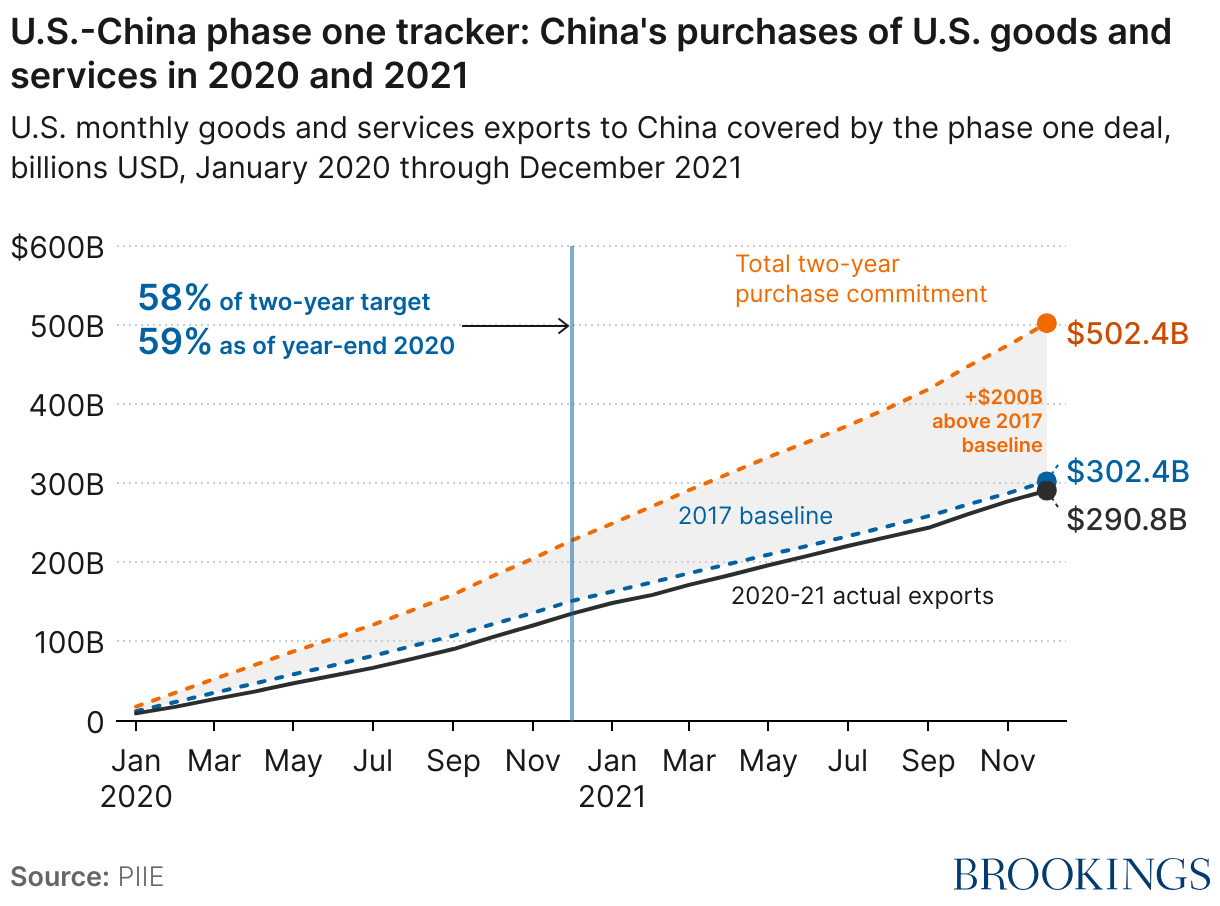

Furthermore, Trump’s phase-one trade deal did not deliver. The deal was premised on a promise that China would increase its purchases of U.S. goods and services by $200 billion above 2017 levels over two years. Those purchases did not materialize. The deal also lacked any forward movement on key structural issues in China’s economy, such as China’s subsidies and preferential treatment for its national champions over foreign competitors. Those issues were punted to a phase-two trade negotiation that never began.

These facts notwithstanding, proponents of Trump’s China trade policy credit Trump with breaking the long-standing trajectory of U.S.-China economic relations. They commend Trump’s efforts to halt the rise in the U.S.-China trade deficit and to hold China accountable for its predatory economic behavior, even if such efforts failed to alter China’s underlying economic practices. Proponents also applaud Trump for helping knock China’s economic ascent off course, even though the size of China’s economy relative to America’s grew during Trump’s time in office.

Trump’s supporters demonstrated a willingness to take an economic hit in service of punching back against unfair Chinese economic practices.

Although Trump’s China trade policies did not deliver the economic windfall he had promised, they did benefit his political standing. A new report by David Autor, Anne Beck, David Dorn, and Gordon Hanson demonstrates how Trump’s tariffs increased his vote share in trade-exposed heartland communities, even though it did not deliver economic benefits or expand manufacturing employment in these regions. Trump’s supporters demonstrated a willingness to take an economic hit in service of punching back against unfair Chinese economic practices. These results are matched by the assessments of political experts, who believe Trump’s break with the free-trade orthodoxy of the GOP since Ronald Reagan helped him make inroads with workers in America’s industrial heartland, thereby broadening the Republican Party’s base of supporters.

The Biden administration’s approach

During the 2020 presidential campaign, Biden slammed Trump’s approach to China trade issues. He blamed Trump’s tariffs for hurting American farmers, manufacturers, and consumers. He agreed that America needed to get tough to curb China’s “abusive” economic behavior but argued that Trump’s approach was the wrong way to do so.

Upon entering office, the Biden administration’s critique of the Trump-era trade policy was that Trump fixated too narrowly on the trade deficit, he lacked a domestic competitiveness dimension, and he was too protectionist and unilateral. A more effective approach, the new administration argued, would be to build support from allies and partners to address specific Chinese actions of concern and to invest at home in the sources of American economic competitiveness.

Over the past three years, the Biden administration has effectively enlisted partners to enhance the impact of their policy efforts directed at China. They have strengthened coordination in overall competition with China through a range of groupings, including the G7, the Australia-India-Japan-United States quadrilateral grouping, the Australia-United Kingdom-United States AUKUS alliance, the U.S.-European Union Trade and Technology Council, and through Japan-South Korea-United States trilateral cooperation.

As a subset of such efforts, the Biden administration has strengthened coordination on technology export controls with key stakeholders. The most notable example has been the harmonization of export control requirements for semiconductors and their production with Japan and the Netherlands. Together, Japan, the Netherlands, and the United States control key chokepoint technologies that are required for the production of advanced semiconductor chips. Without access to these chokepoint technologies, China is limited in its ability to produce cutting-edge chips at a yield that would make production commercially viable. China has vowed to overcome this obstacle, but even if it does so, it will come at considerable cost and time.

The Biden administration’s catchphrase for its China policy has been to invest at home, align with allies, and compete responsibly with China.

The Biden administration’s catchphrase for its China policy has been to invest at home, align with allies, and compete responsibly with China. The second leg of this stool, aligning with allies, has been hampered by the absence of a trade strategy in Asia. The Biden administration’s flagship effort for weaving together America’s economic partners in Asia—the Indo-Pacific Economic Framework (IPEF)—has been an underwhelming effort to synchronize economic practices in the region. The IPEF negotiation on the trade pillar went into an indefinite pause in November 2023 when congressional Democrats voiced their opposition to it. It was an event that hardly attracted notice outside of the negotiators involved in it, given the lack of enthusiasm the initiative had generated in the region prior to being shelved. Until the Biden administration develops a trade strategy and sells it to the American people, the United States will continue to underperform in its international trade strategy, and not just with China.

Beyond its ambivalence on trade, the Biden administration has reframed America’s economic competition with China. Biden has shifted from a narrow focus on the trade deficit as a measure of success to an approach that seeks to harness competition with China to galvanize greater domestic investments in American competitiveness. The Biden administration has made the case to Congress and the American people that the United States needs to make generational investments in American innovation to outcompete China. The result has been over $2 trillion in investments in clean energy technology, infrastructure, semiconductors, and advanced manufacturing through the Inflation Reduction Act, the CHIPS and Science Act, and the Infrastructure Investment and Jobs Act.

The Biden administration also has coalesced with partners around the concept of “de-risking” from China. It argues that it is prudent and wise for the United States to increase domestic production capacity and diversify value chains to avoid dependency on China for critical inputs for America’s health and development. The administration also believes the United States must take more protective actions to guard against American technology being used by China’s military to threaten the security of the United States and its allies, or by China’s security services to violate American values through human rights abuses.

Guided by these concerns, the Biden administration has gone further than the Trump administration in enacting technology export controls, prohibiting the importation of goods made with forced labor, and developing an outbound investment screening mechanism to complement the existing inbound investment screening mechanism.

Outside these areas of concern, the Biden administration has argued that the United States and China should work jointly to build a constructive and fair economic relationship. Secretary of Treasury Janet Yellen has identified three pillars for the economic relationship: protecting national security; seeking a healthy economic relationship that fosters growth and innovation in both countries; and seeking cooperation with China on urgent global challenges.

In an apparent nod to the political salience of Trump’s tariffs, the Biden administration has not removed or lowered the China tariffs it inherited. Even though the tariffs are inflationary, and despite the fact that Biden and members of his team slammed the tariffs during the 2020 election campaign, the tariffs remain in place. This constancy likely reflects Biden’s political instincts. Even if he lacks conviction on the policy merits of sustaining the tariffs, Biden recognizes that removing them would carry greater political costs than benefits.

Biden’s approach thus has been to limit exports of high-technology goods with national security applications to China, maintain Trump’s tariffs, tighten coordination with allies and partners on China, and leverage competition with China to unlock investments at home. This approach has contributed to some notable wins for the American economy.

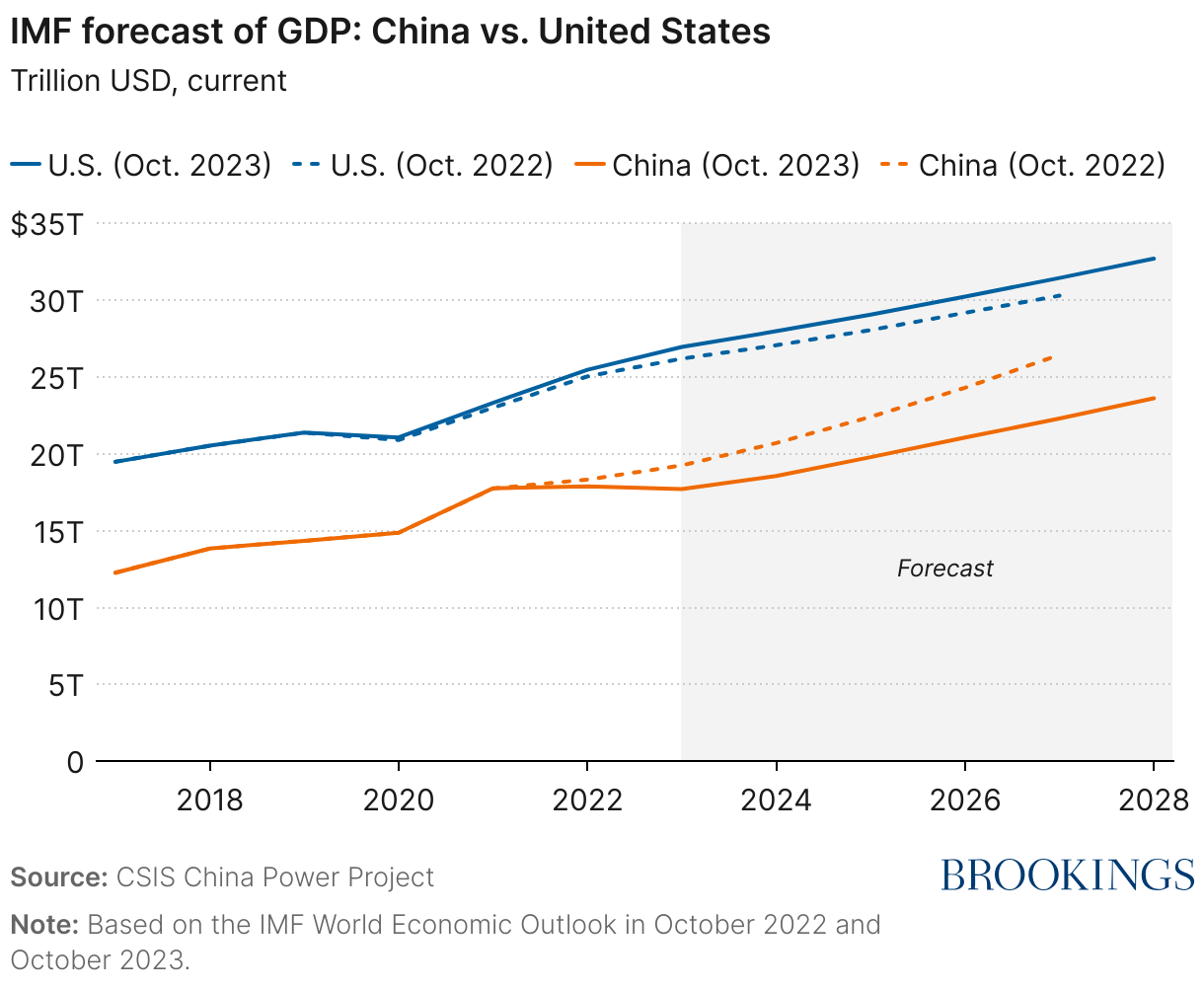

For example, the gap in size between the Chinese and American economies (in dollar-adjusted terms) has grown in America’s favor in recent years, after a prolonged period when China was narrowing the gap. In real terms, China reported growth of 5.2 percent in 2023, with its economy growing from 120 trillion yuan to 126 trillion yuan. However, when converted into dollars at market exchange rates, China’s GDP fell from $17.96 trillion to $17.71 trillion in 2023. In analogous terms, the U.S. economy grew from $21.8 trillion in 2022 to $22.3 trillion in 2023, marking growth of 2.5 percent year-over-year.

Similarly, China experienced a net outflow of foreign direct investment in 2023. According to the Financial Times, China’s 2023 foreign direct investment dropped 82 percent year-on-year and was the lowest figure since 1993. By comparison, the United States was the world’s largest recipient of foreign direct investment in 2023. The influx of foreign capital was particularly pronounced in manufacturing production capacity, as many foreign multinational companies sought to profit from America’s investments in its own commercial upgrading through the CHIPS and Science Act and the Inflation Reduction Act.

A similar story applies to high-skilled immigration. Record numbers of Chinese citizens are leaving the country in search of freedom and opportunity abroad. Meanwhile, a surge of immigration into the United States is providing an estimated $7 trillion stimulus to the U.S. economy.

U.S. companies also control the commanding heights of the global economy. In 2023, nine of the world’s 10 largest companies by market capitalization are American. None is Chinese. The largest Chinese company by market capitalization is Tencent, which ranks 26th on the list of the world’s largest companies. Additionally, American-based companies are driving global innovation, particularly in artificial intelligence and related sectors. Their lead over global competitors in this space is large and growing. Chinese companies are strong in electric vehicles, batteries, and clean energy technologies. Even so, China’s benchmark CSI 300 stock index fell 11 percent in 2023, whereas America’s benchmark S&P 500 stock index closed the year up 26.3 percent. Since 2021, China’s stock market indices have lost over $6 trillion in value. During this same period, the U.S. stock market has added over $5 trillion in value.

And although the Biden administration has not focused on the trade balance as a measure of the U.S.-China trade relationship as Trump did, the trade deficit in 2023 shrank to its lowest level since 2010. The U.S.-China trade deficit now stands at $279 billion, compared to $311 billion in Trump’s final year in office. It is worth noting that the COVID-19 lockdowns were a major exogenous event in the final year of Trump’s term that impacted this data. Nevertheless, this is the best data available for purposes of comparison.

Looking forward

The 2024 presidential election debate on China trade issues will feature two contrasting visions for how best to compete economically with China.

Biden will make a case that his strategy is showing results. He will note that he kept in place all the tariffs on China that Trump enacted and went further than Trump in terms of new export controls, investment screening, and other protections for American workers. He will argue that America’s economy is in a stronger relative position today due to the significant investments that Congress passed under Biden’s watch, investments that were galvanized in large part by Biden’s argument that they are needed to compete with China. He will suggest that it is wiser to work with partners in confronting China’s predatory economic practices than it is to do so alone, as Trump did. These actions align with voter preferences. Recent polling shows that a clear majority favor a “smart, firm, strong, and diplomatic” approach, with 73 percent of respondents saying the United States should hold high-level diplomatic talks with China.

At a broader level, Biden will make a case that he has been tougher on China than Trump was, in part because he confronted China on the wide range of its transgressions, from Xinjiang, Hong Kong, and human rights abuses to China’s military pressure on Taiwan, the Philippines, and others. Biden will seek to contrast what he will describe as his firm but responsible approach to China with Trump’s blustery and erratic approach and his narrow pursuit of a trade deal that ultimately underdelivered. He will chide Trump for his fawning praise of Xi Jinping and contrast Trump’s flattery of Xi with his own assertion that Xi is a “thug” and a “dictator.” He also will continue to roll out new measures throughout 2024, such as on data security and protections against Chinese electric vehicles, to protect American workers against China’s efforts to export its way out of its economic slowdown.

It is possible that Biden may seek to play offense on China issues, arguing that his administration’s tough but smart approach is helping America “win” the race against China. More likely, many of Biden’s arguments will be in response to Trump’s attacks on Biden’s record on China. Biden would much prefer the 2024 election to be a referendum on Trump’s fitness to hold the office of the president than on the fine points of each candidate’s economic policy approach to China.

By contrast, Trump will be on the attack on China trade issues. He will argue that Biden’s approach to China has been too weak. Trump will not allow Biden to neutralize China as a topic of debate. He will continually outflank Biden on China economic issues. For Trump, China is too potent of a political weapon to be left unused.

Already, Trump has floated the idea of imposing a 60 percent flat tariff on all Chinese imports. According to Bloomberg Economics analysis, such an action would diminish a current $575 billion trade flow between the United States and China down to nearly nothing. The Bloomberg Economics model shows that Southeast Asia and Mexico would be the biggest beneficiaries, as value chains would shift to these places if prices of Chinese goods shot up 60 percent.

Privately, Trump’s advisors accept that such an action would increase the prices of imports, but they argue that the cost would be worth it because China’s overall economy would take a larger hit than America’s from the tariffs. Advisors to Trump such as Ambassador Robert Lighthizer believe that such steps are needed to restore America’s manufacturing base and to dull the threat that China poses to the United States. They will try to put Biden on the defensive by challenging him to explain why he hasn’t taken such bold steps to protect American workers and undermine China’s economic competitiveness.

Regardless of whether Biden or Trump prevails in the 2024 election, America’s economic policy toward China likely will grow tighter, rather than looser.

Regardless of whether Biden or Trump prevails in the 2024 election, America’s economic policy toward China likely will grow tighter, rather than looser. Biden and Trump both are likely to crack down on Chinese state-backed economic espionage. There will be heightened scrutiny of Chinese investments into the United States, and of American investment flows into Chinese companies that develop dual-use civilian and military technologies. Export control screening likely will grow tighter. Tariffs will remain in place and could rise. There will be greater emphasis on supply chain resiliency over economic efficiency.

Where there would be differences, however, is on the desired scale of U.S.-China economic disentanglement. Trump would favor broad-based decoupling and would be willing to tolerate high costs in pursuit of such a goal, whereas Biden likely would focus on targeted de-risking in areas of the economy that have national security or human rights nexuses, but not on full-scale decoupling of the world’s two largest economies. Trump likely would take a more expansive view on scrutinizing ethnic Chinese researchers in the United States to determine if they are spying for Beijing, whereas Biden would argue for protecting civil liberties. Biden would place more emphasis on sustaining coordination with allies in confronting Chinese transgressions whereas Trump would be more willing to increase unilateral pressure on China. Biden also would continue to leverage public concern over China’s advances to promote greater domestic investments in basic and applied research, America’s leading technology sectors, and its infrastructure build-out.

In sum, there will be a debate during the 2024 election over how America should address the challenges posed by China’s economic practices. Trump will highlight how he pivoted America to confront China’s unfair economic practices. Biden will counter that he converted Trump’s bluster into a more coherent strategy that has put the United States in a stronger competitive position vis-à-vis China, pointing to America’s expanding lead in overall economic size as proof that his approach is paying off.

This debate will occur against the backdrop of a changing macroeconomic policy landscape. There no longer is a widely accepted theory of the case for how the United States should relate economically to the rest of the world. The American public no longer embraces the idea of free trade opening new opportunities for U.S. corporations to compete on the world stage. Following the COVID-19 experience, there is greater awareness of the risk of dependency on rivals for critical economic, energy, or public health inputs. This has led to rising support for supply chain resiliency, even if such a pursuit reduces economic efficiency.

Underneath these arguments lies a more fundamental question: What economic policies on China would best protect American workers and advance American prosperity? Which leader would best position the United States to outcompete China over the coming century?

Given the large number of other issues that will compete for attention in the 2024 election, such as immigration, Russia’s invasion of Ukraine, Israel-Palestine, the economy, and crime, there may not be much space left for detailed debate to resolve specific policy differences around America’s economic approach toward China. The debate on China likely will be loud and emotional and proceed along multiple fronts, including trade, security, diplomatic, and military issues. Even so, the choice American voters make in selecting their next president will have a major impact on which path the United States takes to compete with China.

Biden’s and Trump’s differing strategies and records for competing economically with China will present American voters with a real choice. The available data suggests that Biden’s economic policy approach to China has generated better results for the American economy. Voters are not always guided by rational calculations of self-interest, though, and China policy is unlikely to be a determinative factor for many voters.

Pundits often claim every election is the most important election in a generation. In the case of China policy, they may be right this time.

Author

Related Content

-

Acknowledgements and disclosures

The author wishes to thank senior research assistants Louison Sall and Kevin Dong for their research support for this piece, two blind reviewers for their constructive feedback, Adam Lammon for editing, and Rachel Slattery for layout.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How will Biden and Trump tackle trade with China?

April 4, 2024