Generative artificial intelligence (genAI) has burst onto the scene, contributing to a bump in stock prices of big tech companies and raising hopes for a transformation of the economy, a new era of faster growth, and, perhaps, rising incomes. At the same time, it has raised concerns about widespread job losses, while some see the new technology as largely hype. In this explainer, we will look at what we know about the prospects of artificial intelligence (AI) for the workforce, businesses, and the overall economy. Could this technology power future growth through improved productivity?

What is productivity and how do we measure it?

Productivity is defined as the ratio of economic output to the inputs required in production. It is a measure of the efficiency of production. The simplest productivity measure is output divided by hours of labor called labor productivity. Labor productivity growth has been slow in recent years, running at about 1.5% per year, compared to over 3% a year in the early 2000s.1 Other inputs to production (especially capital) can also be accounted for and allow an estimate of total factor productivity growth, a measure of the growth contribution of technological progress.

Long-term economic growth is largely driven by productivity growth, which improves living standards and can improve the well-being of consumers, producers, and workers. Initially, productivity growth leads to lower costs and higher profits for firms. In competitive markets, these gains should be passed through to consumers in the form of lower prices and to workers as higher wages.

Unfortunately, in practice the limited productivity gains that have occurred have not helped many workers, leading to a productivity-pay gap. One estimate shows that productivity has grown 3.5 times faster than pay for the typical worker from 1979 to 2021. Productivity gains over the past 40 years have primarily gone to higher-paid, higher-skilled employees and corporate profits.

Historically, technological progress has been the main source of productivity growth, coming from scientific advances, improved managerial practices, better organizational structures, new products and services, and new business models. Despite the proliferation of new technologies, like the internet and smartphones, the contribution of total factor productivity growth has been very low for the past two decades. Increases in the amount of physical capital and improvements in the education of the workforce have continued as modest sources of productivity growth, but a return to faster technological progress is badly needed to boost economic growth and living standards and to sustain the incentive for business investment.

Why has productivity growth been so slow?

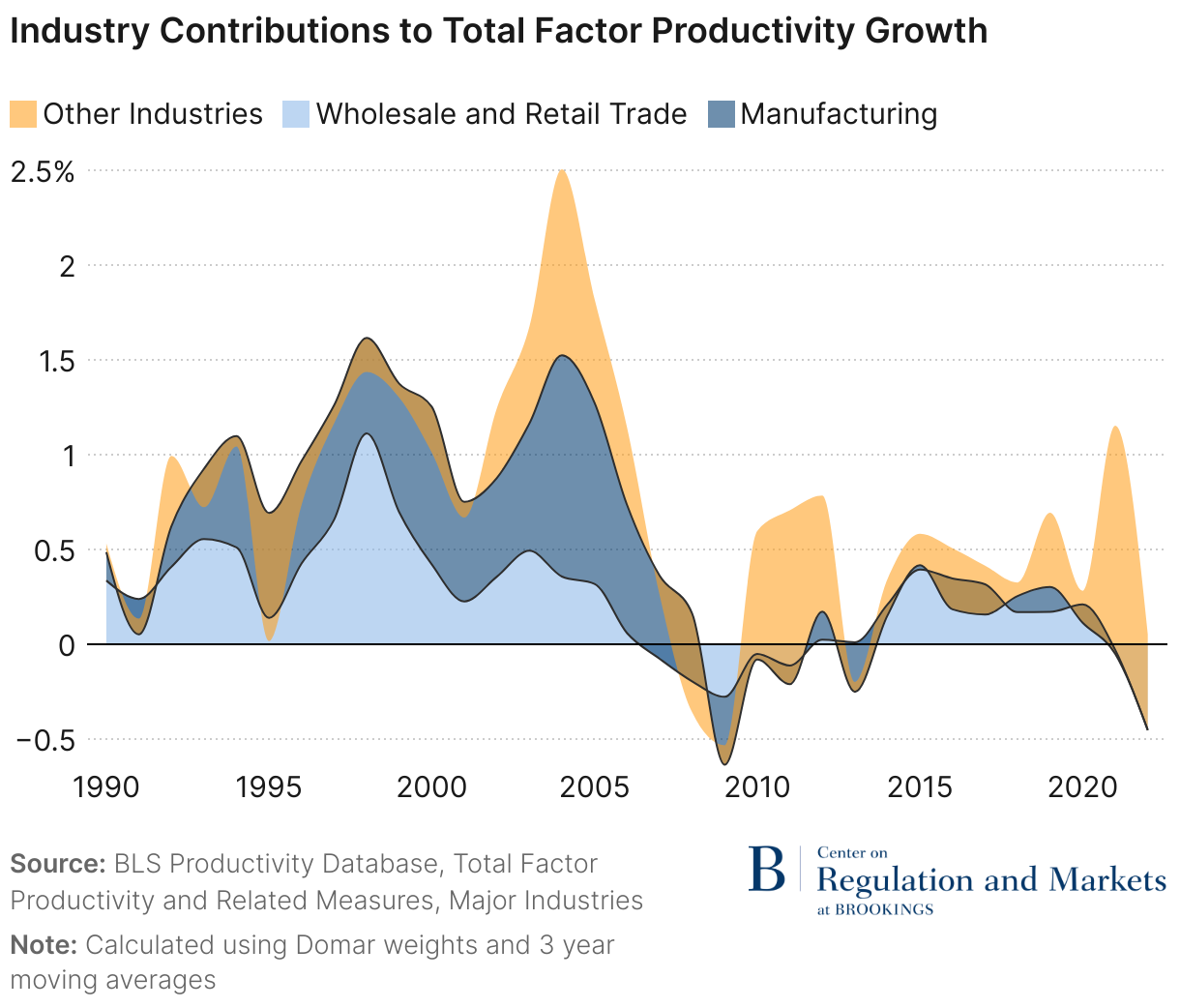

In the past, the industrial sector, particularly manufacturing, has been a major source of productivity gains. Efficiency improvements in most manufacturing industries has drastically slowed, but for a while computers and electronics picked up the mantle and kept manufacturing productivity growing. As “Moore’s law”—the seemingly inexorable climb in electronics performance—has proven harder to sustain, even productivity gains in this industry have slowed.

Wholesale and retail trade has also contributed to productivity growth. Stiff competition among large companies like Walmart, Kroger, and Costco forced the industry to consolidate and speed distribution and point-of-sale efficiency. These gains also have faded, unfortunately, despite the revolution in online retail.

The figure above illustrates the contributions total factor productivity growth in the business economy from wholesale and retail trade, manufacturing, and all other industries. Three-year moving averages are used to smooth out very short-term variations, although a lot of variability remains. From the 1990s through 2008, manufacturing and wholesale and retail trade contributed the most to productivity growth. Around 2007, however, productivity growth in manufacturing and trade fell dramatically and has not recovered. During this period, other industries contributed more to productivity growth, namely finance, insurance, real estate, leasing (from 2009 through 2013), and information and services (from 2015 onwards). The total contributions from these other industries were not enough, however, to drive much growth overall.

One explanation for slow productivity growth is that we are running out of ideas, although this view runs counter to the constant release of new technology and new products. Accounting for changing innovation in productivity data is difficult, which could explain the slow productivity growth. Health care (over 17% of GDP) is an example where very little of the advance in medical technology is captured in the productivity data. The likely main explanation for slow growth is the type of innovations have not changed the way offices and factories operate.

Will AI improve productivity?

Artificial intelligence has been around for years, but recent advances have triggered massive investments and a range of new applications. Generative AI emerged through key breakthroughs such as the novel “transformer architecture,” coupled with massive amounts of computing power made possible by advanced AI chips. This meant that the techniques of data mining and trial and error became extraordinarily powerful. A sample of what AI is already doing in companies includes checking for anomalies in hard disks, assisting with legal and compliance analytics, and fraud detection. These and many other examples are described in Davenport and Mittal (2023).

There is evidence that generative AI can improve the productivity of less-skilled employees within an occupation or organization. Case studies show that genAI increased productivity of call center customer support agents, software developers, and mid-level professionals.

There are also intriguing examples of AI contributing to scientific advancement. A team of physicists at Princeton used AI to control the plasma in their fusion reactor. AI has helped scientists understand how proteins fold, a key step in improving the understanding of biological processes. If AI can contribute to faster scientific advancement, this will add to productivity growth on top of the direct use of AI in businesses.

In the area of health care, AI can read scans and point out problems. Given lab and examination results, it can suggest diagnoses and treatment protocols. It can reduce the paperwork burden by summarizing doctors’ notes and preparing insurance claims. Reducing the cost of health care would have a massive benefit to the economy regardless of how well that is captured in the productivity statistics.

AI is having an impact now, but most of its effects will occur in the future and are uncertain. To get at the potential for AI-driven productivity improvements ahead, AI can be compared to past major technology breakthroughs. Economists use the term general purpose technology (GPT) for an innovation that has widespread application across the economy, shows sustained improvement in its own performance, and generates innovations in the industries using the GPT. Past GPTs (such as electric motors and personal computers (PCs)) have generated broad productivity growth. Because it is relatively easy to use and adapt to many applications, it is likely that AI will be a GPT and thus can be expected to generate broad productivity improvement ahead.2

How can policy affect AI’s impact on the labor market?

The AI revolution is coming, and America needs to embrace what the technology can do for productivity while recognizing its dangers and putting policies in place to ameliorate the negatives.3 The policy issue we focus on here is that AI may displace workers and push them into lower-paid positions as production shifts away from relying on human labor and more on automation.

Previous technological advances have been skill-biased, where high-skill workers experienced wage gains because of productivity improvements while people in lower-skilled jobs, where tasks are repetitive, experienced job losses and decreased real wages due to automation. GenAI could automate a significant portion of a job’s tasks, leading to potential job losses in occupations affected the most.

Even if the effort to steer AI towards augmentation is successful, some jobs will likely be lost. Looking at the past, agriculture and manufacturing are two sectors where productivity growth has been rapid and in both cases, the share of employment in these sectors has dropped a lot. Despite job disruptions, though, U.S. unemployment has generally been low and remains very low today.

The depth and breadth of job losses will depend on whether employers embrace job retraining, which could be supplemented by government training programs. As our colleague Harry Holzer has written, the U.S., a $25 trillion economy with 150 million adult workers, spends less than 0.1% of GDP on workforce development. The U.S. spends a fraction of what other countries spend, particularly the European Union, on “active labor market policies,” which are other countries’ version of workforce development.

As well as a cause of job displacement, AI and related technologies could be part of the solution by providing better options to train workers with new skills, particularly in the technology sector. For example, Khan Academy, a nonprofit that offers free courses to help students, is now working closely with OpenAI to implement a genAI tutoring system. Government training programs can learn from the private sector on how to use AI to enhance learning both for youth trainees and in retraining older workers.

America is a leader in the development of AI and, while there are dangers involved, there is the potential for AI to enhance productivity and increase economic growth.

Authors

-

Acknowledgements and disclosures

We have been studying AI and productivity with David Byrne, whose insights have been invaluable. Michael Chui of the McKinsey Global Institute has helped our understanding of AI.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

-

Footnotes

- Data on productivity is available from the Bureau of Labor Statistics (BLS) Productivity Database.

- See, for example, Goldfarb, Taska, and Teodoridis (2022).

- Dangers to the political system and concerns about bias and racism are considered by our Brookings colleagues Bell and Korinek (2024) and Lee and Cummings (2024).

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How will AI affect productivity?

May 2, 2024