The sudden halt in commerce across the United States over the past two weeks due to the coronavirus has placed millions of small businesses in peril, and tested the capacity of the private sector and governments at all levels to deliver relief as the economy freezes in place. As Annie Lowrey wrote in The Atlantic, “This is not a recession. It is an ice age.”

Local policymakers—and the collaborative private and nonprofit networks that support them—do not plan for ice ages. But they are admirably stepping up in this time of crisis with novel small business stabilization solutions. This brief is designed to guide them through the economic and policy uncertainty surrounding the COVID-19 small business crisis by offering insights in three areas:

- What is the scale of the problem, by estimating the number of businesses that are at risk of closure in the immediate and near term, both nationwide and in counties, metro areas, and states.

- What is the scale of the federal relief, by reviewing the small business provisions embedded in the CARES Act.

- What local policymakers should do now, by outlining how small business support providers can provide awareness, technical assistance, and immediate liquidity for small businesses.

What is the scale of the problem?

To answer this question, we segmented industries into three categories: immediate risk, near-term risk, and long-term risk, drawing on consulting industry risk analyses from Moody’s and the Boston Consulting Group, as well as news sources on which industries have been most affected.

Any way we segment the numbers, the scale of the problem is enormous. Importantly, this is not a definitive prediction of the number of small businesses that will close and the number of jobs that will be lost. Rather, it gives policymakers a sense of the magnitude, key sectors, and timeline for vulnerabilities.

Nationwide, about 26% of small business establishments (those with fewer than 250 employees) are in the immediate risk category (2 million small businesses), which collectively employ about 27.5 million Americans. If you add the small businesses in the near-term risk category, another 28% of small businesses and 20.3 million more jobs are vulnerable. Combined, these two categories include 54% of small businesses (4.2 million total) and 47.8 million jobs. One-quarter of these jobs and about 16% of these establishments are in the hard-hit bars and restaurant sector.

In terms of vulnerability, we know that the smallest businesses are least liquid. Microbusinesses (employers with fewer than 10 employees) within industries at immediate or near-term risk account for 2.9 million business establishments and 8.7 million jobs. This is about 70% of small businesses in the immediate or near-term risk categories, but a smaller portion of overall small business jobs in those categories (18%).

Due to industry variation across the nation, counties, metro areas, and states differ in their exposure to the COVID-19 small business crisis. U.S. states vary in the share of their small business establishments in the immediate and near-term risk categories, from Washington, D.C. on the low end (38% of establishments and 41% of jobs) to North Dakota on the high end (60% of establishments and 58% of jobs).

In general, the larger the metro area, the lower the share of small business establishments in immediate risk industries (Table 2). Smaller communities—known as micropolitan areas—have about 29% of their business establishments in immediate risk industries, compared to 25% in the largest metro areas.

These averages mask metro-area-level variation. In Ocean City, N.J.—a summer tourist destination—71% of small business establishments and at least 59% of jobs are in industries at immediate or near-term risk. At the other end of the spectrum, those numbers for Boulder, Colo. are 43% and 44%, respectively. Even at the low end, that is tremendous exposure.

Most communities find themselves somewhere in the middle. Take Cuyahoga County, the largest county in Greater Cleveland: Half of small business establishments are in immediate or near-term risk industries—about 16,000 businesses that together employ around 190,000 workers. Of those establishments, about 11,000 have fewer than 10 employees. At its narrowest, there are about 5,000 businesses with fewer than 10 employees that are in immediate risk industries—these are restaurants, gyms and fitness studios, and main street retailers.

What is the scale of the federal relief?

The CARES Act was signed into law on March 27, providing $2 trillion in much-needed public health and economic relief. This brief studies the three programs that provide relief to small businesses, focusing mainly on the Paycheck Protection Program and SBA Economic Injury Disaster Loan program. More details are in this useful overview.

- Paycheck Protection Program: This program makes $350 billion available to private lenders to lend to small businesses. The program was designed such that any business or nonprofit that meets Small Business Administration standards (i.e., under 500 employees) can contact any certified lender (banks, credit unions, CDFIs) and request a loan that equals 250% of their average monthly payroll costs over the last 12 months (maxing out at $10 million). Importantly, there are no fees, no credit score requirements, and no collateral required. The loans will be forgiven—effectively becoming grants—if the business uses the loan to cover payroll expenses by keeping their employees on payroll or rehiring employees before June 30. But the specifics of the loan forgiveness are not entirely clear, and new guidance by the Treasury Department suggests that the program is not as generous to small businesses as originally believed. Moreover, the requirements may be difficult for banks to implement, which leads to the major question with PPP: Will this relief get to businesses fast enough, and will it make sense for small businesses to take on these debt loads under uncertain current conditions? The application form is simple, but estimates for loan processing vary considerably. Treasury Secretary Steven Mnuchin has indicated that borrowers will receive funds the same day they apply, but other estimates suggest it could take weeks.

- SBA Economic Injury Disaster Loans and Grants: The SBA’s Economic Injury Disaster Loan (EIDL) program differs from PPP. In the wake of a disaster, SBA offers lower-interest loans of up to $2 million to help small businesses recover. Every state has qualified for this disaster relief, and thus many small businesses have already applied for these loans. While there is no set timeline, approval for these loans can take weeks. Eligibility requirements are more onerous than PPP, and the loans are issued by SBA, which means they’ll likely take longer to be issued. Therefore, through the CARES Act, Congress gave SBA $10 billion to issue as $10,000 grants to small businesses that apply for EIDL loans. These grants will be available within three days of filling out the loan application, and businesses do not have to pay them back. If they qualify for a PPP loan, the EIDL grant will be deducted from that loan amount.

- SBA debt relief: For the subset of small businesses that already have a loan from the SBA, Congress made $17 billion available to provide six months of principal and interest relief. This will be administered by the lender that issued the loan.

What should local leaders do now?

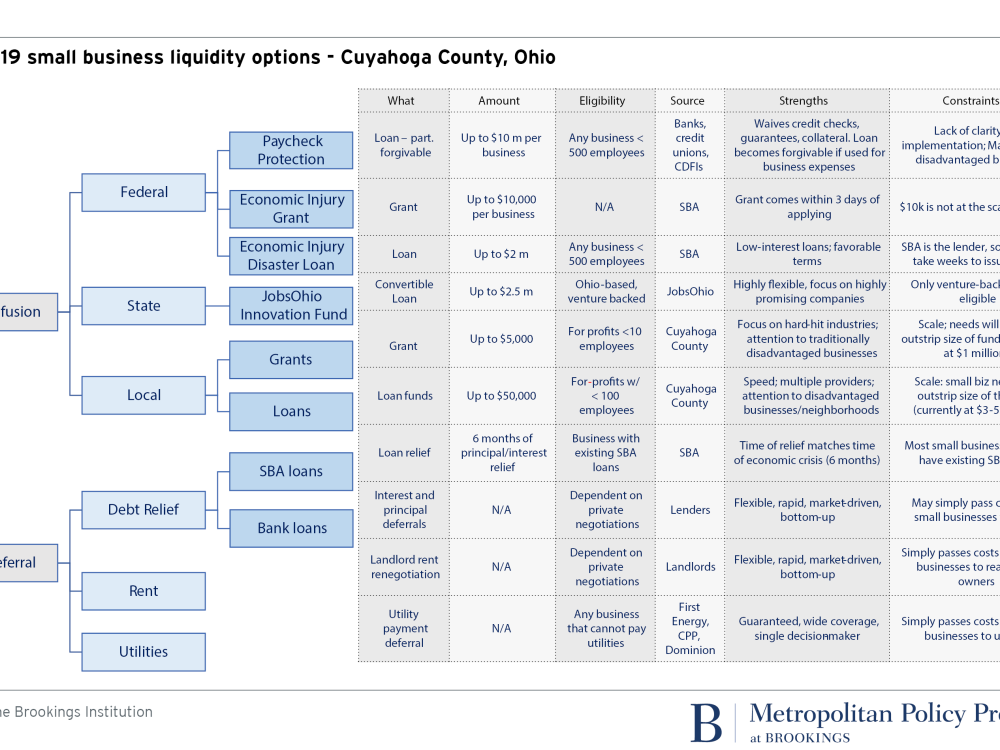

Map the options for small business liquidity

The equation for the small business crisis is troubling but simple: Small businesses are not generating revenue, yet they still have fixed costs (utilities, rent, debt payments, etc.) and variable costs such as payroll that policymakers want to incentivize them to maintain. Additional liquidity can come through two routes: 1) inject cash, or 2) reduce expenses. The purpose of mapping different small business liquidity options is to inform the small business support ecosystem’s strategic response and address gaps.

There is no silver bullet for the small business liquidity problem—it will require using every pathway imaginable. Figure 1 outlines these liquidity pathways for one local community: Cuyahoga County, Ohio. Economic development and community development officials consulted local financial institutions, real estate developers, CDFIs, and small business development intermediaries to outline these options in addition to reviewing the CARES Act. As you’ll see, some of these pathways are formal programs—both local and federal—while some represent private market renegotiations and deferrals, either on the part of landlords, private lenders, or utility companies. Dozens of communities have already created local small business stabilization funds. To the extent that those funds can continue to be recapitalized, they should be. But with corporate and philanthropic balance sheets already stretched thin—and local governments likely entering their own fiscal crisis—self-help will only take cities so far.

Connect to CARES

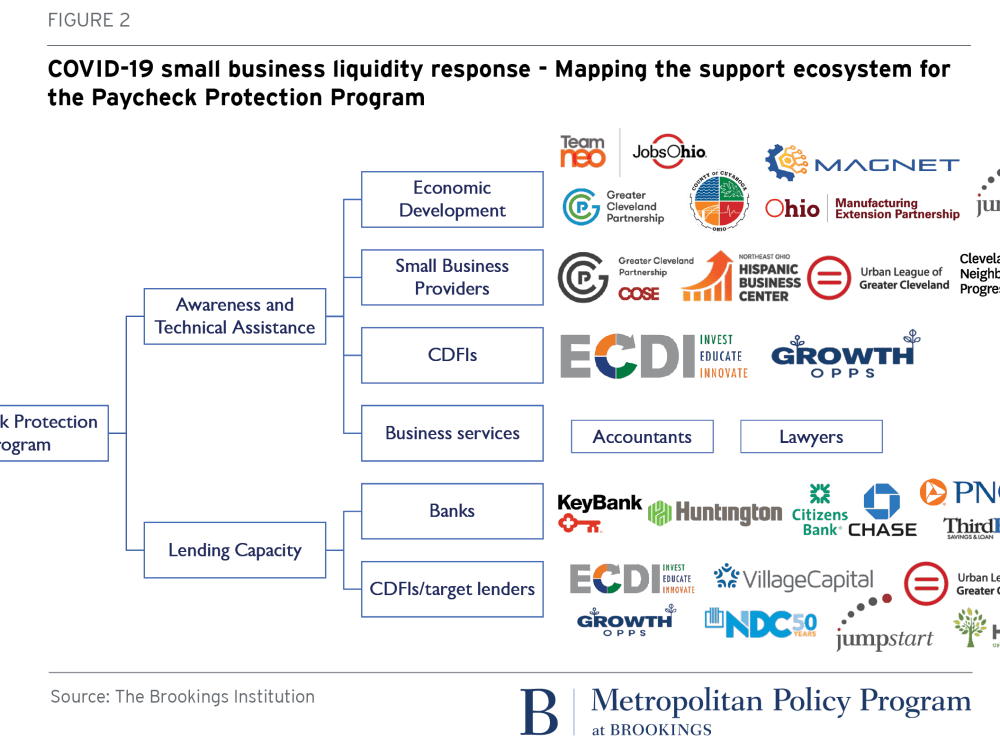

The programs embedded in the CARES Act—particularly the Paycheck Protection Program—are the nation’s best chance at staving off a small business disaster. At this point, building out strategies for connecting small businesses to these options is the most important job for small business support stakeholders in every community. Figure 2 maps this landscape for Cuyahoga County.

Small businesses vary in the degree they interact with mainstream institutions who are spreading awareness of these programs. For a business earning revenues of $25 million per year, they likely have a commercial banker, a lawyer, and an accountant that are all sending them information on these programs and guiding them through applications. A small restauranteur with annual revenues of $250,000, however, may not have a relationship with a financial institution nor local business support organizations like chambers of commerce or economic development organizations. As the Urban Institute’s Brett Theodos and Jorge González point out, many small businesses are not well-served by mainstream organizations, and thus additional outreach through community-based organizations, churches, and neighborhood groups is warranted. One way to ensure that every business in the local community receives information about what is available to them would be for the utility to send out a mailing on local and federal programs—in both English and Spanish.

Local communities will need to deploy technical assistance providers from Small Business Development Centers (which are receiving $265 million as part of CARES), chambers of commerce, CDFIs, and community-based business support organizations to help businesses become aware of and navigate these programs. The initial push from these small business assistance organizations will be to help businesses secure loans, but that support will be even more important when businesses try to seek loan forgiveness—a much more complex undertaking.

Advocate for CARES 2.0

The scale of the crisis will demand another economic relief package. In addition to fighting today’s battles, local leaders should inform their congressional leadership about how CARES is coming to ground, and advocate for additional investments in small business relief, worker support, and local and state government fiscal stabilization in the next package. Given early indications of the way the CARES Act is being implemented across the nation’s cities and regions, they will be needed.

Related Content

Authors