A growing share of students and parents are taking out increasingly large loans to earn higher education degrees that do not pay off the down the road. With student debt now reaching $1.4 trillion, many are rightly worried about what will happen if it cannot be repaid.

As borrowers continue to struggle with their student loan burdens, a key question is who should be held accountable when students cannot repay their loans? Clearly, the students themselves are already on the hook for their loans, which cannot be discharged even in bankruptcy. And if they are never able to repay, taxpayers are left holding the bag. However, the postsecondary institutions where these loans finance a large fraction of overall operations do not currently incur any costs when the loans systematically fail to be repaid. Schools should be held accountable when they systematically ask students to borrow for an education that proves to be a poor investment.

This is one question the Senate HELP committee is asking as Congress pursues the reauthorization of the Higher Education Act of 1965—the federal law responsible for federal financial aid programs. Reaching out to members of the higher education community, Committee Chairman Lamar Alexander (R-Tenn) requested feedback on how to create accountability measures that ensure students receive degrees worth their time and money.

We wrote to the committee to explain an idea of ours cited in a recent committee white paper: A risk-sharing proposal where institutions share in the risks that students and taxpayers face from burdensome loans. The idea was originally proposed in this 2017 Hamilton Project paper.

We believe educational institutions need stronger incentives to improve the long-term financial outcomes of their students, and that rigorous accountability is needed to promote quality educational outcomes, to ensure students do not take on unmanageable debt, and to safeguard the taxpayer investment of hundreds of billions of dollars in higher education.

Though our comment to the committee stressed the need for improvements in institutional accountability, we also cautioned against adopting weak versions of the risk sharing proposal or eliminating existing federal protections for student borrowers and taxpayers.

Our risk-sharing proposal would:

- Make higher education institutions partially repay the government when a cohort of borrowers fails to meet a repayment threshold within five years. If after five years of exiting an institution, student borrowers are not on track to repay their undergraduate loans within 15 years, our proposal requires institutions to chip in for a portion of the underpayment. The threshold was set so that a sizable number of institutions had “skin in the game” and a financial incentive in their students’ post-college success. Lower thresholds—like a risk-sharing target of zero percent repaid after five years—are insufficient and would not provide broad incentives to improve educational quality, provide real accountability at low-performing institutions, nor insulate taxpayers or borrowers from the consequences of unpayable debts.

- Examine both program-level and institution-level loan outcomes. Measuring loan outcomes at the program level is ideal, but risk-sharing incentives should include an institution-level backstop to prevent schools from gaming the rules or small programs from being excluded.

- Complement existing student protections. Risk-sharing should not be viewed as a substitute for existing student protections like Gainful Employment or 90/10 rules. This is particularly important as we develop more practical experience with risk-sharing policies.

- Revenues raised through risk sharing should be provided to institutions that serve low-income students well. The proposal should promote access to high-quality institutions for those who cannot afford to attend on their own.

Why we need more accountability

Despite the significant benefits of a college education, many students struggle with high costs of tuition, experience poor labor-market outcomes, and have difficulty repaying their student loans. 11.5 percent of borrowers entering repayment in FY 2014 had defaulted by the end of FY 2016. Over longer horizons, outcomes are even worse. A recent study by Judith Scott-Clayton shows that among borrowers entering school in the 1995-96 school year, 25 percent had defaulted at some point within the subsequent twenty years. The more recent 2004-05 cohort has substantially worse outcomes—with a quarter having defaulted at the 11-year mark. Such poor outcomes are concentrated among students at low-quality institutions, who are less likely to complete a degree and—even if they do graduate—are less likely to have earnings high enough to repay their loans.

Existing accountability systems have reduced the incidence of very poor student loan outcomes using rules based on student loan defaults (the Cohort Default Rate rules), how educational costs are financed (the 90/10 rules), and post-enrollment labor market outcomes (the Gainful Employment rules). However, the efficacy of the Cohort Default Rate rule, in particular, is waning because of changes in the educational market and rising enrollment among borrowers in income-driven repayment plans (IDR). While IDR helps protect borrowers from the worst consequences of default, it has the unintended consequence of undermining existing the current default-rate-based accountability systems. As more borrowers enroll in IDR plans, default rates will fall regardless of whether a school is offering economic opportunity to their students or whether those students ultimately will repay their loan obligations. Hence, default-based accountability systems will no longer be an appropriate tool for ensuring institutional quality or measuring student loan repayment.

Related Content

Better accountability systems are also more important today simply because of the increase in student debt due to both rising costs and increases in loan limits and credit availability among undergraduates, graduate, and parent borrowers. Borrowing is more widespread today than in the past, and the dollar amounts are far larger. There is currently $1.4 trillion of federal student debt outstanding, up from $0.5 trillion in 2007. In Fiscal Year 2009 (the year on which we focus for data analysis in our paper), approximately 3.8 million students entered repayment with $57.4 billion in aggregate initial loan balances, or an average of $15,100 per borrower. There has also been a proliferation of institutions and programs offering low-quality education subsidized by the federal government through the loan program. Hence, the risks to taxpayers and borrowers have increased substantially without commensurate protections or economic benefits. The misaligned incentives in educational markets are increasingly important.

College remains an excellent investment and—for many students—a student loan is an excellent way to finance that investment. However, the consequences of bad choices can be severe. Student loans cannot be discharged in bankruptcy, and defaulting on federal student loans may result in serious consequences for borrowers, including damaged credit, wage garnishment, and offsets of tax refunds and Social Security payments. Even for borrowers who do not default, outstanding loan balances may cause other financial hardships or make it difficult to reach important economic goals.

The current system is also unfair to taxpayers. Because a substantial fraction of loaned funds at low-repayment rate institutions will never return to federal coffers, the student loan program represents a substantial taxpayer-funded transfer to these institutions. Taxpayers should not have to support institutions that provide little or no educational value to their students. Responsible stewardship of federal dollars requires that subsidies be targeted to institutions that do well by their students.

Why risk-sharing?

In addition to managing taxpayer risk, accountability measures at the federal level should direct federal aid toward high-quality programs that lead not only to degrees, but to degrees that lead to jobs that allow students to repay loans and thrive economically. Institutions that receive federal aid and disburse loans to students on behalf of the government are in the best position to help their students succeed and share in the responsibility for their students’ outcomes. Hence, it is important that institutions have the right incentives to make improvements.

Risk-sharing programs that give schools “skin in the game” are one way to provide incentives to improve students’ loan outcomes. A well-designed proposal would improve matching between students and programs, enhance program quality, control costs, promote graduation, strengthen loan counseling, and keep institutions focused on student outcomes not just while in school but after leaving school as well. However, it is important to design the program to minimize unintended consequences. Potential unintended consequences include reduced access to education for low-income students, pass-through tuition increases, gaming of accountability metrics, and negative distributional consequences for institutions serving low-income and minority populations. Our proposal is designed to minimize such unintended effects.

We describe key elements of the proposal below; more detail can be found in our paper.

With student debt now reaching $1.4 trillion, many are rightly worried about what will happen if it cannot be repaid.

Focus on the repayment rate

Our risk-sharing proposal is based on a measure we call the cohort repayment rate—the fraction of a cohort’s initial principal that is repaid within five years after leaving school, calculated at the program level or institution level or both.1 In short, it asks whether students leaving a given program or institution have made sufficient progress repaying their loans after five years.

The repayment rate is a useful measure for federal accountability purposes because it directly reflects the federal investment and return on its investment, is straightforward to measure, draws on existing administrative systems, and it is difficult to game or manipulate. Moreover, it is highly correlated with student outcomes, other measures of institutional quality, and the economic return on federal loan dollars.

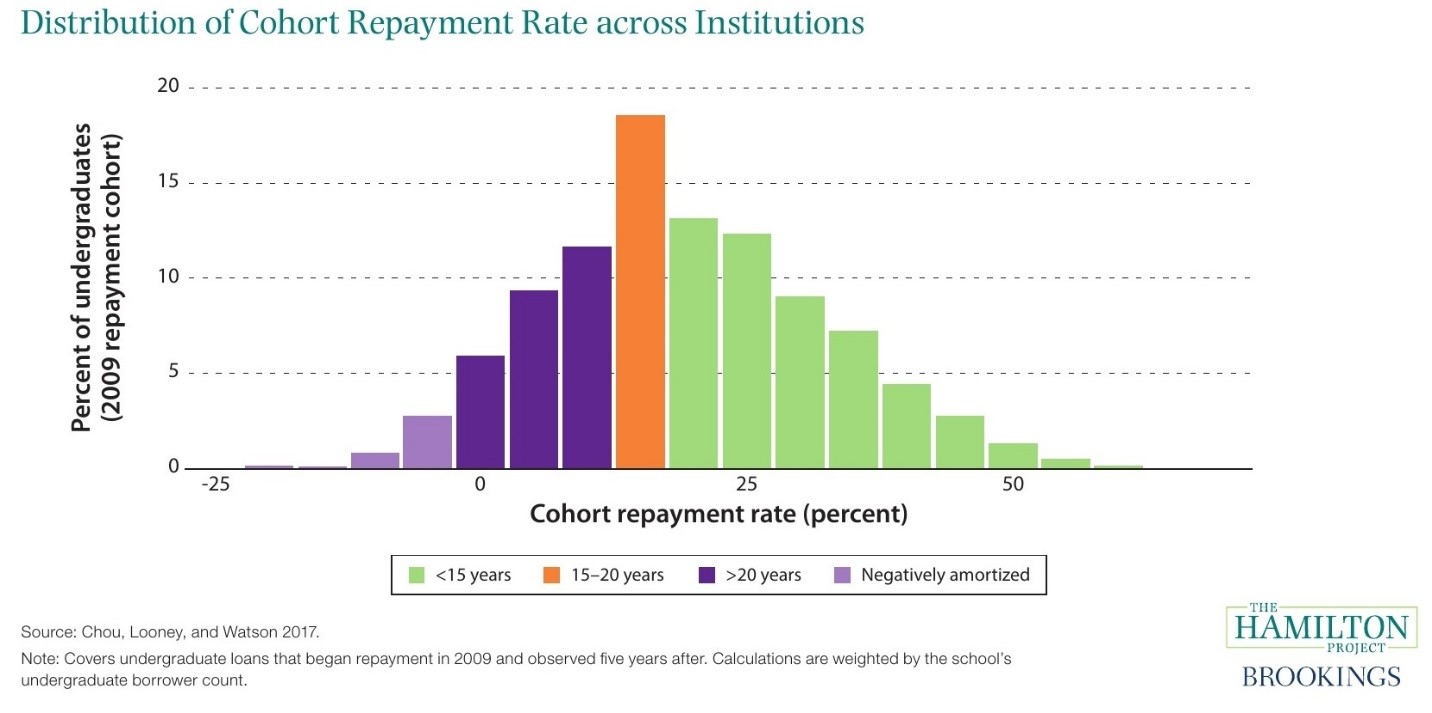

The cohort repayment rate varies considerably across institutions. The figure below shows the fraction of institutions classified by their undergraduate repayment rates. The figure shows that 32 percent of students attend institutions with cohort repayment rates below 15 percent (implying they are not on track to repay their loans within 20 years).

The measure can and should be measured separately for undergraduate and graduate loans, and can and should be measured by program as well as institution. A system that focused on programs only could lead to institutional gaming, but a well-designed system that combines both program and institutional-level measures would encourage institutions to focus their resources on the programs that are serving students most effectively. Data that is now routinely reported to the Department of Education makes such calculations feasible.

We propose that an institution’s aggregate 5-year cohort repayment rate—the share of the aggregate balances of its students that have been repaid 5 years after they were required to start repaying—be compared to a minimum threshold. To the extent that the actual balance repaid is too low, the institution would be required to repay the government for a share of the difference.

In our proposal, the threshold is that 20 percent of aggregate balances must have been repaid after 5 years to avoid any institutional obligation. About half of institutions in 2009 would have had a risk-sharing obligation under our policy. Though a student working to pay off a standard 10-year loan would be expected to pay down 40 percent of the principal after five years, few schools achieve a 40 percent repayment rate in practice. The 20 percent repayment threshold in our proposal is consistent with loans offered over roughly a 15-year repayment period.

The policy would require institutions reimburse the federal government for a portion of unpaid balances below the threshold, with the marginal rate per unpaid dollar starting at 25 percent. Institutions with unpaid balances below a lower threshold (15 percent) would reimburse the government for larger amounts. For schools below the threshold and liable for risk sharing payments, the payments would be around 3 to 9 percent of the original loan amounts distributed to schools. Funds generated from the risk-sharing program would be used to provide grant support to institutions with high value-added for low-income students (as measured by earnings compared to others of similar economic backgrounds), regardless of whether those institutions had high loan repayment rates.

A 20 percent rate is a reasonable target for institutions, especially if risk-sharing payments are initially modest but risk increases with the degree of underpayment. Such a threshold reflects a trade-off between incentivizing improved performance against possible unintended consequences of an aggressive target. An alternative target of 15 percent, roughly corresponding to a 20-year time frame, would also be reasonable to consider. On the other hand, some have advocated for risk-sharing systems that, like the current CDR framework, only target the institutions with the most extreme repayment problems. A threshold of 0 percent, for instance, would affect only about 5 percent of institutions and is unlikely to be sufficient to deter negative outcomes or provide stronger incentives for most institutions. We counsel against such a policy.

Importantly, no adjustment to the rate should be made for whether a student has defaulted, entered into a hardship forbearance, or made reduced or no payments because of income-driven repayment plans. As a result, the repayment rate is difficult to manipulate or game—students pay or they do not. It is also more difficult to manipulate than other measures of loan repayment, like the fraction of borrowers who have paid back at least $1 of principal or default rates.

Loans that fail to perform early on are very likely to remain non-performing at Year 15. Unlike the current default-centered loan repayment system, accountability systems that prioritize loan repayment directly reflect taxpayer risk. The repayment rate is directly relevant to federal finances—it represents the repayment on loans offered by taxpayers. As we show in our Hamilton Project paper and sister National Bureau of Economic Research paper, a student’s repayment after five years is a strong indicator of where the loan will stand after fifteen years. Early and late loan outcomes are highly correlated—nearly 90 percent of loans that are performing 5 years after entering repayment will still be performing at Year 15

The repayment rate is also reflective of student outcomes. Even after accounting for the economic background of the students, schools with low repayment rates have higher cohort default rates, higher levels of debt relative to earnings, and worse post-college economic outcomes. For instance, students from families earning below $30,000 have about a 58 percent chance of earning at least $25,000 if they attend a school with an average repayment rate, compared to only a 45 percent chance at lower-repayment rate institutions. These outcomes are similarly apparent in loan-performance. At the worst repayment-rate schools, low-income students are very likely to default and struggle to repay their loans on time.

Incentives, targets, and obligations

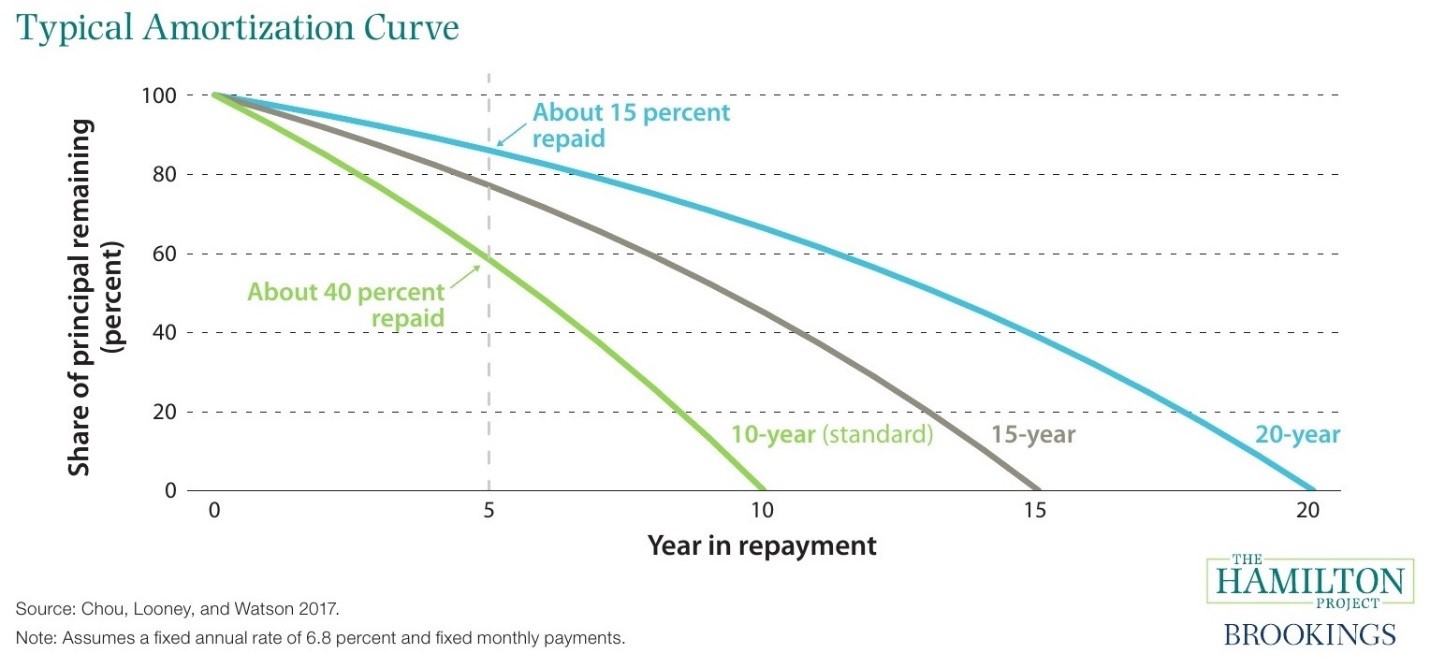

For the proposal to protect taxpayers and effect meaningful change, accountability should entail a broad-based, gradual incentive structure. Incentives should be relevant to more than just a handful of schools but should not be draconian for those with only modest repayment problems. The figure below gives a sense of how different repayment rate targets would correspond to repayment periods: our proposed 20 percent repayment rate target is associated with repayment over about 15 years, while a 15 percent target would require closer to 20 years.

Our program is designed so that risk-sharing obligations would be small or modest for most affected institutions, particularly those near the target level. However, the marginal impact of non-repayment is higher for schools with lower repayment rates. Specifically, there are three brackets: 0 percent, 25 percent, and 100 percent. Institutions with moderate repayment rates will experience a slight financial nudge to improve and a low effective rate measured as a fraction of overall loan dollars. Those with lower repayment rates will face more substantial fees. For institutions with very low repayment rates, risk-sharing obligations would be quite significant.

It may be desirable to provide a blanket exemption for some schools. In particular, institutions may decide to entirely opt out of the loan program if they face a large fixed cost due to risk-sharing or just do not want to deal with the uncertainty of having any risk-sharing payments (even if those payments are expected to be very small or they have very few borrowers). Causing such schools to exit the loan program could be an undesirable outcome.

In the proposal, we provide a nuisance exemption to schools where few students borrow. As modeled in the Hamilton Project paper, we exclude those at which less than a quarter of undergraduates borrow, as based on the College Scorecard. For schools where one-quarter to one-half of undergraduates borrow, we build in a linear dial-down of the assessment rate. This means a school with 30 percent of undergraduates borrowing would pay 1/5 of the undergraduate fee of a school with 50 percent of undergraduates borrowing even if they have the same loan performance and dollar volume. A dial-down rather than a binary cutoff avoids abrupt increases in the fee associated with making one additional loan. One could also exclude schools with very few total borrowers, and/or schools with a low dollar volume of loans.

Potential concerns

A concern raised by the proposal is that it could have the unintended consequence of reducing educational opportunities for disadvantaged students. Schools may be tempted to discourage enrollment from students who are poor ex ante credit risks. To be sure, one goal of the proposal is to reduce the likelihood that students attend programs that fail to provide them with educational value. But financial aid policies should not force low-income students to choose between not going to school or taking on debt they cannot repay.

In our proposal, we used the money raised to encourage access for low-income students. Because the proposal is expected to raise revenue, those funds could be used to finance bonus payments to institutions that serve low-income recipients well (as measured by students’ later-life earnings), in proportion to the number of low-income students served. However, raising revenue is not a primary goal of the proposal. If the program is successful, schools will improve repayment rates and face little or no risk-sharing obligation.

A related concern is that some institutions that serve disadvantaged students may not have sufficient resources to improve repayment outcomes. Though policymakers may want to consider a temporary exemption for Title III A and B and Title V schools before they are expected to come into compliance with the proposal, we do not include such an exemption here. The bonus payment system or a similar plan will help offset the cost of risk-sharing for many of these institutions, while at the same time preserving incentives for all institutions to improve loan repayment outcomes.

We expect that market pressures will prevent a full pass-through of cost of risk-sharing obligations to tuition, because the payments will apply only to a fraction of institutions competing in a common market. The bonus payment system will offset some or all of the resource constraints at under-resourced schools that serve low-income students well, and these schools will not need to increase tuition in response to risk-sharing.

Conclusion

A well-designed risk sharing program would improve accountability, strengthen educational quality, and improve loan outcomes. However, policymakers should be cautious. It remains to be seen to what extent a risk-sharing program will be effective or will have unintended consequences. Policymakers should not expect that risk-sharing can replace systems that have been effective for 25 years.

A well-designed risk sharing program would improve accountability, strengthen educational quality, and improve loan outcomes.

Further, it would be a mistake to adopt a risk-sharing scheme that incorporates some of the weaknesses of the current cohort default rate system. In particular, it is important that the accountability be broad-based. This means coupling aggressive targets with modest obligations for those who narrowly miss targets. A risk-sharing system that targeted, for example, a zero percent repayment rate would fail to provide meaningful incentives for improvement among a large number of institutions that could be serving students better.

A risk sharing system based on student loan performance is only one element of a well-designed accountability system and measures only one dimension of student outcomes. New administrative data used in the U.S. Department of Education College Scorecard and the Gainful Employment Rule provide information on wide variety of student outcomes including completion rates and labor market outcomes. These outcomes provide policymakers with multiple measures of quality that would be valuable inputs into a comprehensive accountability and program integrity system.

The right approach is to use a variety of incentives and multiple measures to monitor federal investments. In this regard, risk sharing systems are not substitutes for other effective taxpayer and borrower protections like the Gainful Employment and 90-10 rules. A well-designed risk sharing plan would be an important addition to efforts to protect students and improve accountability in higher education.

The authors did not receive financial support from any firm or person for this article or from any firm or person with a financial or political interest in this article. Neither is currently an officer, director, or board member of any organization with a financial or political interest in this article.

Authors

-

Footnotes

- Cohorts are defined using existing “cohort default rate” (CDR) rules. However, rather than focusing on the share of loans that subsequently default, we examine the cohort repayment rate: the amount of principal repaid by Year 5 of repayment, relative to the amount of principal owed at the start of repayment.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).