This blog post summarizes findings from a February 2018 paper by Adam Looney and Constantine Yannelis on borrowers leaving school with more than $50,000 in student debt. You can find more of Looney’s student lending research, alongside corresponding tabulations of administrative student loan data, on this data resource page.

Student loan debt—at almost $1.4 trillion in outstanding federal loans—has ballooned into the largest source of consumer debt after housing. An increase in student debt alone shouldn’t sound alarm bells, but debt that can’t be repaid should—and the evidence suggests that more borrowers with large balances won’t repay their debt anytime soon. This will create major hardships not just for borrowers who suffer serious financial penalties for failure to repay, but for the taxpayers left with the bill.

In a new Brookings paper that uses administrative data to look at “large-balance borrowers,” New York University’s Constantine Yannelis and I find that the share of students graduating with more than $50,000 in student debt has more than tripled since 2000, increasing from 5 percent of borrowers in 2000 to 17 percent of student borrowers in 2014. That group now holds the majority of outstanding student debt owed to the government—about $790 billion of the $1.4 trillion total at the end of 2017. Among these borrowers, we’re seeing a troubling trend: They’re repaying their loans more slowly, if at all.

In a country where education is still the doorway to opportunity, we should be wary of changes to our student lending system that prevent low-income students from obtaining the quality education their high-income peers can more easily afford. But neither should we force students to choose between not going to college or taking out loans that would be crippling to repay.

Strengthening institutional accountability systems and extending them to include graduate and parent loans is a sensible and proven way to improve student loan outcomes. Risk sharing proposals, like the one we proposed in our 2017 Hamilton Project paper, can be an effective and robust mechanism for reducing risks to taxpayers and borrowers and for promoting high-return educational investments.

Strengthening institutional accountability systems and extending them to include graduate and parent loans is a sensible and proven way to improve student loan outcomes.

In a risk-sharing student loan model— in which educational institutions would have to repay taxpayers for some of the loans their students don’t pay—institutions would have stronger incentives to improve the long-term financial outcomes of their students. The risk-sharing concept was recently referenced in a Senate HELP discussion paper (PDF) and in the President’s FY 2019 budget proposal (PDF, see page 41).

As a complement to accountability systems focused on academic success, financial oversight, and labor-market outcomes, a robust risk-sharing proposal would help improve outcomes for students and reduce costs for taxpayers.

Who’s taking on more student debt? Parents, independent undergraduates, and graduate students

While loan burdens over $50,000 were once relatively rare, the portion of borrowers with balances over $50,000 and even $100,000 has surged. In 1990, fewer than 5 percent of borrowers leaving school had loan balances above $25,000 (in inflation-adjusted terms) and almost no borrowers had loans above $100,000. By 2014, more than 40 percent of borrowers had balances above $25,000 and more than 5 percent of borrowers had balances above $100,000.

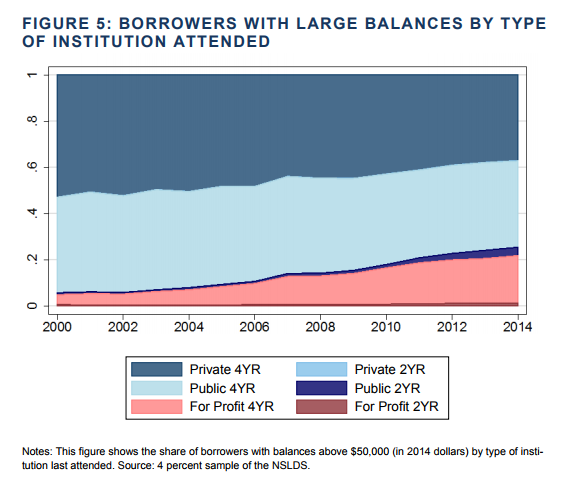

In the past, large-balance borrowers posed less of a risk to taxpayers and were unlikely to struggle with their loans because most went to graduate or professional schools, borrowed modest amounts and had strong labor market outcomes. They were doctors, lawyers, or MBAs from well-known public and private nonprofit institutions. But over the last 15 years, that’s changed. Today, large balance borrowers are increasingly likely to be parents and independent undergraduate borrowers—the government places lower limits on the loans that undergraduate borrowers who are dependents can take—whose economic outlook tends to be riskier and whose rising debts consume a larger share of their income. In addition, graduate-school borrowers are increasingly running up large loan balances at less-selective institutions, for non-professional degrees, and at for-profit or online-only institutions.

The share of borrowers taking more than $50,000 in graduate-only loans declined between 2000 and 2014 from 27 percent to 11 percent, while the share of borrowers taking out more than $50,000 in debt in undergraduate-only loans increased from 28 percent to 37 percent. For parents, that share increased from 6 percent to 16 percent.

Further, the share of large-balance borrowers who last attended less-selective schools has increased, and the share of graduate large-balance borrowers who attended a for-profit institution for graduate school increased from 5 percent in 2000 to 15 percent in 2014.

Large-balance borrowers aren’t necessarily defaulting—but they aren’t repaying, either

These borrowers aren’t defaulting at high rates, but that doesn’t mean they’re repaying their loans. As a group, large-balance borrowers have been slower to repay their loans, and repayment rates have been falling. At many institutions, even five years after leaving school more than half of students have failed to repay a dollar of graduate debt.

For cohorts who entered repayment in the 1990s and early 2000s, the median large-balance borrower made gradual progress repaying his or her loan. But for cohorts who entered repayment in the 2010s, a new pattern has emerged: the typical large-balance borrowers are falling behind on their loans with interest accumulating faster than they are making payments.

So why aren’t large-balance borrowers repaying their loans? Many more are taking advantage of provisions like hardship forbearances or enrolling in income-driven repayment plans, which suspend or reduce payments when borrowers’ earnings are low. The ability to make smaller payments based on one’s income and loan forbearance policies mean students can pay loans slowly and minimally for decades at a time.

But the rising take-up of such plans is driven by more concerning trends in the institutions where students are pursuing their degrees, how much they are borrowing, and how well they are doing in the labor market. A rising share of graduate borrowers are attending for-profit or less selective public and private non-profit institutions, where job prospects and student loan outcomes are worse, and they’re borrowing much larger amounts to do so. A rising share of large-balance borrowers are not employed, and their labor market outcomes measured in various ways have not increased between 2000 and 2014. Hence, with rising levels of debt, the ratio of their average debt to average earnings—one indicator of ability to pay—has increased.

It’s time to protect students—and taxpayers—from outrageous debt

It’s time to ask whether the government should be lending so much money to any student who wants it. Higher undergraduate and graduate loan limits implemented in the early 1990s and 2007, the elimination of limits on PLUS loans in 1993, watering down of accountability rules, like the change to the “85/15” rule in 1998, expansions of loan eligibility to online programs (including online graduate programs) in 2006, and overall rising costs have allowed many more borrowers to accumulate not-before-seen levels of debt, and many will never be able to repay it.

Looking at the evidence, it’s clear we’re overdue for stronger guardrails on how federal aid can be used, including restoring limits on credit, eliminating certain types of loans, strengthening institutional and program-level accountability rules in general, and applying those rules to institutions based on graduate and parent loan outcomes.

Because a small number of borrowers account for the majority of dollars in default, changes targeted at a small number of individuals and institutions could have large implications for taxpayers and the students involved, helping to keep borrowing to levels borrowers can realistically repay and to reduce costs of these programs for taxpayers.

Unless we adjust our policies, the student loan crisis will only get worse. Access to higher education is important, but driving students into crippling debt isn’t the best—or fairest—way to provide it.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

More students are taking on crippling debt they can’t repay—it’s time for higher education to share the risks

February 16, 2018