Over two years ago, Congress adopted Sections 1502 and 1504 of the Dodd-Frank Wall Street Financial Reform Act, which focuses on conflict minerals and natural resource transparency. However, the Securities and Exchange Commission (SEC) was tardy in issuing the implementing regulations, but it passed both rules this past Thursday— more than 450 days past its April 2011 deadline.

A lot is at stake for citizens in dozens of countries, for investors and for multinational companies. Section 1502 mandates that U.S. companies sourcing minerals from the Democratic Republic of Congo (DRC) and adjacent countries perform due diligence on the source and chain of custody of minerals and disclose whether they use conflict minerals.

Section 1504 requires publicly traded oil, gas and mining companies to make project-level disclosures of payments made to governments around the world for the purpose of commercial development of natural resources. The aim of both provisions is to enhance corporate and government accountability. Yet, vague rules that allow for exemptions or do not require reporting on critical details would easily undermine the objective of effective transparency.

Was the wait worth it? That, of course, depends on who you ask. The wait appears worth it in the case of rules on the disclosure of resource payments to foreign governments (Section 1504), while the results are somewhat mixed for rules mandating the disclosure of conflict minerals (Section 1502).

The SEC first voted on disclosure rules for conflict minerals (Section 1502). The mere fact that after such a long delay the agency finally voted in favor of these regulations constitutes a step forward. The intent of Section 1502 of Dodd-Frank (and thus of SEC) was not to mandate penalties for sourcing minerals from mines controlled by armed groups in conflict-afflicted regions. Instead it relies on the adverse reputational effect of such disclosure. Reputable companies would want to avoid having their name associated with armed conflict, human rights violations, slavery and rape. Yet, an important segment of the industry opposed such disclosures on the basis that compliance costs would be high and that disclosure would be ineffective in addressing instability in the region.

But following the SEC’s ruling on Section 1502, the glass is only half full because the industry managed to get some reprieve from full disclosure. For all companies there will be a two-year phase-in period, and for smaller companies a four-year phase-in period. Other companies, such as Wal-Mart and Target, will be exempted from disclosure because the SEC does not require disclosure for store brand products manufactured by third-party suppliers. Further, companies using recycled or scrap minerals would also avoid the disclosure rules.

Thus, while human rights advocates and the industry (with the exception of some firms which were not opposed to Section 1502) were generally at odds about the provision, they agreed that the outcome of the SEC ruling was mixed. Many in the industry are displeased that the rules were passed, but are pleased that there will be significant implementation delays and exemptions. Civil society and human right advocates are pleased that the SEC voted in favor of adopting rules but fear that the rules are relatively weak.

Both sides do agree that the disclosure alone will not solve the conflict in the eastern DRC; and human rights activists feel that the measures passed by the SEC may help mitigate conflict and deter human rights abuses, even though they believe broader governance reforms are needed. It remains to be seen how effective the actual implementation of these provisions will be and whether broader complementary measures to tackle misgovernance and conflict in the DRC will be implemented.

In contrast to the “glass half full” ruling on Section 1502, the Section 1504 ruling on natural resource payment disclosure represented a much fuller glass. The American Petroleum Institute (API), big oil and several other extractive industry companies had lobbied heavily against rules that would require project-level disclosure and in favor of various exemptions, including the so-called “tyrant veto”, which would exempt companies from disclosing payments in countries where payment disclosure was prohibited by local law.

In its ruling, the SEC rejected the “tyrant veto” exemption and exemptions in cases where contracts stipulate secrecy. Further, the SEC also mandated that companies file disclosures, rather than merely furnish them, which is important because the requirement to file enables investors to litigate in certain cases of false reporting. The SEC also specified that payments above $100,000 must be reported and disaggregated by category, rejecting the arguments put forth by the industry for a materiality approach or a threshold of $1 million.

A key question prior to the final ruling was how the SEC would define a “project”. Industry lobbyists pushed for a broad definition that would allow disclosures at as aggregate a level as possible. Some even tried to equate a project with all operations in a country. In its ruling, the SEC acknowledged that the term “project” is commonly understood by issuers and investors, and granted companies some latitude in defining what constitutes a project. But, thanks to the guidance issued by the SEC with the rules, the amount of discretion that companies will have is rather limited.

Specifically, in its guidance, the SEC rejected several project definitions that were proposed by industry stakeholders and strongly opposed by civil society. It clarified that a project cannot be defined at the country level or following criteria driven by geological basin, reporting unit or materiality thresholds. At the same time, the SEC indicated that for the purposes of the rule, the notion of “project” should be guided by the relevant contract (since the payments made by companies to the government are usually stipulated in the contract). Thus, the ruling demarcated reasonable boundaries around what constitutes a project. As a result, reporting is expected to take place at a rather detailed and disaggregated level.

Further, the SEC decision not to rule on a project definition may have been a clever move, both substantively and tactically. Substantively, giving companies latitude in defining a project rather than imposing a “one size fits all” definition may result in disclosure of payments for segments of the industry outside of exploration and production. Tactically, by sticking to the wording of the original Dodd-Frank law, the SEC may fend off a possible source of litigation by the industry (API).

However, the SEC’s clever ruling on the project definition may not dissuade the API from litigation. If they do decide to litigate, the industry body may opt to focus on the costs associated with implementing transparency rules, which they claim will be huge, particularly with regard to compliance costs and loss of competitiveness. In fact, in issuing the rules, the SEC itself did acknowledge that some of these costs to industry may not be trivial.

When discussing compliance costs, it is important to distinguish between the total costs of reporting and the additional costs resulting from the new disclosure requirements. The latter are particularly relevant in assessing the potential costs of 1504, and are likely to be much lower than some companies claim. Most companies already have extensive internal systems in place for recording payments, and already collect project level information to handle their current reporting requirements. Adjustments due to the new set of rules are thus likely to be relatively minor and could be done in a timely and cost-effective manner.

Several companies also highlighted concerns that other market participants could use information disclosed by issuers to derive trade secrets such as contract terms, data on reserves, or other confidential information. These arguments have been rebutted by outside analysis and advocates of transparency. The SEC did not give them credence either, noting that the statute covers the amount of payments, not the manner in which payments are determined or other contract terms.

Companies were also concerned that they would become less competitive relative to companies not subject to the reporting obligations under 1504. The American Petroleum Institute (API) and companies like ExxonMobil and Rio Tinto are concerned that by becoming more transparent they will lose contracts in countries where the government either legally prohibits disclosure or prefers to work with companies that are not subject to payment disclosure. In its ruling, the SEC rejected this flawed notion that implies that corrupt or opaque governments would drive the provision of exemptions from transparency of companies listed in the U.S.

Furthermore, the impact on competitiveness would be minimal in the numerous jurisdictions where payment information is already publicly available, partly as a result of increased participation by governments and companies in the voluntary disclosure framework under the Extractive Industry Transparency Initiative (EITI).

There is also a clear trend toward the globalization of mandatory disclosure of payments by extractive sector companies. The European Union is soon likely to adopt laws similar to those set forth by the U.S. Together, U.S. and EU regulations would cover the vast majority of listed natural resource companies in the world. Moreover, mandatory rules were already adopted by the Hong Kong Stock Exchange and discussions are ongoing in other financial centers in Asia.

More generally, it seems misplaced to equate, as API and some companies have tried to, competitiveness and the ability to keep payments secret. Yes, there are some companies in the world that benefit from rent-seeking, monopolistic behavior, bribery of foreign officials and tax avoidance or outright evasion.

But, as previously argued, private companies around the world, including in dynamic sectors in the U.S., compete on the basis of efficiency, entrepreneurship, and high technical and innovation standards. A truly competitive firm would have little to gain from secrecy; to the contrary, it would benefit from the level playing field created by high levels of transparency.

Over the past two years, the discussion of the potential costs of disclosure has been long and detailed. By contrast, there has been far less said about potential benefits. It is the case that the benefits of transparency are not easy to quantify. Yet, as we have noted before, a body of empirical work has found the benefits of transparency, good governance and corruption control to be quite large and to accrue to multiple stakeholders, including citizens, investors and competitive companies in the extractive sector. In their submissions to the SEC, some investors noted that new disclosure requirements would help them assess the risks faced by companies operating in resource-rich countries and thus possibly promote investment and capital formation.

In fact, our own data and research suggests that in the long run there is up to a 300 percent development to citizens dividend from increased transparency, accountability and improved governance. In particular, improved governance can contribute to a threefold rise in incomes and two-thirds decline in infant mortality.

Further, project-level disclosure will empower citizens to obtain information on how much their governments earn from natural resources, advocate for a fairer share of revenues, and verify government-published budget data. Once the data is disclosed and processed by analysts and civil society, citizens should also be able monitor the flow of money from the central government to regional and local governments, thus helping ensure that they are receiving what is promised. Finally, more transparency in dealings between companies and governments may help companies sidestep attempts by some government officials to engage in unethical activities.

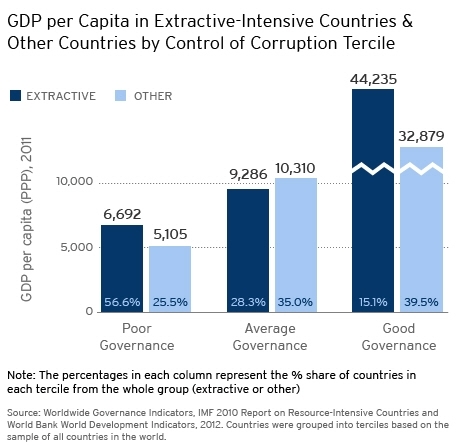

More generally, it is also important to emphasize that extractive-intensive countries need not be subject to the resource curse. Countries with transparent and enlightened leadership, and with satisfactory standards of governance and corruption control (supported by good corporate governance practices among multinationals), can harness their natural resources to achieve robust and inclusive growth and development. As seen in figure 1, extractive-rich countries that do well in controlling corruption also have higher income levels, in contrast with poorly governed ones. The challenge in coming years is raising the governance standards of many resource-rich countries that are lagging in this area.

The robust implementation of the SEC rules on transparency in natural resources as mandated by Section 1504 of the Dodd-Frank Act will be an important step forward, but it will not be sufficient. In order to make extractive industry transparency a global norm, the EU and other financial centers need to follow the lead taken by the United States. Building on its success in promoting the U.S. rules on Section 1504 advocacy organizations, such as the Publish What You Pay Coalition and its main NGO members, as well as key investors, need to now fully focus on the passage of a similarly strong set of transparency rules in the European Union.

Engaging China on this issue will also be important. And extractive-rich countries around the world need to do their part, deepening their work on transparency through the EITI and other such mechanisms. And important dimensions of opacity that still prevail in natural resources, untouched by Dodd-Frank 1504, will need to be addressed separately, such as promoting contract transparency; tackling the challenge of obscure “beneficial ownership” (to ensure the public is aware of who the ultimate owners/beneficiaries are of natural resource extraction and exploration); and the further analysis and codification of the considerable payoff to transparency reforms.

The original Dodd-Frank Section 1504 and the SEC rulings are a huge step forward toward transparency and are likely to resonate worldwide. But much of the concrete work remains ahead.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Op-edSEC Passes Natural Resource Transparency and Conflict Minerals Rules: The Glass is Fuller than Expected

August 28, 2012