The problem

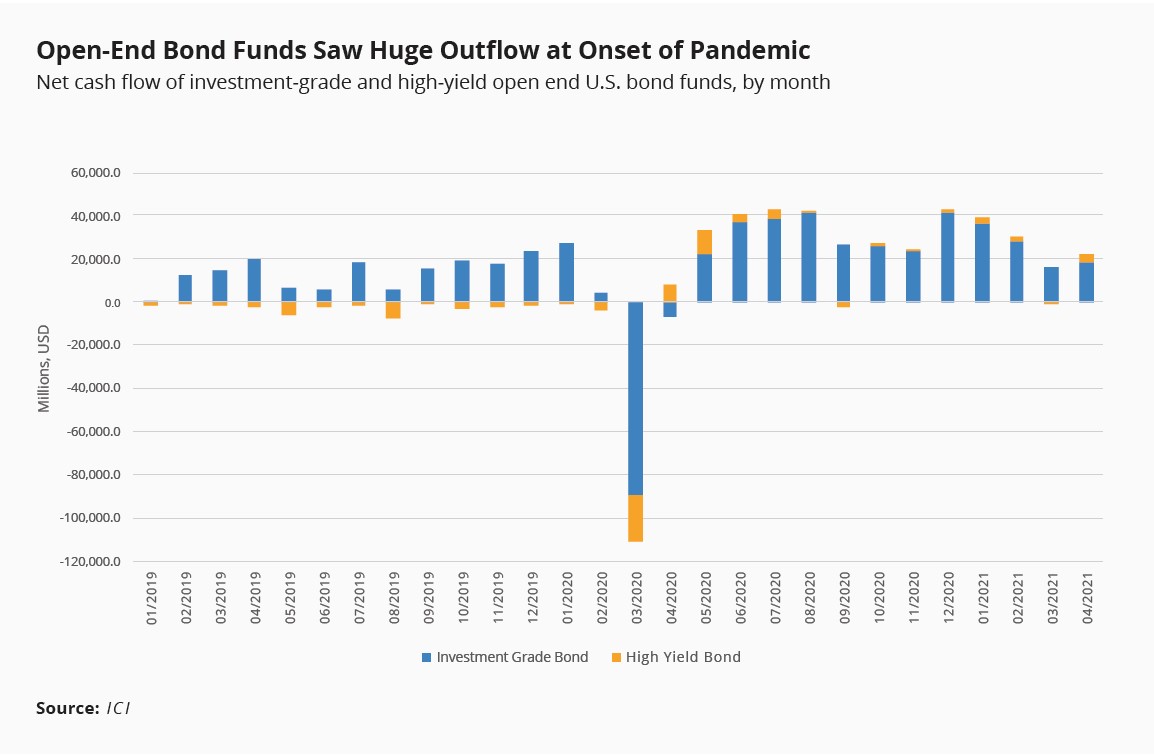

In March 2020, at the start of the COVID-19 pandemic in the U.S., investors pulled more than $100 billion out of corporate investment-grade and high-yield bond mutual funds, forcing funds to sell some of their holdings. The spread between corporate bond yields and U.S. Treasuries (a market that had its own dysfunction) widened, transaction costs rose, and issuance of new bonds came to a halt, disrupting the flow of credit to the nation’s corporations. This led the Federal Reserve to intervene by offering, for the first time, to buy corporate bonds and exchange traded corporate bond funds in what proved a successful effort to keep credit to corporations flowing. It was an extraordinary move that underscores the risks these funds pose to financial stability. (For details, see this Federal Reserve note.)

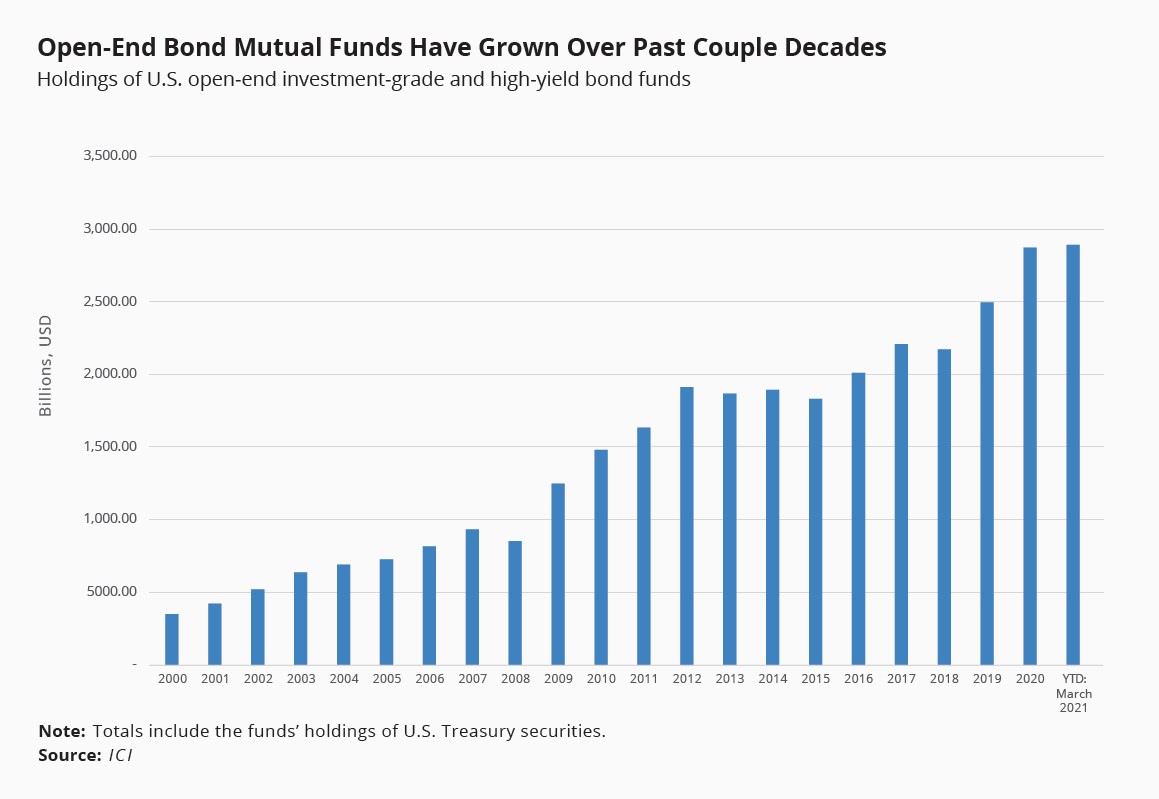

The growth of open-end fixed income funds magnifies the systemic significance of the tension between shareholders’ expectations of daily liquidity and the (often illiquid) holdings of the funds. The average corporate bond is traded about once a month. Shareholders in an open-end bond fund expect (and receive in many cases) to be able to sell their shares much more easily and quickly than if they held bonds directly. When he was governor of the Bank of England, Mark Carney said, “These funds are built on a lie, which is that you can have daily liquidity, and that for assets that fundamentally aren’t liquid.”

In normal times, redemptions are modest and can be met by an offsetting inflow of funds or by selling liquid securities in the portfolio like Treasuries.[1] But big outflows can force a fund to sell holdings of less liquid securities that may require a price concession to attract a buyer. Especially in times of stress, big sales force down bond prices because of the absence of a truly liquid market for the underlying bonds. This, in turn, raises the rates that all corporate borrowers have to pay on newly issued bonds—if they can sell them at all—thus harming the overall economy.

Shareholders in a fund who get out early can redeem at a better price than those who remain, because their redemptions are met before the fire sale forces the fund to mark down the value of its portfolio. This creates a “first-mover advantage,” which can induce a rush to the door that amplifies the price movements that would otherwise occur. (With equity funds, this is less of an issue. Most equities are traded in highly liquid markets where prices quickly reflect order flow. To be sure, there are small stocks that do not trade every day, but most trade every few days, and there is not enough volume in any single small stock to create a problem. The average corporate bond trades once a month; some commercial paper hardly ever trades. So any selling of such fixed-income securities can affect the price substantially.)

A possible solution

More widespread adoption of swing pricing. Swing pricing is widely used in Europe but not in the U.S., although its use was authorized by the SEC in 2018. Basically, it allows the manager of an open-end fund to adjust its net asset value up or down when inflows or outflows of securities exceed some threshold. In this way, a fund can pass along to first movers the cost associated with their trading activity, better protect existing shareholders from dilution, and reduce the threats to financial stability.

This brief draws from the report of the Task Force on Financial Stability, which recommended more widespread use of swing pricing, and a roundtable the Task Force convened with industry, academic, and public sector officials to consider the pros, cons, challenges and costs to doing so.

What is an NAV, and why is that important for open-end funds?

The net asset value (NAV) is the price at which shareholders can purchase or sell their shares in an open-end mutual fund. The Investment Company Act of 1940 requires mutual funds to offer and redeem shares at the next net asset value calculated by the fund after receipt of an order. The NAV is usually calculated by dividing the value of the fund’s assets by the number of its shares. With swing pricing, this calculation of the NAV is adjusted up or down to account for the price impact and transactions costs that will be incurred because of redemptions and new share purchases that will occur after the NAV is calculated. Most U.S. funds calculate their daily NAV using the closing market price of the securities at 4:00 pm Eastern time. Orders from investors that are submitted after 4:00 pm are executed at the next day’s NAV.

Open-end funds can issue an unlimited number of shares. In contrast, a closed-end fund has a set number of shares, the price of which is determined in the market and can diverge from the net asset value of the underlying assets. Exchange-traded funds (ETFs) combine characteristics of open-end and closed-end funds. The price of ETFs fluctuates throughout the day and is determined by the price in the market. The movement in ETF prices is indicative of the kind of swing in an NAV that might be needed in stress, because the ETF price adjusts to attract a willing buyer.

What is dilution and the first-mover advantage in open-end funds?

If shareholders redeem a large quantity of shares in an open-end mutual fund, the fund may be forced to sell not only the highly liquid U.S. Treasuries it holds, but other assets as well. If many funds are doing the same thing at the same time—as they were in March 2020—the price of their underlying assets can fall; this is known as a “fire sale.” The first redeemer or first mover gets out at the initial NAV, which does not reflect the price declines associated with the subsequent fire sale, leaving the remaining investors to bear the costs associated with the portfolio manager having to sell assets to satisfy the first movers. This decline in the value of the fund’s holdings, which are owned by the remaining investors, is known as “dilution.” In a stress situation, therefore, investors have strong incentives to be among the “first movers,” which itself can amplify redemptions and resulting fire sales.

Using data on daily fund flows, Falato, Goldstein, and Hortacsu find that between February and March 2020, the average bond fund experienced outflows of about 10% of net asset value, far larger than the 2.2% experienced during the peak of the 2013 taper tantrum. They find that fund illiquidity and vulnerability to fire-sale spillovers were the primary drivers of these outflows, and that the “more fragile funds benefitted relatively more from the announcement effect of the Fed facilities.”

How does swing pricing address this issue?

Swing pricing is a mechanism to apportion the costs of redemption and purchase requests on the shareholders whose orders caused the trades. It is designed so that remaining shareholders don’t bear all the costs (including dilution) caused by first movers. In effect, those attempting to take advantage of limited fund liquidity are charged for their redemptions by adjusting the price they receive to reflect the liquidity of the market for the fund’s assets. With swing pricing, the incentive to be a first mover is diminished, and with it the risk that existing shareholders will be diluted and the risk that large redemptions will drive prices down sharply with spillover effects on the market and the economy. To be fair both to those who sell and those who remain, a swing price must reflect a fair valuation and approximate the costs imposed by first movers; it cannot be set simply to impose an enormous penalty on redeeming shareholders.

Under full swing pricing, the NAV is adjusted daily for the likely costs of redemptions, regardless of the amount of shareholder activity. Under partial swing pricing, the adjustment is triggered only when net redemptions exceed some pre-determined threshold—a recognition that small transactions do not pose much of a problem.

How does swing pricing work in Europe?

Many global open-end mutual funds are based in Luxembourg (because it has a favorable regulatory climate), and many of those routinely use swing pricing.

Not all funds follow the same procedures, but here’s an illustrative example. All orders that will be redeemed at a given day’s NAV must be received by noon CET on the day of the trade. In that case, any orders received after noon will be processed at the next day’s NAV. The NAV itself is not set until 4 pm CET each day. This gives the fund four hours to assess its order imbalance and determine the gap between buy and sell orders. Most buy and sell orders can be “crossed,” so that rather than buying and selling new securities, the redeeming and purchasing customers can have ownership transferred without incurring any transactions costs or putting pressure on prices. If there is a net imbalance (say, many more requests to redeem than to purchase), then to meet the net demands, some securities will need to be sold. If there is a large imbalance, then the NAV is adjusted (or “swung”) to reflect the impact of the sales.

The swing threshold is the amount of net subscriptions or redemptions that trigger the adjustment to the NAV. The fund then estimates how much prices for the assets being sold are likely to move to meet the subscription or redemption requests it has received; other factors taken into account include transaction costs and the bid-ask spread. The fund then uses those estimates to adjust the NAV by some percentage, generally no more than 2% or 3%. The adjustment is known as the swing factor.

Swing thresholds and swing factors vary depending on the market for the fund’s underlying securities. Swing factors tend to be larger in funds that invest in more thinly traded securities.

Fund managers set the rules and size of the adjustment and disclose their procedures, but precise details are not always disclosed so as to avoid investors exploiting them unfairly. A bond fund prospectus might, for instance, set a maximum swing factor of 3%, but give the fund discretion up to that level.[2] (For an example, see paragraph 17.3 of the prospectus for BlackRock’s Luxembourg-based global funds. )

Here is a stylized example of partial swing pricing from Allianz. It shows the threshold (the volume of orders) that trigger swing pricing in normal markets and in times of distressed markets, and the size of the swing under various scenarios (0.5% or 1.0%).

A survey by the Bank of England and the Financial Conduct Authority of 272 U.K. mutual funds found that 83% (202 funds) have the option to use swing pricing in place. Most funds using partial swing pricing had a trigger of net flows of 2% or less of total NAV. During COVID, however, several funds used their discretion and reduced their swing threshold or moved to full swing pricing. Swing pricing is advantageous to investors not only because it mutes dilution, but because the fund needs to hold fewer lower-yielding highly liquid assets to meet redemptions.

Researchers at the Bank for International Settlements compared the track record of Luxembourg-based funds (which generally use swing pricing) to similar U.S.-based funds (which do not use swing pricing). They found that the Luxembourg-based funds hold less cash than their U.S. counterparts. They also found that during the 2013 taper tantrum, the Luxembourg funds had higher returns than their U.S. counterparts (in part because there was less dilution and in part because they hold less cash), though there was more daily volatility in the Luxembourg funds.

In addition to the Luxembourg-based funds, funds based in the U.K., Ireland, France, Netherlands, and recently Germany use swing pricing.

While investor fairness has been the primary driver of swing pricing in Europe, market participants say it can affect investor behavior in ways that may contribute to financial stability. If an investor has a very large order to place in a European-based fund, the investor may spread out the purchase or sale over several days or otherwise break up the order to avoid imposing costs on the mutual fund that will be passed along in an adjusted swing price.

What are the impediments to implementing swing pricing in the U.S.?

The institutional structure of the market and operational issues are the main impediments to embracing swing pricing in the U.S.

Although the NAV is usually set at 4:00 pm Eastern time every trading day, many U.S. funds don’t know the size of their net inflows and outflows until late in the day or even the next morning. Many funds receive order flows from intermediaries that stand between an investor and the fund, such as 401k plan administrators, broker-dealers, and financial advisers. Some intermediaries have agreements that allow them to receive requests until 4:00 pm Eastern but not convey the order to the fund until that evening or even the next morning, but then upon passing them on still have the order serviced at that 4:00 pm NAV. In other words, the fund managers determine the NAV before they know how large the flow of orders is. Such agreements would need to be renegotiated and the software systems used by the intermediaries would need to be overhauled if new redemption rules were to be put in place. The intermediaries would also need to rework their client agreements.

Industry participants noted the following additional considerations:

- Setting a cutoff at 12:00 noon New York time for investors to place mutual fund orders at today’s NAV would be 9:00 am in California and 6:00 am in Hawaii. But global funds based in Luxembourg deal with even more time zones and have navigated this problem.

- Retirement fund record keepers and insurance companies require actual NAVs to process trades, e.g. an investor who wants to sell $1 million worth of shares need to know an NAV to translate the $1 million into an actual number of shares. European funds often price such trades at yesterday’s NAV.

- Smaller fund management companies may not have the resources to implement swing prices.

In any event, changing all this would be costly and would require a mandate from the Securities and Exchange Commission and coordination with other regulators, including the Department of Labor (which has oversight over retirement plans) and FINRA, among others. No single fund or group of funds will make this shift unless everyone else is doing so as well.

If a shift were mandated, the same rules would need to be applied to other types of savings vehicles that are economically similar to mutual funds, such as bank collective investment trusts.

When it authorized swing pricing in the U.S. in 2018, the SEC said, “We…appreciate the extent of operational changes that will be necessary for many funds to conduct swing pricing and that these changes may still be costly to implement, but we were not persuaded by commenters who argued that these changes are insurmountable, and indeed one stated that despite these challenges ‘the long-term benefits of enabling swing pricing for U.S. open-end mutual funds outweigh the one-time costs related to implementation for industry participants.’”

What are the alternatives to full-scale swing pricing?

One alternative would be for funds to consult and gather information from intermediaries and vendors a few hours before 4:00 pm, and then allow (or mandate) the fund managers to estimate a full-day’s flows and apply a swing factor if indicated. This would accomplish some, perhaps even much, of the benefits of swing pricing without the cost of reorganizing the whole network of vendors, intermediaries, and fund managers. It probably would require a safe harbor to protect intermediaries, vendors, and funds from liability if the estimates proved inaccurate.

The SEC anticipated such a possibility in its 2018 rule: “We acknowledge that full information about shareholder flows is not likely to be available to funds by the time such funds need to make the decision as to whether the swing threshold has been crossed, but we do not believe that complete information is necessary to make a reasonable high confidence estimate. Instead, a fund may determine its shareholder flows have crossed the swing threshold based on receipt of sufficient information about the fund shareholders’ daily purchase and redemption transaction activity to allow the fund to reasonably estimate, with high confidence, whether it has crossed the swing threshold.”

Other ways that have been discussed to mitigate the impact of transaction costs to a mutual fund’s portfolio generated by subscriptions and redemptions, as well as to reduce the risks to financial stability, are:

- An anti-dilution levy or redemption fee—a surcharge on investors subscribing or redeeming shares to offset the effect of those orders.

- Dual pricing, i.e. one price for buying shares and another for redeeming.

- Notice periods of perhaps a few days before an order can be executed.

- Redemption in kind, e.g. giving the shareholder bonds, not cash (not practical for funds with retail investors).

- Restricted redemption rights so investors can redeem up to a certain dollar amount on any one day.

- Redemption gates that allow a fund to limit withdrawals (although the experience with these for money market funds indicates that such gates tend to exacerbate the rush for the exits).

- A regulatory mandate to align redemption policies (including a requirement of advance notice) with the liquidity of the underlying securities.

Does the rising popularity of Exchange Traded Funds change any of these considerations?

ETFs require that buyers and sellers agree on a price that reflects market conditions. So during periods of stress, ETF prices move considerably. In a sense, they have an element of swing pricing built into them. Some investors may prefer ETFs because they know that it will be possible to sell on short notice.

ETFs have their own issues regarding the infrastructure that is needed to support them. To make sure the fund price reflects the value of the securities that the fund is supposed to track, ETFs rely on firms that serve as “authorized participants” (APs) to step in to buy or sell the fund to keep the price of the ETF close to the underlying securities. The APs make profits by arbitraging differences in the prices in the underlying securities and the ETFs. If the APs step back from trading, say, because they are exposed to more risk than they are comfortable with, the ETF prices can become disconnected from the prices of the securities that they are supposed to mimic.

This risk can mean that the ETF prices can also fail to reflect only fundamental risks associated with the securities. Nonetheless, ETFs are not subject to the first mover advantage and seemed to handle March 2020 better than the open-end funds.

Can swing pricing help improve the stability of money market mutual funds?

Money market funds are a special kind of open-end fund that can hold only short-dated securities such as U.S. Treasury bills, commercial paper, and certificates of deposit. By limiting the securities to those deemed relatively safe and liquid, it is expected that the price of the fund will be stable as the securities have no price risk if held to maturity. Problems can—and do—still arise for money market funds if they sell the securities they hold before maturity; in that case, there is price risk. Prime money market mutual funds invest in short-term private-sector securities such as commercial paper and certificates of deposit. Default rates on these securities are low, but they trade infrequently so they are subject to the same kind of illiquidity problems as open-end bond and loan funds.

Prime money market mutual funds suffered a run in March 2020, leading commercial paper markets to freeze up and prompting the Federal Reserve to intervene to keep credit flowing to businesses.

Investors in prime money market funds generally are using these funds as substitutes for bank accounts. They expect to withdraw, possibly large amounts in some circumstances, and at multiple times during the day. As a result, these funds often set an NAV multiple times throughout the day. Some in the industry say that feature of these funds means the information demands of setting a swing would be daunting and incompatible with how investors use them. Still, in a June 2021 consultation report, the Financial Stability Board included swing pricing among several possible policy responses to the problems posed by money market mutual funds.

[1] Heavy selling of Treasuries during the opening months of the COVID-19 pandemic created problems in that market as well. See Chapter 3 of the report of the Task Force on Financial Stability and the Group of Thirty report, “U.S. Treasury Markets: Steps Toward Increased Liquidity.”

[2] When the SEC authorized swing pricing in the U.S. in 2018, it set a 2% ceiling on the swing factor.

Anil Kashyap is a member of the Financial Policy Committee of the Bank of England and a consultant to the Federal Reserve Bank of Chicago and the European Central Bank. He did not receive financial support

from any firm or person with a relevant financial or political interest in this piece.

Related Content

2021

Authors

Commentary

What is swing pricing?

August 3, 2021