Though the emergency relief measures passed in response to the COVID-19 pandemic allowed student loan borrowers to defer their loan payments, student loan debt burdens still loom large for millions of U.S. households. According to the Federal Reserve, the national student debt level in the fourth quarter of 2020 was $1.7 trillion spread across 45 million borrowers—the highest level on record. Given the size of the debt burden, it is perhaps unsurprising that the possibility of student loan forgiveness has become a major policy discussion.

Most recently, President Joe Biden called for $10,000 in student debt forgiveness, while others, such as Senator Elizabeth Warren, have called for as much as $50,000 in debt forgiveness. Some have even called for total debt forgiveness, which would represent a larger amount of spending than the cumulative spending on unemployment insurance over the last 20 years. In a recent poll from the Center for Responsible Lending, 63 percent of respondents supported permanently reducing student loan debt by $20,000. As policymakers grapple with this question, it is important to explore how debt forgiveness might relate to household behaviors.

A student loan forgiveness experiment

To examine the relationship between student debt forgiveness and household behaviors, researchers at the Social Policy Institute conducted a survey experiment that asked participants with student debt to imagine a scenario in which the federal government forgave some amount of their student debt, and then had these participants report on how this would affect their decisions and behaviors. Participants were randomly assigned to one of four conditions that featured different levels of student debt forgiveness:

- Condition 1: $5,000 of student debt forgiveness

- Condition 2: $10,000 of student debt forgiveness

- Condition 3: $20,000 of student debt forgiveness

- Condition 4: All student debt forgiven

Participants could then select different behaviors they would engage in if their student debt were forgiven. The response options were intended to capture a wide range of experiences like working less, changing purchasing behaviors, having children or getting married, saving for different purposes, or returning to school. In total, 1,009 respondents who reported having student debt participated in the experiment.

The amount of debt forgiven matters

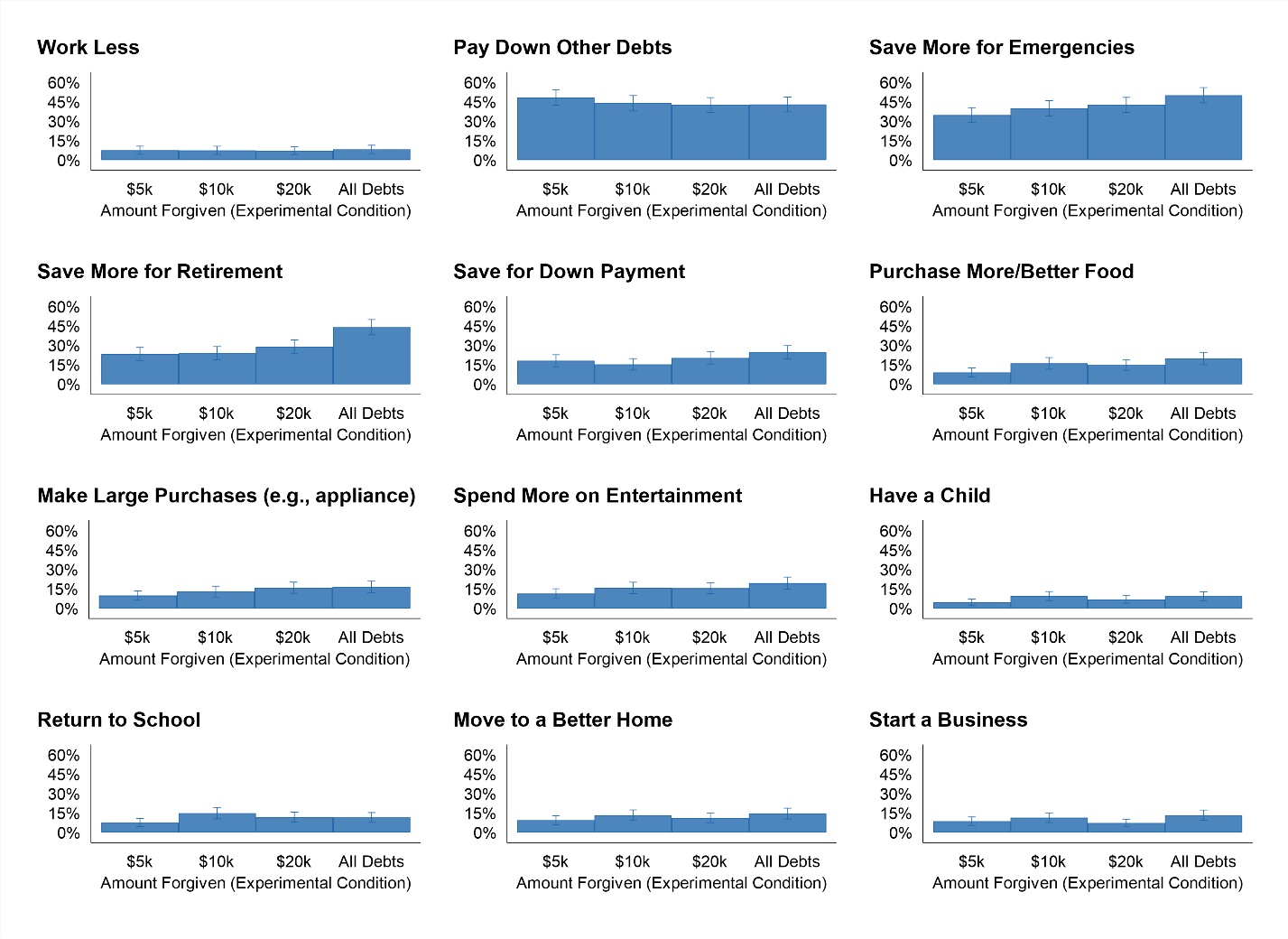

We present the results from this experiment in Figure 1. Generally speaking, the most common ways people reported that they would change their behaviors after student debt forgiveness—regardless of the amount forgiven—concerned their balance sheets. Large proportions of student debt holders reported that they would pay down other debts, save more for emergencies, save for a down payment on a home, or save more for retirement.

Figure 1. The relationship between the amount of student debt forgiven and household behaviors

Source: Social Policy Institute

Note: These results are from a survey experiment in which student debt holders were randomly assigned to receive one of four levels of student debt forgiveness. The impacts of the different levels of debt forgiveness were estimated using logistic regression models that also controlled for the amount of student debt held by participants. N=1,009. The brackets on each bar represent the 95 percent confidence interval of each estimate.

Turning to the differences between experimental conditions, we see interesting patterns in the relationship between the amount of debt forgiven and household behaviors. In particular:

- The amount of student debt forgiven was not strongly associated with either working less or paying down other debts.

- Higher levels of student debt forgiveness were associated with higher reported rates of purchasing more/better food, making large purchases like a car or appliance, returning to school, and saving more for emergencies.

- Student debt holders only say they would save more for retirement if all their student debt were forgiven, which implies that many student debt holders would prioritize other behaviors over the long-term goal of saving for retirement.

- Student debt holders were also twice as likely to report that they would have a child if they received $10,000 of debt forgiveness or complete debt forgiveness as they would if they only received $5,000 of debt forgiveness ($20,000 of debt forgiveness did not produce a statistically significant difference from $5,000).

- Higher amounts of student debt forgiveness were associated with other investment behaviors like starting a business or savings for a down payment on a home, as well as a willingness to spend more on entertainment.

The proportion of debt forgiven matters, too

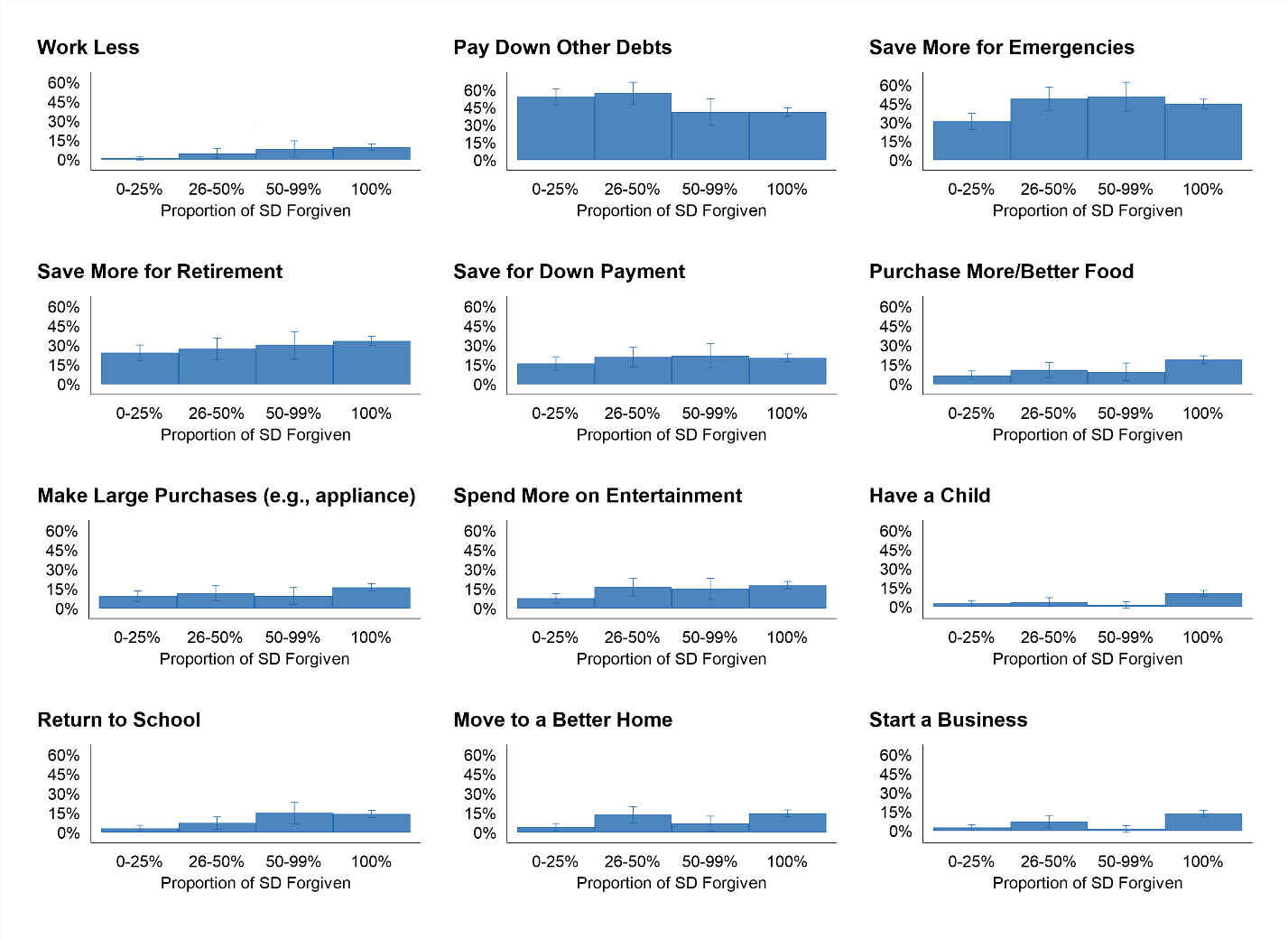

In Figure 2, we shift our focus away from the amount of debt forgiveness to the proportion of debt forgiveness. For this analysis, we converted the amount of forgiveness in each experimental condition to a percentage based on each participant’s reported amount of student debt. That is, someone with $20,000 of student debt assigned to the $5,000 forgiveness condition would have 25 percent of their student debt forgiven, whereas if that person were assigned to the $10,000 forgiveness condition, they would have 50 percent of their debt forgiven. Everyone assigned to Condition 4, as well as everyone assigned to a condition that offered more student debt forgiveness than the amount of debt they owed, were coded as having 100 percent of their student debt forgiven.

Figure 2. The relationship between the proportion of student debt forgiven and household behaviors

Source: Social Policy Institute

Note: These results are from a survey experiment in which student debt holders were randomly assigned to receive one of four levels of student debt forgiveness. The proportions were calculated by diving the amount of student debt held by the proposed amount of student debt forgiven. The impacts of the different proportions of debt forgiveness were estimated using logistic regression models that also controlled for the amount of student debt held by participants. N=1,009. The brackets on each bar represent the 95 percent confidence interval of each estimate.

Interestingly, Figure 2 shows some interesting differences in response patterns when we shift from considering the amount forgiven to the proportion forgiven.

- There is now a clear relationship between the proportion of student debt forgiven and working less—roughly 10 percent of respondents who had 50 percent or more of their student debt forgiven would work less, compared to almost no one having 25 percent or less of their debt forgiven.

- Respondents having less than half of their student debt forgiven were much more likely to report paying down other debts than those with higher proportions of debt forgiven.

- The bulk of respondents saying they would be more likely to have a child if their student debt were forgiven were those who would have all their debt forgiven.

- Respondents became much more likely to report that they would save for emergencies once the proportion of their student debt forgiven exceeds 25 percent, and were more likely to return to school when the proportion exceeds 50 percent.

- Respondents who had all of their debt forgiven were also much more likely to report starting a business as well.

Student debt forgiveness would benefit both high- and low-income households

As a supplemental analysis, we investigated whether or not student debt holders’ incomes influenced the relationship between student debt forgiveness amounts and hypothetical changes in their behaviors. Interestingly, for the vast majority of possible behaviors, both high- and low-income households reported that different amounts of student debt forgiveness would affect them in similar ways. The one primary exception to this was in terms of savings for emergencies—low-income households were much more likely than high-income households to say that they would increase the amount they saved for emergencies as the amount of student debt forgiveness increased.

Implications

These results show two things. First, they show how extensively student debt affects debt holders. The responses to this experiment indicate that student debt is strongly influencing decisions that can have large implications for household economic stability (e.g., emergency savings) and mobility (e.g., saving for a down payment on a home, starting a business). In addition, student debt may be altering the structure of families themselves. Roughly 7 percent of respondents reported that they would be more likely to get married (results not shown) or have children if their student debt were forgiven, indicating that this debt burden is affecting even fundamental decisions about debt holders’ life trajectories.

Second, these results show that the level of student debt forgiveness matters. In particular, setting a student debt forgiveness target too low may not lead to broad-based changes in households’ economic behaviors. However, setting a student debt forgiveness amount at a point where the average debt holder would have more than a quarter of their debt forgiven may yield large changes in savings behaviors, human capital investments (e.g., returning to school), and business starts, without leading to large changes in labor supply.

As policymakers grapple with whether or not to forgive student debt, how much to forgive, and who gets their debt forgiven, it is important to consider the impact of debt forgiveness on household behaviors and how this might differ by the amount of debt held. Our results suggest that larger amounts of debt forgiveness can improve both family stability and upward mobility—especially when these amounts make up a greater proportion of their overall student debt amounts.

A proportional approach to student loan forgiveness

Among those who are considering student debt forgiveness policies, the debate is often framed as a choice between a universal or a targeted policy approach. In this debate, proponents of targeted approaches suggest that universal approaches tend to be inequitable, as they offer benefits to individuals who don’t necessarily need them, and that these approaches tend to be unfair, as these breaks do not apply to previous debt holders who paid off their student loans. As universal approaches tend to be more expensive, proponents of targeted approaches also note fiscal trade-offs, as the money used to pay off the “luxuries” of higher earners could instead be used to help lower earners meet basic needs, such as food and housing.

While the universal approach often focuses on the dollar amount of debt forgiven and the targeted approach often focuses on the income threshold for who would qualify for debt forgiveness, our results suggest that an approach forgiving a proportion of loans should be considered as an option as well. Here, policies could take into account the actual amount of individuals’ debt and forgive a certain proportion of it. This strategy could be applied to either universal or targeted debt forgiveness, or a combination of both approaches. For example, all individuals could have a proportion of their student debt forgiven, and this proportion could increase for lower-income individuals. This approach would have the benefit of addressing the equity concerns of those advocating for a more targeted approach, while still providing real and substantial benefits to student debt holders across the income spectrum.

Related Content

Authors

Commentary

Student debt forgiveness would impact nearly every aspect of people’s lives

May 18, 2021