The neutral rate of interest (also called the long-run equilibrium interest rate, the natural rate and, to insiders, r-star or r*) is the short-term interest rate that would prevail when the economy is at full employment and stable inflation: the rate at which monetary policy is neither contractionary nor expansionary. It is a function of the economy’s underlying characteristics and is not set by the Federal Reserve. It’s usually discussed in real terms, that is, with inflation subtracted out. The neutral rate cannot be observed directly; it can only be estimated.

Why does it matter?

It matters because it affects how the Fed judges whether the interest rates it sets are stimulating or restraining the economy. The Fed may temporarily set the benchmark federal funds rate, the rate at which banks borrow from each other overnight, above the neutral rate to cool the economy or below the neutral rate to stimulate it. The neutral rate is essentially a guidepost for monetary policy.

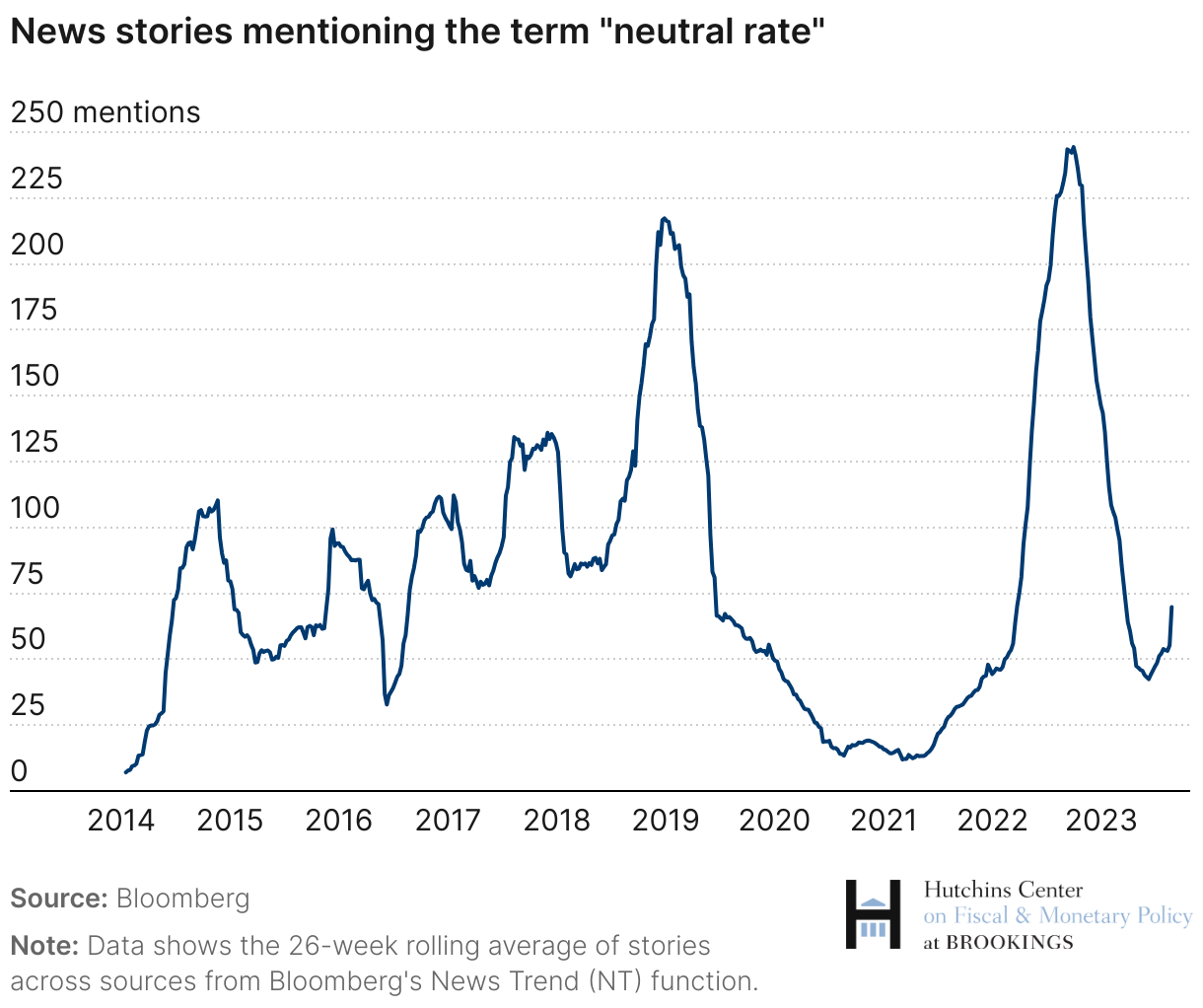

People have been talking more about the neutral rate in recent years. The chart below shows the number of news stories mentioning the term “neutral rate” according to a metric from Bloomberg that aggregates news trends across over 100 sources. The number of news stories mentioning the term “neutral rate” has risen since 2014 as the Fed has raised rates, apart from a substantial drop during the COVID-19 pandemic.

How has the level of the neutral rate changed?

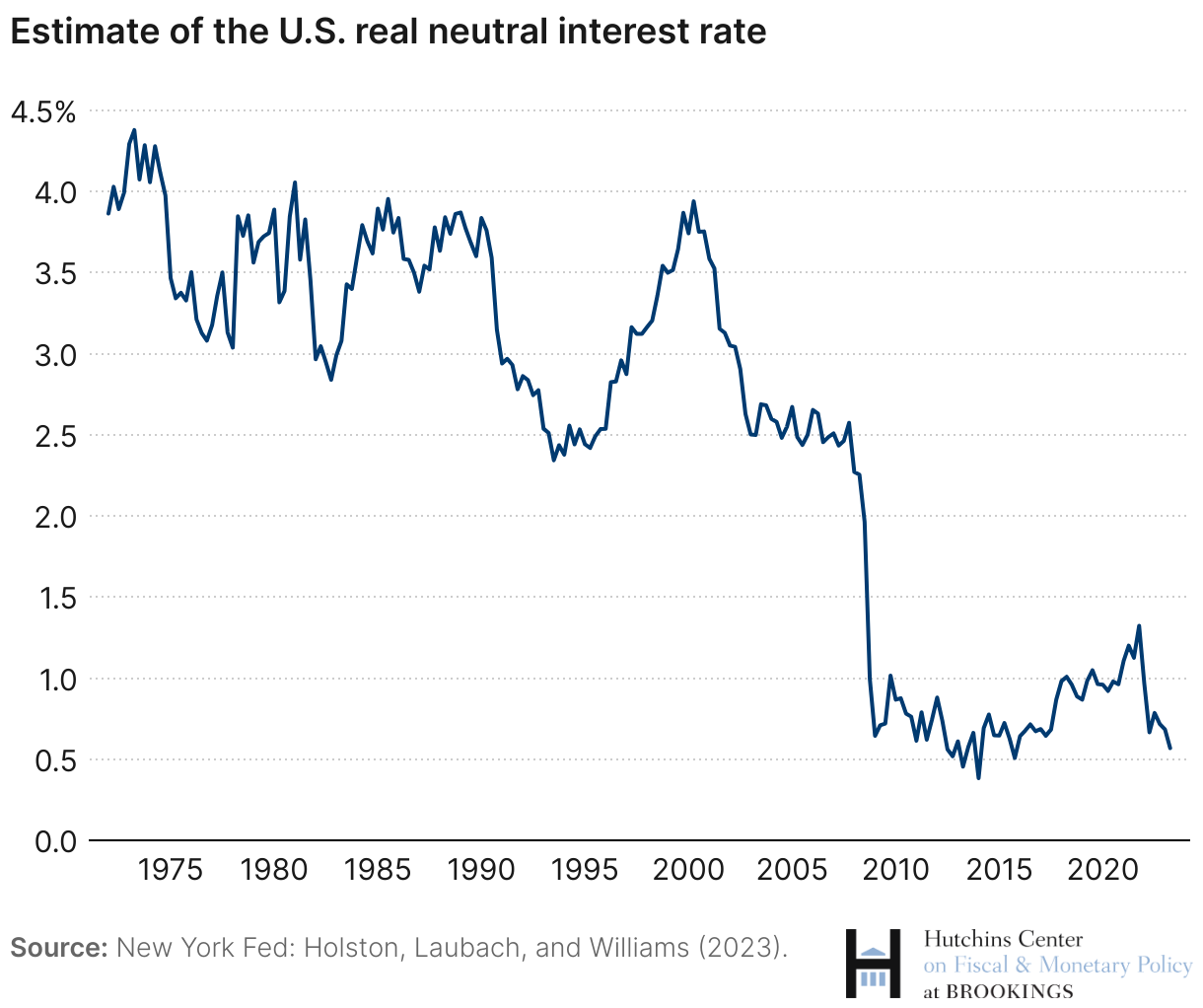

Economists use different models to estimate the neutral rate. Widely cited estimates from Federal Reserve economists Kathryn Holston, Thomas Laubach and John Williams put the real (or inflation-adjusted) neutral rate at about 0.6% in the United States as of the second quarter of 2023. This measure has declined over time. The chart below shows the Holston, Laubach, Williams (HLW) estimate of the long-run neutral rate for the U.S. since the 1970s. Since 1972, the estimated neutral rate has declined by about 3.4 percentage points.

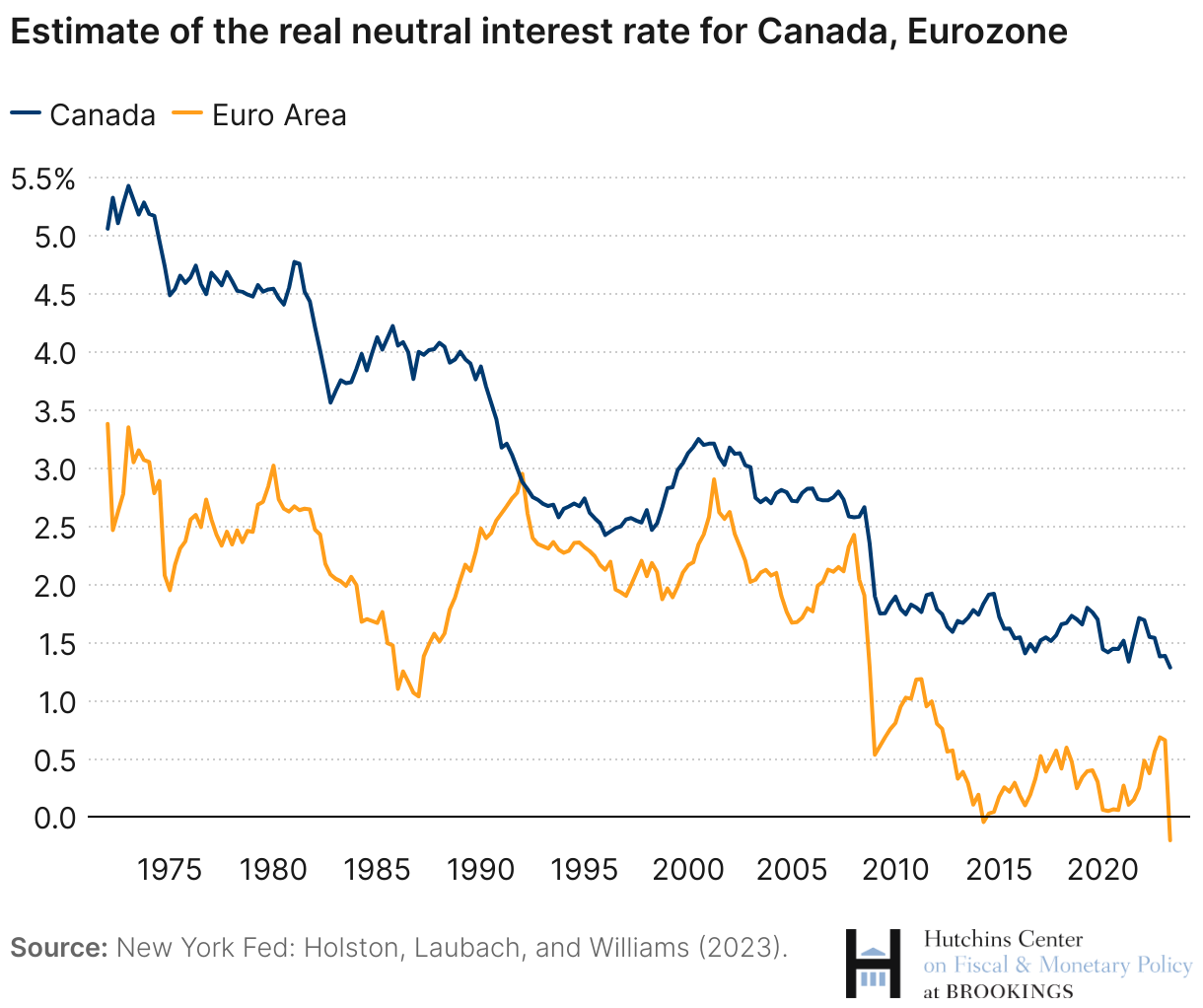

The trend is similar for other advanced economies, indicating that the decline in the neutral rate is not due only to specific factors in the United States. In Canada, the HLW estimate of the neutral rate of interest has fallen by about 3.8 percentage points since 1972. Estimates in Europe are even more stark: the HLW estimate of the neutral rate in the second quarter of 2023 is negative, having fallen about 3.6 percentage points over the same period.

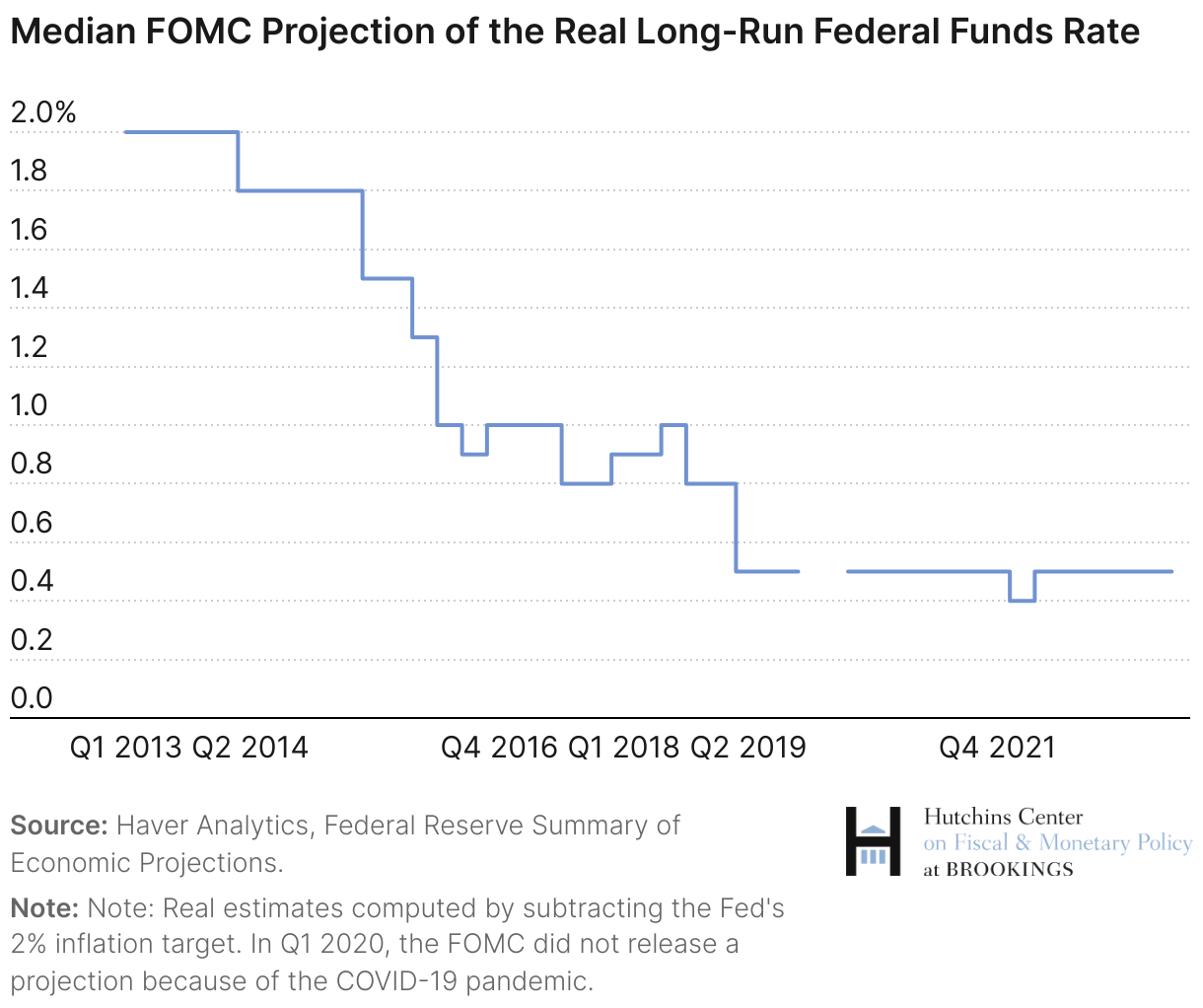

The median projection of members of the Federal Open Market Committee—the Fed governors in Washington and the presidents of the regional Fed banks—puts the long run real neutral interest rate at 0.5% as of the third quarter of 2023. The median projection of the long-run fed funds rate—essentially, an estimate of the neutral rate—has declined over time. It is now 1.5 percentage points lower than it was a decade ago.

What determines the neutral rate of interest in the long term?

In the long run, the neutral rate of interest is determined by the supply of and demand for savings. For example, for firms to make new investments, they need households and other savers to supply the capital to finance that investment. Therefore, total investment in the economy must be equal to the pool of available capital or savings. For that to happen, interest rates need to be high enough to convince savers to save and low enough to incentivize borrowers to borrow. The interest rate that does this in the long run is the neutral rate of interest. Over time, there are several factors that can affect the supply of and demand for saving.

Productivity growth – If firms are more productive, they are able to produce more from a finite set of resources. Higher productivity growth is generally associated with new investment opportunities that increase the demand for capital, driving up interest rates. In recent years, productivity growth has been quite low, driving down the neutral rate.

Secular stagnation – One view that focuses on factors related to aggregate demand is the secular stagnation hypothesis, a view advanced most prominently by former Treasury Secretary Larry Summers. Summers believes that savings have increased while desired investment has fallen, due to a change in economic fundamentals—in particular, modern business requires less capital to function. As a result, he sees low real interest rates as an enduring phenomenon. He reads recent interest rate trends as evidence that the world economy has a chronic shortfall of aggregate demand for new investment and that, barring significant fiscal stimulus, interest rates will remain low for some time.

The global savings glut – As the world becomes more connected, the pool of available savings becomes global, making interest rates more sensitive to capital flows in foreign economies. Former Fed Chair Ben Bernanke argues that, as a result of these forces, a ‘global savings glut’ has driven down the neutral rate of interest. The theory contends that the export-oriented policies of emerging market economies like China flooded capital markets with an increased supply of global savings in the early 2000s. Particularly after a wave of emerging market currency crises in the 1990s, central banks around the world accumulated large foreign exchange reserves to better manage capital flows. This accumulation of foreign reserves, mostly invested in U.S. treasury bills, dramatically increased the supply of savings and drove down the neutral rate. Some research has given credibility to this hypothesis, particularly in the lead up to the Great Recession.

Should these savings and investment trends reverse, the neutral rate of interest could go back up. In April 2015, for example, Bernanke predicted that interest rates would tend to rise if trends in global capital flows reversed. Indeed, recent research suggests that the global savings glut may be moderating. This differs from the secular stagnation theory, which implies a more permanent situation.

Safe assets and risk aversion – Other explanations for the decline in the neutral rate focus on the demand for safe assets. If people become more risk averse, they may save more as a buffer against a future economic downturn. This could increase demand for ultra-safe U.S. Treasury bills, which are very easy to buy and sell and have a very low chance of default—the modern equivalent of stuffing cash under your mattress. Some economists argue that investors became more risk averse after the global financial crisis of 2008, and put more of their money into safe assets instead of riskier (but potentially more productive) investment projects. Some research suggests that increased risk premiums and a greater demand for safe assets is the primary force driving down the neutral rate of interest in recent years.

Demographics – For many, the biggest reason to save is to prepare for retirement. Therefore, the longer people expect to live, the more they should save. As a result, increases in life expectancy in advanced economies have increased the supply of savings and driven down the neutral rate of interest. Of course, once people retire, they draw down their savings. But at the same time, lower fertility rates mean that the U.S. labor force is growing more slowly, so there are fewer workers to supply with capital and, thus, less demand for new investment. That pushes down the neutral rate of interest. Researchers in the U.S., Europe, and Japan have shown that demographic trends have had a large downward effect on interest rates in advanced economies.

What are Fed officials saying about the natural rate?

Fed officials talk a lot about the neutral rate. As the Fed increases interest rates to tame inflation, many have debated if the neutral rate has also increased. New York Fed President John Williams—the same Williams as in Holston, Laubach, and Williams above—believes not, arguing in May 2023 that recent HLW estimates for the U.S. and other advanced economies indicate “there is no evidence that the era of very low natural rates of interest has ended.” On the other hand, Richmond Fed President Tom Barkin has stated that, though too early to draw conclusions, “If the economy is running above potential at 5.25% [nominal] interest rates, then that suggests to me that the neutral rate might be higher than we’ve thought.”

At the September 2023 FOMC meeting, the median projection for the long-run real neutral rate was 0.5%, but five of 17 participating members suggested they believe the rate (the nominal rate minus the Fed’s 2 % inflation target) is now 1% or higher. At their June meeting, only three had projections of 1% or higher. (Back in 2013, the median projection for the long-run real neutral rate was 2.0%.) Powell said, “[I]t may … be that the neutral rate has risen … you do see people raising their estimates of the neutral rate … and that’s part of the explanation for why the economy has been more resilient than expected.”

Given that the neutral rate of interest cannot be observed directly, policymakers must also consider how useful it is to rely on the concept to conduct monetary policy. In a 2018 speech, Williams downplayed the use of the neutral rate. He emphasized that the neutral rate is a good benchmark as a general concept but is less useful as a precise estimate of what rates should be in the short term.

“[…] as we have moved far away from near-zero interest rates, it makes sense to shift away from a focus on normalizing the stance of monetary policy relative to some benchmark ‘neutral’ interest rate, often referred to as ‘r-star.’ Now, I have spent a good deal of my career studying r-star and I find it to be a useful concept for describing the economy’s longer-run behavior. Having said that, at times r-star has actually gotten too much attention in commentary about Fed policy. Back when interest rates were well below neutral, r-star appropriately acted as a pole star for navigation. But, as we have gotten closer to the range of estimates of neutral, what appeared to be a bright point of light is really a fuzzy blur, reflecting the inherent uncertainty in measuring r-star. More than that, r-star is just one factor affecting our decisions, alongside economic and labor market indicators, wage and price inflation, global developments, financial conditions, the risks to the outlook… I think you get the point.”

Fed Chair Jay Powell has long been skeptical of over-relying on the neutral rate to conduct monetary policy. At the Fed’s 2018 Jackson Hole conference, he argued that given the uncertainty in measuring the natural rate, monetary policymakers must be cautious about using it as a guide for conducting monetary policy. Referring to the neutral rate as r-star, as insiders often do, he said:

“[…] These assessments of the values of the stars are imprecise and subject to further revision…[T]he FOMC has been navigating between the shoals of overheating and premature tightening with only a hazy view of what seem to be shifting navigational guides.”

In his 2023 Jackson Hole speech, Chair Powell stressed that rather than relying heavily on estimates of the natural rate to conduct monetary policy, the Fed should adopt a risk management approach by “balancing the risk of tightening monetary policy too much against the risk of tightening too little.” In his view, this is particularly important today when determining how much rates need to increase to slow down inflation: “We see the current stance of policy as restrictive, putting downward pressure on economic activity, hiring, and inflation. But we cannot identify with certainty the neutral rate of interest, and thus there is always uncertainty about the precise level of monetary policy restraint.”

What are the dangers of a low neutral rate?

A low neutral rate of interest leaves monetary policy with less room to cut interest rates in a recession. As former Treasury Secretary Larry Summers noted at a Hutchins Center conference in 2017, the Fed’s response to past recessions has been to cut nominal interest rates by 5.3 percentage points on average. If inflation is 2% and the neutral real rate is 1%, the normal level of nominal interest rates would hover around 3%. In that case, the Fed won’t be able to cut rates by anywhere near 5 percentage points in a recession before hitting zero. Research by Fed economists Michael Kiley and John Roberts shows that with a very low neutral rate of interest, the Fed might have to lower interest rates to zero up to 40% of the time. There are several proposals for how to deal with the problem of the so-called zero lower bound on interest rates. Some include use of the Fed’s unconventional monetary tools, such as quantitative easing and forward guidance. Others focus on a change in the Fed’s monetary policy framework. In any case, as long as the neutral rate remains low, the Fed will have to be creative in conducting monetary policy when the next recession arrives.

This post is an updated version of a 2015 post by Peter Olson and David Wessel.

Related Content

Authors

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

What is the neutral rate of interest?

October 3, 2023