Last week, the Treasury Department and Small Business Administration (SBA) released the most detailed data to date on small business relief provided through the Paycheck Protection Program (PPP), Congress’s central policy for keeping workers in their jobs amid widespread small business closures due to COVID-19. The new data reveals interesting variations in PPP loans across states and metro areas, indicating that federal relief is not going to the places and businesses where it’s needed most.

Like the economic crisis it seeks to mitigate, the scale of PPP is historic. Through July 6, nearly 5,500 lenders distributed 4.9 million loans with an average of $106,000, totaling $521 billion. According to the SBA, these loans went to small businesses that supported over 51 million jobs nationwide, or 84% of the nation’s small business payroll. If the data is accurate, it means that despite notable implementation challenges and emerging evidence that very small business owners (those with under $250,000 in annual revenues) were less likely to apply, the PPP did what it intended to do: provide liquidity relief to a wide swath of small businesses in as short a time as possible.

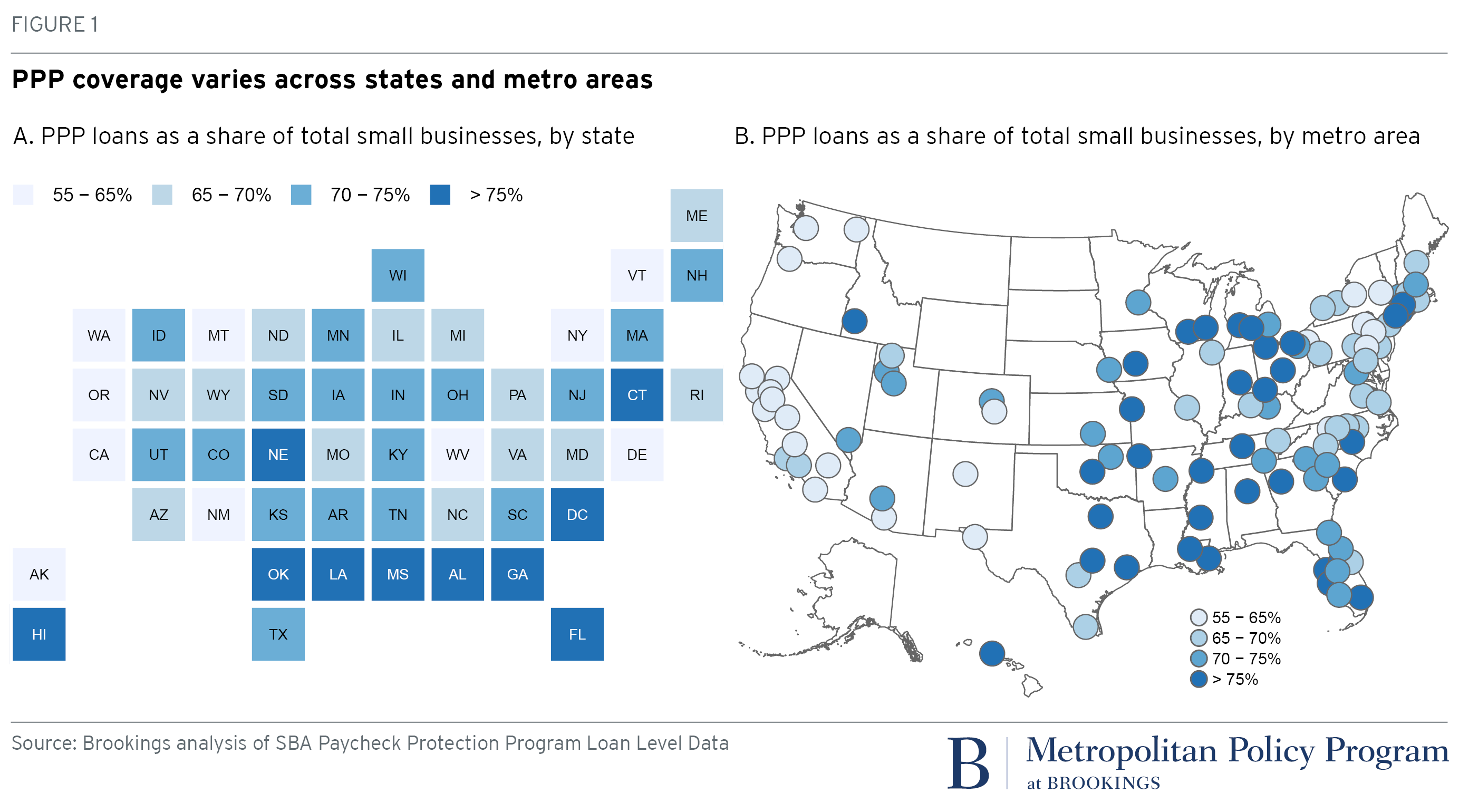

These national aggregates, however, obscure the varying intensity of the small business crisis across places. States and metro areas have experienced differences in the pandemic’s severity and the duration of lockdown orders, as well as industry exposure to both factors. Along those lines, the new Treasury/SBA data provides the clearest picture on how “PPP coverage”—the share of small businesses who received a PPP loan—varied across the nation’s states and regional economies.

To measure PPP coverage, we divide the number of loans approved through the program by the total number of small businesses in 2018, the latest year available (see Appendix Table), for each relevant geography. (Small business data comes from the Census Bureau’s 2018 Annual Business Survey. We define “small businesses” as firms with fewer than 500 employees, excluding PPP recipients who are independent contractors, self-employed individuals, and sole-proprietors because they are not covered in Annual Business Survey.) Unfortunately, PPP disclosure is subject to some big reporting errors, especially in jobs-retained estimates, and the two-year lag in the small business data does not reflect changes in recent years.

Still, this PPP coverage rate provides a rough-but-useful indication the federal relief program’s reach at the national and subnational levels. Overall, 70% of small businesses in the United States received a PPP loan. That share ranged from around 60% in West Coast states to more than 75% in Hawaii, Connecticut, Washington, D.C., and a group of states in the South, including Mississippi, Louisiana, Alabama, Georgia, and Florida (Chart 1a).

Similar patterns are found across major metro areas. Among very large metro areas (those with more than 1 million residents), more than 80% of small businesses received PPP loans in New Orleans, Cincinnati, Atlanta, Miami, and Hartford, Conn. Meanwhile, fewer than 60% of small businesses received loans in Tucson, Ariz., San Francisco, Sacramento, Calif., and San Jose, Calif. (Chart 1b).

The ranges are even wider across large and midsized metro areas (those with populations between 250,000 and 1 million residents). In Jackson, Miss. and Crestview-Fort Walton Beach-Destin, Fla., more than 90% of small businesses received PPP loans, followed closely by tourism hubs such as Honolulu (87%) and Gulfport-Biloxi, Miss. (87%), where the decline in travel has devastated the local economy.

West Coast metro areas such as Salinas, Calif., Visalia, Calif., San Luis Obispo, Calif., Eugene-Springfield, Ore., and Bremerton, Wash. all had fewer than 55% of their small businesses benefit from PPP loans.

Metro area variation in PPP loans could simply reflect that COVID-19 negatively impacted small businesses in some regions more than others, and that greater liquidity challenges resulted in higher rates of PPP application and receipt.

However, Chart 2 indicates the opposite relationship. Data from the Census Bureau’s Small Business Pulse Survey (available for the nation’s 50 largest metro areas) reveals a clear pattern: The cities in which the largest share of small businesses experienced revenue loss had the lowest share of small businesses receiving PPP loans. This pattern is particularly striking for the Bay Area and New York, where more than 65% of small businesses reported revenue decreases in May but fewer than 60% of businesses received PPP loans. Most of the metro areas with lower-than-expected PPP coverage were in California and the Northeast. By contrast, Sunbelt and Midwestern metro areas were not as likely to suffer revenue loss in May, but had much higher PPP coverage.

We are unaware of definitive explanations for these state and metro-level differences. Prior research suggests that the variations can be explained by banking infrastructure, with greater access to PPP in markets where smaller community banks accounted for a higher share of small business lending. But while that relationship existed initially—perhaps due to smaller banks’ ability to dispense loans more quickly—we do not find a strong correlation between the intensity of community banks and the share of small businesses receiving PPP loans (correlation coefficient: 0.07).

A second explanation could be that metro areas vary in the make-up of their small business sectors, with the business size and ownership demographics being pertinent factors in securing financing. There has been some survey evidence that very small businesses were less likely to apply for and receive PPP loans. Consistent with that, we found lower PPP uptake in communities in which there are higher shares of small businesses with fewer than 10 employees (negative correlation of -0.22).

Relatedly, survey evidence suggests that business owners of color have been less likely to receive the full requested amount for PPP loans. In a Global Strategy Group survey of business owners of color conducted in April and May, just 12% of respondents indicated they had received the federal small business assistance they requested, compared to 38% of small business owners overall.

Metro areas with higher shares of minority-owned businesses were less likely to receive PPP loans (negative correlation of -0.4), which is largely driven by a negative relationship between the share of Asian American-owned businesses and PPP loans. This relationship may result from the high share of Asian American-owned businesses in California, where PPP uptake was relatively low. Metro areas with higher shares of Black-owned businesses were more likely to receive PPP loans (correlation of 0.2). These findings do not disprove unequal access to PPP among Black business owners—only that those dynamics do not seem to be driving the metro-level variation.

Since the Treasury/SBA data is subject to revision, these observations should be treated as preliminary. Still, it is clear that policymakers need to understand and reckon with PPP’s spatial mismatch. The program has been extended through August 8 in an attempt to lend out the remaining $130 billion, and future legislative solutions are still being debated in Congress. Local leaders working in economic development and small business support organizations are closest to these challenges, and can inform local, state, and federal small business strategies over the next 24 months. As the virus continues to threaten both lives and businesses, additional federal relief will be necessary—it should go to the people and places that need it most.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Across metro areas, COVID-19 relief loans are helping some places more than others

July 14, 2020