China’s economic rise is one of the factors creating strains in the international financial order. China is already the largest trading nation and the second largest economy. It is likely to emerge in the next few years as the world’s largest net creditor. It is already #2 behind Japan. Until recently, China’s main foreign asset has been central bank reserves, mostly invested in U.S. Treasury bonds and similar instruments.

In the last couple of years, however, this pattern has started to change. China’s reserves peaked at about $4 trillion at the end of 2014. Since then, the People’s Bank of China has sold some reserves, but the country as a whole is still accumulating net foreign assets as evidenced by the large current account surplus. What is new is that the overseas asset purchases are coming from the private sector and state enterprises, not from the official sector. The Institute for International Finance estimated that the net private capital outflow from China was $676 billion in 2015. (That estimate includes outward investments by China’s state enterprises, which strictly speaking are not “private”; the point is to distinguish between official holding of foreign assets at the central bank and more commercial transactions.) As investment opportunities diminish in China owing to excess capacity and declining profitability, this commercial outflow of capital from China is likely to continue at a high level.

Tilted playing field

Most of the major investing countries in the world are developed economies; in addition to making direct investments elsewhere, they tend to be very open to inward investment. China is unusual in that it is a developing country that has emerged as a major investor. China itself is an important destination for foreign direct investment (FDI), and opening to the outside world has been an important part of its reform program since 1978. However, China’s policy is to steer FDI to particular sectors. In general, it has welcomed FDI into most but not all of manufacturing. However, other sectors of the economy are relatively closed to FDI, including mining, construction, and most modern services. It is not surprising that China is less open to FDI than developed economies such as the United States. But it is also the case that China is relatively closed among developing countries.

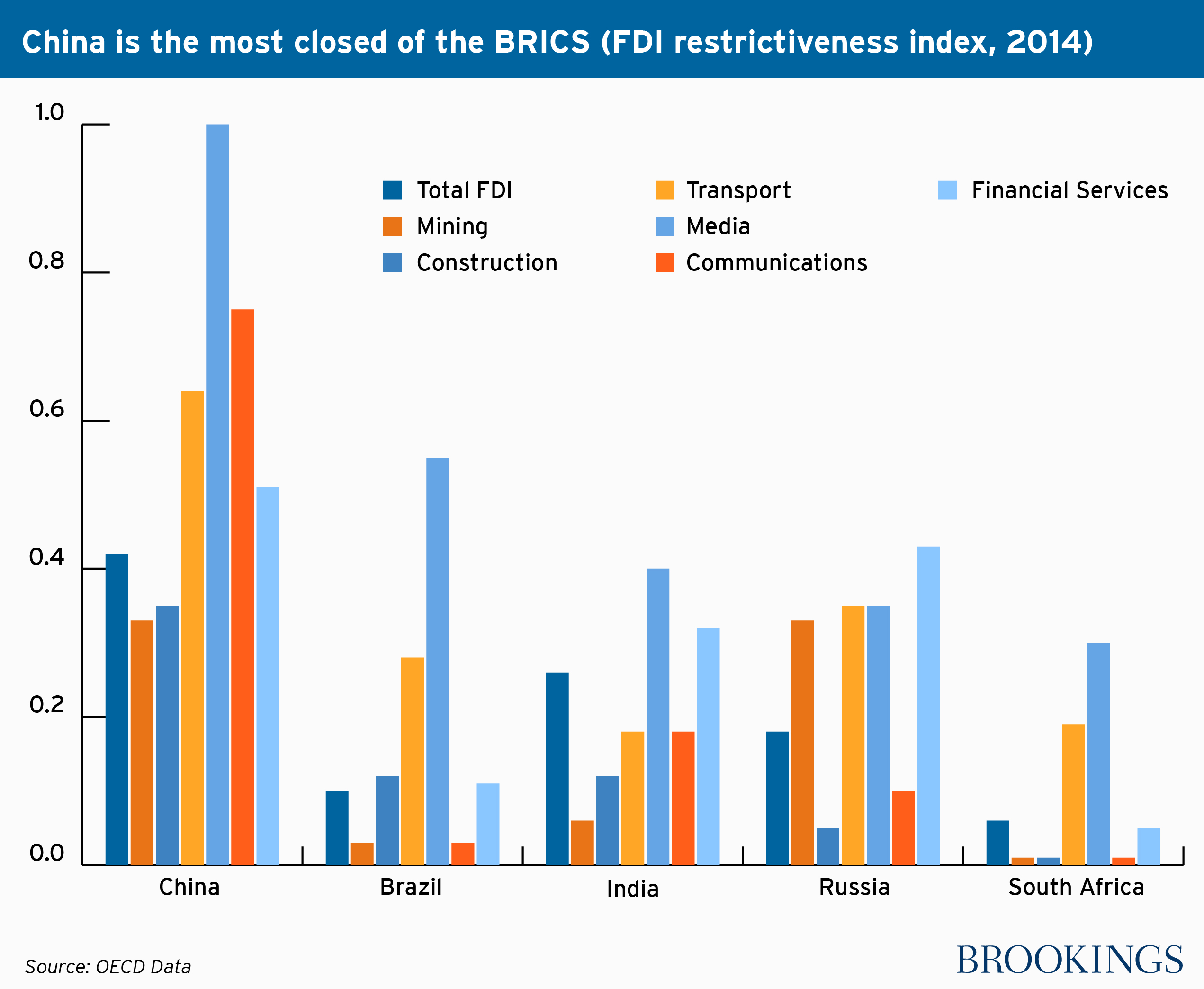

The OECD calculates an index of FDI restrictiveness for OECD countries and major emerging markets. The index is for overall FDI restrictiveness, and also for restrictiveness by sector. China in 2014 was more restrictive than the other BRICS countries (Brazil, Russia, India, and South Africa). Brazil and South Africa are highly open, similar to advanced economies with measures around 0.1 (on a scale of 0=open and 1=closed). India and Russia are less open with overall measures around 0.2. China is the most closed with an index above 0.4. Some of the key sectors in which China is investing abroad, such as mining, infrastructure, and finance, are relatively closed at home.

This lack of reciprocity creates problems for China’s partners. China has the second largest market in the world. In these protected sectors, Chinese firms can grow unfettered by competition, and then use their domestic financial strength to develop overseas operations. In finance, for example, China’s four state-owned commercial banks operate in a domestic market in which foreign investors have been restricted to about 1 percent of the market. The four banks are now among the largest in the world and are expanding overseas. China’s monopoly credit card company, Union Pay, is similarly a world leader based on its protected domestic market. A similar strategy applies in mining and telecommunications.

China is unusual in that it is a developing country that has emerged as a major investor.

This lack of reciprocity creates an unlevel playing field. A concrete example is the acquisition of the U.S. firm Smithfield by the Chinese firm Shuanghui. In a truly open market, Smithfield, with its superior technology and food-safety procedures, may well have taken over Shuanghui and expanded into the rapidly growing Chinese pork market. However, investment restrictions prevented such an option, so the best way for Smithfield to expand into China was to be acquired by the Chinese firm. Smithfield CEO Larry Pope stated the deal would preserve “the same old Smithfield, only with more opportunities and new markets and new frontiers.” No Chinese pork would be imported to the United States, he stated, but rather Shuanghui desired to export American pork to take advantage of growing demand for foreign food products in China due to recent food scandals. Smithfield’s existing management team is expected to remain intact, as is its U.S. workforce.

The United States does not have much leverage to level the playing field. It does have a review process for acquisitions of U.S. firms by foreign ones. The Committee on Foreign Investment in the United States (CFIUS) is chaired by Treasury and includes economic agencies (Commerce, Trade Representative) as well as the Departments of Defense and Homeland Security. By statute, CFIUS can only examine national security issues involved in an acquisition. It reviewed the Smithfield deal and let it proceed because there was no obvious national security issue. CFIUS only reviews about 100 transactions per year and the vast majority of them proceed. This system reflects the U.S. philosophy of being very open to foreign investment.

A thorn in the relationship

Chinese policies create a dilemma for its partners. Taking those policies as given, it would be irrational for economies such as the United States to limit Chinese investments. In the Shuanghui-Smithfield example, the access to the Chinese market gained through the takeover makes the assets of the U.S. firm more valuable and benefits its shareholders. Assuming that the firm really does expand into China, the deal will benefit the workers of the firm as well. It would be even better, however, if China opened up its protected markets so that such expansions could take place in the most efficient way possible. In some cases, that will be Chinese firms acquiring U.S. ones, but in many other cases it would involve U.S. firms expanding into China.

This issue of getting China to open up its protected markets is high on the policy agenda of the United States and other major economies. The United States has been negotiating with China over a Bilateral Investment Treaty (BIT) that would be based on a small negative list; that is, there would be a small number of agreed sectors that remain closed on each side, but otherwise investment would be open in both directions. So far, however, negotiations on the BIT have been slow. It is difficult for China to come up with an offer that includes only a small number of protected sectors. And there are questions as to whether the U.S. Congress would approve an investment treaty with China in the current political environment, even if a good one were negotiated.

The issue of lack of reciprocity between China’s investment openness and the U.S. system is one of the thorniest issues in the bilateral relationship.

The issue of lack of reciprocity between China’s investment openness and the U.S. system is one of the thorniest issues in the bilateral relationship. A new president will have to take a serious look at the CFIUS process and the enabling legislation and consider what combination of carrots and sticks would accelerate the opening of China’s markets. In terms of sticks, the United States could consider an amendment to the CFIUS legislation that would limit acquisitions by state enterprises from countries with which the United States does not have a bilateral investment treaty. In terms of carrots, the best move for the United States is to approve the Trans-Pacific Partnership and implement it well so that there is deeper integration among like-minded countries in Asia-Pacific. Success in this will encourage China to open up further and eventually meet the high standards set by TPP. Greater investment openness is part of China’s own reform plan but it clearly needs incentives to make real progress.

For more on this and related topics, please see David Dollar’s new paper, “China as a global investor.”

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

What do China’s global investments mean for China, the U.S., and the world?

May 18, 2016