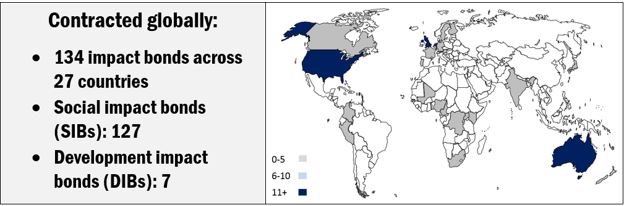

2018 was an eventful year for the impact bond market. The number of contracted impact bonds continued to grow: As of January 1, 2019, the Brookings Global Impact Bond Database tracked 134 impact bonds as either completed or in implementation, up from 110 last year. Understanding the potential value of impact bonds as an innovative financing mechanism depends on several key factors. Below we provide a global snapshot of the impact bonds landscape from the past year and forecast the pivotal role of data in supporting the growth of outcome-based contracting in 2019.

What does the impact bond market look like?

Most of these contracts are still social impact bonds (SIBs), where the outcome funder is the government—there are just seven development impact bonds (DIBs), with third-party funders paying for outcomes. Social welfare and employment remain the most popular sectors for impact bonds, together making up 69 percent of contracts. While 27 countries have now contracted impact bonds, over a third of the contracts are in the U.K., with just one or two contracts signed in most other countries. Further details from the database can be found in our Impact Bonds Snapshot: January 2019.

Fewer contracts were signed in 2018 than 2017, with just 24 new impact bonds contracted, down from 34 in 2017. New contracts this year were split fairly evenly between social welfare (9), employment (6), health (5), and education (4). Most of these contracts were in high-income countries; however we saw four new contracts across low- and middle-income countries. Cameroon launched a DIB for cataract patients, while India launched its third DIB to date—the Quality Education India DIB—with three service providers offering different interventions to improve learning outcomes. South Africa launched two SIBs, one for youth employment, and another for early childhood development.

Are impact bonds a success?

At least once a week people ask us to weigh in on whether impact bonds are successful. In our view, the answer to this question is not a simple ‘yes’ or ‘no.’ Instead, we think about it in terms of five potential measures of success. The first measure of success is simply: Is there a demand for impact bonds or outcome-based contracting? Second, do impact bonds reach the populations in need? And third, do the contracts achieve outcomes (and are investors receiving positive returns)? A fourth measure of success considers whether impact bonds are achieving something besides outcomes: In other words, what effects might this contracting mechanism have on the wider ecosystem? Finally, are the deals efficient?

While the majority of impact bonds are still in the implementation phase, an increasing number of the early deals are ending, which allows us to answer some of these questions. More than a quarter of the 134 contracts have now completed, and there is a growing body of evidence on the successes, challenges, and lessons learned from the first cohort of deals.

As described above, the impact bond market is growing steadily and has spread across many regions. But what should this be benchmarked against to measure success? In terms of upfront capital commitment, the impact bond market remains small at about $370 million invested to date (over eight years) compared to the $228 billion in impact assets under management in 2018.

From the available data on the completed deals, we know that most have repaid investors their principal plus positive returns, and that just one–the NYC Able Project for Incarcerated Youth–made no outcome payments. Most of the completed deals so far have been in the U.K., where a range of process and impact evaluations have been published.

2018 marked the final year of the Educate Girls DIB, the first education impact bond in a low- or middle-income country, which we have followed closely since its launch in 2015. The evaluation by IDinsight found that Educate Girls, the service provider, was able to enroll 768 out-of-school girls, and to achieve learning outcomes that were 160 percent of the final target.

We will focus on tracking the success of impact bonds around the world, across a range of criteria, in the coming months. It is important to note the continued difficulty in isolating the “impact bond effect”—that is whether using the impact bond financing mechanism actually adds value. Even for impact bonds where rigorous evaluations were used to measure outcomes, only the effectiveness of the intervention itself was captured, so we don’t know if the same results could have been achieved with input-based financing, traditional payment by results, or even just providing cash with no strings attached.

Data needs for achieving outcomes

One of the key observations from our study of the global impact bond market is the role of data, and the need for service providers to be able to gather, analyze, and respond to information to achieve outcomes. Through our conversations with impact bond actors around the world, we know that intermediaries and investors are often closely engaged with service providers, supporting the design and implementation of improved systems of performance management. If impact bonds are to increase in scale—for example through the ambitious Education Outcome Funds for India, or for Africa and the Middle East—the demand for timely, usable data, and the systems that support their use, will continue to grow. We are interested in how technology, and in particular tech tools and platforms for data collection, can help support outcome-based contracting to ensure that implementers can make informed decisions and improve their practice. In 2019, we will further research the availability of tech tools for data-informed decisionmaking in outcome-based financing, and the characteristics that facilitate their use.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

A global snapshot: Impact bonds in 2018

January 2, 2019