We write as engaged researchers in the area of student loans with a plethora of hands-on policy experience, having been involved in detailed analyses and modelling of university financing systems since 1989 in a number of countries. These include, inter alia, Australia, the U.K., Colombia, Chile, Japan, Brazil, the U.S., Malaysia, China, Ireland, Germany, South Korea, Vietnam, and Indonesia.

Based on our combined 60-plus years of research and international engagement in higher education financing, the two key lessons for student loan repayment are:

- Income-driven repayment plans are vastly superior to the standard time-based repayment plans; and

- The key to the U.S. government transforming higher education financing is having one simple income-driven repayment plan and to use employer withholding as the collection mechanism.

Now is a critical time for our contribution given the recent attempts at loan forgiveness by the Biden administration, the planned reforms to the U.S. income-driven repayment (IDR) plan, and the government’s call for submissions and suggestions related to the suggested changes. All of our analysis relates directly or indirectly to the future design of U.S. IDR loans (see Chapman and Dearden (2023). A description of the key elements of the Australian and U.K. systems and how they compare with current U.S. IDR plans was provided in the 2023 Economic Report of the President (see Box 5-2 on p. 168).

Lesson One: Why is time-based repayment inferior to income-driven repayment?

Under a time-based loan repayment plan, borrowers make the same monthly payment over a set period of time. For example, in the United States, the standard repayment plan divides loan payments evenly across ten years. But an income-based repayment plan ensures loans are repaid only when the debtor’s income exceeds a certain annual amount, at a given percentage of income.

Many debtors will at some point(s) experience difficulties repaying because of low incomes—from unemployment, an accident or poor health, or graduating when job opportunities are scarce. This will likely then lead to loan deferral and for some, default, which is a very bad outcome resulting in major damage to their credit reputations when using the standard time-based repayment plan. It may also lead to suboptimal career choices and family formation decisions.

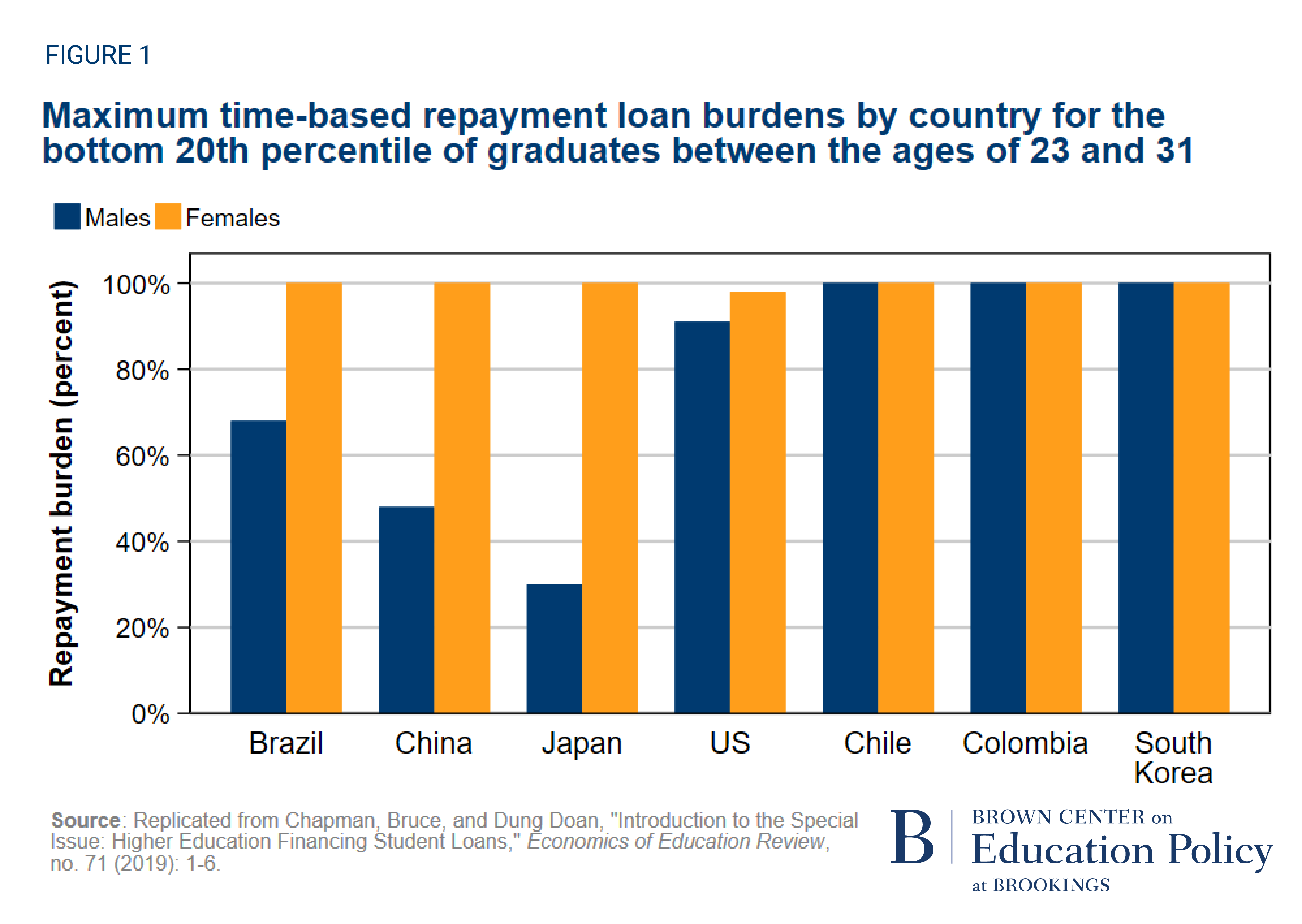

We measure the consequences of time-based repayment plans with the concept of a loan “repayment burden,” defined as the proportion of personal income required to repay loans each period. If “repayment burden” is 100% in a given month, that means that all income has to be used for loan repayment, leaving nothing to live on. In Figure 1 we graph the maximum repayment burden faced by young graduates (ages 23 to 31) whose incomes put them at the 20th percentile of all graduates in countries with time-based repayment plans (this figure is from Chapman and Doan (2019)).

We find that in all countries, females at the 20th percentile of the graduate earnings distribution will at some point (generally in the first year that they must start making loan repayments) have to use 98% or more of their incomes to make their regular loan payment. For male graduates in the 20th percentile of the graduate income distribution in their country, the maximum repayment burdens are 68% or more for five of the seven countries, including the United States. Under time-based repayment, the lowest-income graduates will experience considerable consumption hardship and fairly high probabilities of default.

In contrast, an income-driven repayment approach safeguards against repayment burden by setting a maximum monthly payment at a low level. For example, in England, New Zealand, Australia, and Hungary, the monthly repayment obligations can never be more than 9%, 12%, 10%, and 6% of incomes, respectively. Thus, there are no repayment hardships, nor are there any defaults.

Herein lies the essential message: Standard, fixed repayment plans lead to major repayment risks and default, while an income-driven approach provides insurance against all financial adversity. Currently there are at least 12 million U.S. former student loan defaulters (just about all of them hugely disadvantaged) labelled as credit risks, and in other countries with similar time-based repayment approaches student loan default rates range from 40% to 70%. In contrast, in Australia, the U.K., New Zealand, and Hungary, there is no hardship nor default.

In addition, a well-designed income-driven repayment plan can provide higher long-term revenue streams to the government compared to time-based repayment. In our recent comment submitted to the U.S. Department of Education, we illustrate this with a simulation using administrative data from Colombia with actual time-based loan repayments, defaults, and earnings over an extended period. How is this achieved? When loan repayments are determined by earnings rather than equally distributed across a fixed loan term, lower-income borrowers can extend payments over a longer period of time and their repayment amounts automatically adjust if borrowers fall on hard times. Barr, Chapman, Dearden, and Dynarski show that in the case of the U.S., a well-designed income-based repayment plan would mean high-earning graduates pay back more quickly than under the current time-based repayment system, and low-earning graduates will pay back over a longer time horizon without the taxpayer or loan holder facing any costs associated with default. They also highlight the importance of other parameters of the IDR plan, such as the real interest rate, repayment threshold, repayment rates, and whether the loan is written off after some period as is the case in England (after 25, 30, or 40 years).

In summary, for both borrowers and governments, income-driven repayment is a more efficient and equitable approach to student loans, and time-based repayment plans everywhere should be assigned to the wastebasket of higher education financing history. But for this to be true, income-driven repayments programs have to be collected efficiently, and this is our next lesson.

Lesson Two: A New U.S. Income-Driven Loan Repayment System Collected through Employer Withholding

The newly proposed income-driven repayment plan in the U.S. would determine monthly repayments using borrowers’ previous year’s income declaration, the way in which all such loans for the U.S. have been designed. This is a critical mistake.

A much fairer, better targeted, and more efficient system involves instead the use of employer withholding, the tried-and-true collection mechanism for income taxes, social security payments, and wage garnishing used everywhere in the world. It is the method highly successfully used for ICL in Australia, the U.K., and New Zealand.

There are significant advantages to employer withholding. For employers, it is a simple matter of an additional element of withholding on behalf of the government and requires little more than an adjustment to the existing payroll procedures. For borrowers, it is all automatic: There is nothing to worry about, no forms to fill in, and no need for involvement in complicated choices between alternatives. It is a stress- and transaction-free process. Stiglitz argues that these efficiencies are the key to a successful student loan system, a point highlighted also by Hauptman.

Moreover, with employer withholding, the marginal cost of collection to the government is very small because the system builds on existing employer withholding arrangements (e.g., for the collection of income taxes and social security contributions). Note that employer withholding would cut out third-party loan servicers in the United States. Borrowers’ employers would perform the administrative and payment processing functions currently executed by loan servicers. The outstanding debt collection functions these loan services also provide at present will no longer be needed moving forward. Though this proposal essentially shutters a small industry in the U.S., we feel the long-term benefits to the government and borrowers more than justifies this cost.

Additionally, a major benefit of employer withholding is that repayments reflect the borrower’s current, not past, financial circumstances. This is especially important for low-income borrowers and borrowers at the beginning of their careers who often do not have stable and predictable incomes. Accordingly, the U.S. income-driven repayment systems in use are not really income driven, not in practice or reality.

There are other critical issues concerning income-driven repayment system design as Dynarski persuasively argues, such as the powerful need for simplicity and to avoid students having to choose between complex and hard-to-understand options. Chingos, Delisle, and Cohn stress the importance of minimizing unnecessary subsidies. Best and Best, Chapman, and Mitchell highlight the restrictions of loan availability to properly accredited educational institutions.

Our Bottom Line

From our unique research with and policy understanding of student loans, we can come to one line for the U.S. reform agenda: The whole system can be made so much fairer, more efficient, more progressive, and simpler, with the institution of a single income-driven loan repayment system for all borrowers based on transparent principles made clear from overseas experience using employer withholding.

Related Content

Authors

Commentary

Key lessons for the U.S. from analyses of student loan systems all around the world

April 23, 2023