This week, December 10-14, marks the Program for Infrastructure Development in Africa (PIDA) week. This year’s conference is under the theme, “Enhancing Trade and Economic Transformation through Regional Infrastructure Development.” As African leaders tackle various challenges related to infrastructure at the conference in Swakopmund, Namibia, a major theme will be strategies for financing infrastructure development.

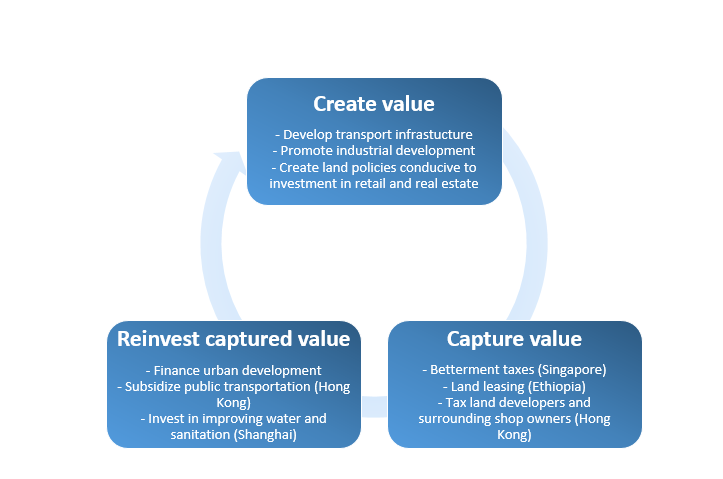

One financing tool for infrastructure in African cities we believe has potential to reap major benefits is land value capture. The definition of land value capture we use in this context is that it is a method of financing urbanization through the recovery of profit generated by the increasing value of property as a result of public infrastructure investment. Land value capture can take several forms as the value of land is determined by a list of factors such as public investment in infrastructure, changes in land use regulations, demographic change and economic development, private investment in land, and land productivity. But can Africa take advantage of this tool?

Land value capture is also used as an instrument for raising infrastructure development funds. Land value capture tools are varied; they include tax levies, the sale of development rights, public land leasing, land acquisition and resale, land sales, and impact fees, among others. Land acquisition and resale is a method through which the increasing value of land around newly developed infrastructure development is capitalized. For instance, when a new metro system is built, the land surrounding the new stations sees its value increase. Consequently, there exists a virtuous circle between infrastructure development and land value capture.

Figure 1: The land value capture process

Countries that are presently in the process of developing their infrastructure have the most room for land value capture. The land value capture literature finds a positive relationship between transport infrastructure and land value, as noted above. A paper by Mercy Brown-Luthango on the potential for land value capture in midst of South Africa’s recent transport infrastructure development suggests the levy of betterment taxes. This tax is based on the increase of the land value surrounding the newly created transport system. Singapore has levied a betterment tax under the name “development tax.” In this case, land developers pay the Singapore government 50 percent of the increase in land value, which results from the development of said land. Given South Africa’s long history of tax collection and its relatively well-functioning tax collecting infrastructure, the country’s large cities such as Cape Town and Johannesburg may be good fits for implementing this system to capture the increased land value generated by the country’s newly developed transportation systems.

Countries that are presently in the process of developing their infrastructure have the most room for land value capture. The land value capture literature finds a positive relationship between transport infrastructure and land value, as noted above. A paper by Mercy Brown-Luthango on the potential for land value capture in midst of South Africa’s recent transport infrastructure development suggests the levy of betterment taxes. This tax is based on the increase of the land value surrounding the newly created transport system. Singapore has levied a betterment tax under the name “development tax.” In this case, land developers pay the Singapore government 50 percent of the increase in land value, which results from the development of said land. Given South Africa’s long history of tax collection and its relatively well-functioning tax collecting infrastructure, the country’s large cities such as Cape Town and Johannesburg may be good fits for implementing this system to capture the increased land value generated by the country’s newly developed transportation systems.

The city-state of Hong Kong presents one of the most complete cases of land value capture to date. Hong Kong has explored various ways of taking advantage of its growth and the accompanying growing infrastructure. The Mass Transit Railway (MTR) Corporation manages Hong Kong’s rail and bus system, one of the most profitable in the world: In 2012, the MTR produced a $2 billion profit. In addition to revenue from user fees, the MTR creates deals with surrounding businesses and land developers to receive a share of their profits in exchange for transporting their customers. In turn, the fees levied from the surrounding businesses serve as a subsidy for public transportation, and part of the funds are also reinvested in real estate. The success of this model was rendered possible by a number of enabling conditions. Hong Kong is a dense territory (6,690 people per square kilometers) with a low car ownership rate and a high reliance on public transportation. Moreover, land in Hong Kong is relatively scarce, thus limiting developers’ ability to refuse entering into partnerships with the MTR. Third, Hong Kong’s land policy is set to facilitate the planning and granting of development rights. All land in Hong Kong is owned by the government, which then issues leases.

Given these factors, it could be difficult to replicate the Hong Kong model in an African setting. First, African cities are relatively not as dense (though there are exceptions such as Lagos and Kinshasa). Second, African cities have relatively poorly developed public transportation systems. In order for a transportation authority to levy fees from surrounding developments, and for that development to, in turn, subsidize the public transportation system, that system must have the ability to handle high traffic and attract shop owners and land developers to the surrounding area. In addition, African cities have relatively informal or sometimes unaffordable public transportation systems.

Using land value capture as a capital mobilization instrument requires that a number of factors be in place, including enabling policies, support from national government, a powerful local government, an established financial sector, and existing public-private partnerships. For example, according to the World Bank’s Doing Business 2017 report, poor land ownership policies hinder property development in Africa. The quality of land administration index in the Doing Business report measures the efficiency of land registration and mapping systems, i.e., the registry of property showing the extent, value, and ownership of land. In other words, the indicator measures the ease of acquiring, making use of, and disposing of land rights, and provides information on the location and ownership of land parcels. On a scale of 0-30, the regional average lies at 8.4, the lowest of all regions, and less than half the OECD average 22.7 (Figure 2). Still, many countries, including Kenya, Mauritius, Rwanda, and Senegal, have been implementing reforms to improve land registry in their countries.

Figure 2. Quality of Land Administration Index

The many factors that hinder Africa’s ability to attract investment capital also obstruct the continent’s ability to capitalize on land value capture. Such factors include a poor institutional environment, the difficulties in doing business and unreliable or inexistent infrastructure, in addition to insecure land ownership. Addressing these constraints may go a long way in seeing flourishing private developers in the African market and improving infrastructure in African cities.

Related Content

Authors

Commentary

Financing African cities: What is the role of land value capture?

December 14, 2017