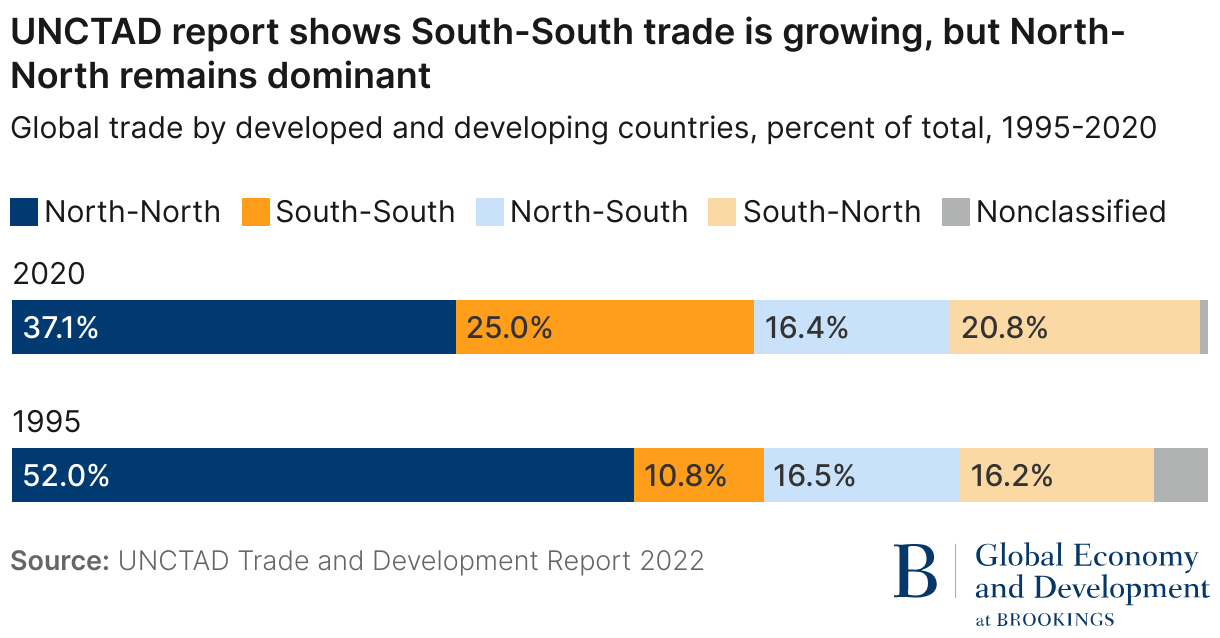

The standard narrative suggests that, although rising, South-South trade—trade between developing economies or the Global South—is still overshadowed by North-North trade—trade between high-income economies or the Global North. For instance, in their Trade and Development Report 2022, economists from the U.N. Conference on Trade and Development (UNCTAD) recognized the changed structure of international trade over the past 25 years. They noted that the share of trade between developed economies had declined by nearly 15% since 1995, having been superseded by growth in South-South trade, which was up 14.1%. But the figures they arrived at still suggest that North-North trade (37.1%) dominates over South-South (25%) (Figure 1).

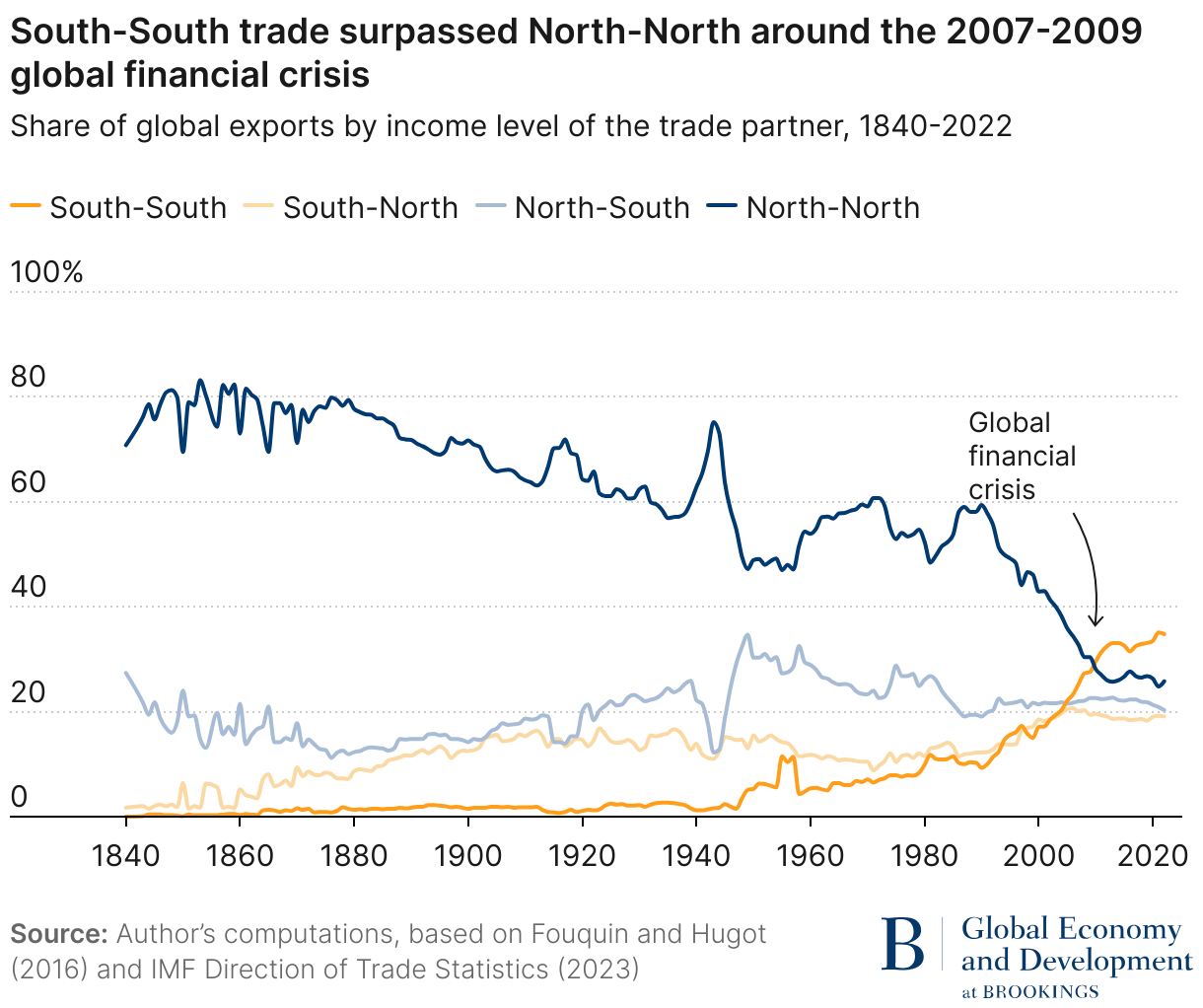

Is this narrative correct? It is ultimately a question of perspective. Using a historic bilateral trade dataset, Ortiz-Ospina, Beltekian and Roser took a long-run look at the trends in North-North and South-South trade from 1840-2014. But they started from a different premise. They defined two blocks in the world—”rich” and ”poor” (analogous to our North-South classification)—on the basis of a group of 24 countries identified as “rich”1 back in 1980, defining the rest of the countries in the world as “poor.”

What they then did differs from many similar exercises—they kept the group of ”rich” countries constant over the whole period. This is surely methodologically correct given that the number of countries classified as “high-income” has changed markedly since 1990, increasing from 40 to 83. If we were to define “North” by the ”high-income” countries of today, then almost by definition “Northern” countries would always be responsible for the bulk of global trade. In other words, if we keep adding countries to the “high-income” group over time as the classifications change, inevitably Northern countries will continue to dominate global trade. But this is arguably not the right optic through which to see the rise of South-South trade.

A more accurate portrayal of the trade data?

In Figure 2, I build on Ortiz-Espina et. al.’s analysis and update it to 2022. The results of the computations are unambiguous: In the mid-19th century, the dominance of trade between “rich” countries (North-North) was stark, accounting for 70-80% of all global trade, with negligible commerce between developing countries.2 Although there was subsequently a gradual decline in that share (interrupted only by the Second World War), even by the early 1990s North-North trade still accounted for nearly 60% of the total. But in the early 1990s, there seems to have been a turning point that signaled a period of sharp decline in the North-North share. Around the time of the global financial crisis, South-South trade surpassed North-North trade for the first time, and today 35% of global trade is accounted for by South-South merchandise trade, and just 25% by North-North.

Needless to say, this represents a dramatic departure from the past and has a number of important implications for development policy, in part because there is a wealth of studies that show that South-South trade tends to be more diversified, better at inducing technology transfer, and more pro-developmental than trade between developing and high-income countries.

Implications for Africa and the AfCFTA

What does this mean for the African Continental Free Trade Area (AfCFTA), if anything? At a basic level, it implies that the dynamics of global trade have changed, and that focusing efforts on trying to export and diversify through increasing trade with high-income economies may no longer be the best strategic choice. To be sure, these are not new arguments—concerns were raised in the 1980s about the difficulties developing countries were facing in increasing their diversified exports to high-income economies, and consequently the advice was to double down on South-South trade. That advice petered out at the end of the 1980s as South-South trade failed to take off in the expected way.

Arguably, however, Figure 2 suggests that things are different this time around. For instance, between 1990 and 2022, China’s bilateral trade with Africa rose from just $2.7 billion to more than $209 billion, and China has now become Africa’s single largest trading partner. To be sure, there are senses in which African trade with China replicates some of the negative characteristics of North-South trade—African exports to China are almost exclusively commodities while imports from China are manufactured goods. However, there is also evidence of positive developmental implications: In a study of Chinese capital goods supplied to Tanzania, Kenya, and Uganda, the authors concluded that the capital equipment was distinct from Northern-origin capital goods—it was more economically accessible, profitable to users, and demonstrably more appropriate to the operating conditions in these three economies.

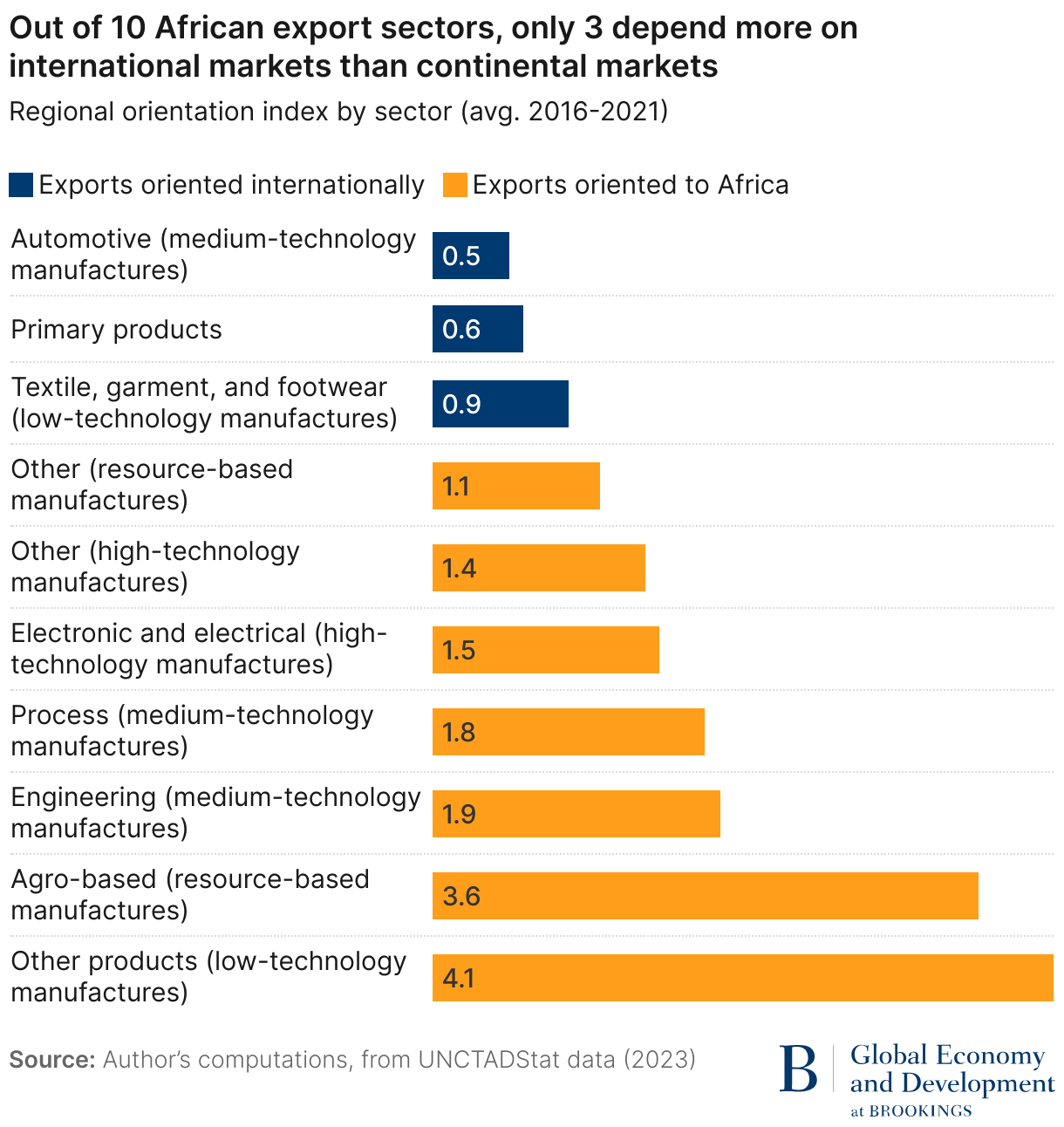

It would equally be wrong to underestimate the importance of the African market itself. In an earlier paper, I argued that the economic significance of intra-African trade has been persistently underestimated. That argument is brought home forcefully by referring to Figure 3, which shows the regional orientation index of aggregate exports for the whole of the African continent. The index is a measure of the importance of intra-regional exports relative to extra-regional exports: It tells us whether exports of a particular product from the region under study to a given destination are greater than exports of the same product to other destinations. It ranges from 0 to infinity, with a value greater than 1 implying a regional bias in exports. The data is broken down by sector using the well-known classification of exports provided by Sanjaya Lall, according to the level of technological sophistication (Figure 3).

This index provides some striking results: Of the 10 categories of exports, just three sectors are still more dependent on the international market rather than the continental one—predictably, the primary sector (commodities still accounted for nearly 80% of total African exports in 2022); textiles and clothing (which have become heavily oriented to the U.S. and European markets through the preferential market access schemes of the African Growth and Opportunity Act and Everything But Arms); and the automotive sector (essentially reflecting the orientation of the Moroccan and South African automobile industries, which export principally to Europe and North America). Seven of the 10 sectors are already more dependent on the African market than on the international market—including such strategically important sectors as low-technology manufactures, agro-processing, engineering, electronics, and even high-technology exports.

Thus, growing South-South dominance in global trade is not just a phenomenon related to the precipitous rise of China and other emerging Asian economies—it is also revindicated within the African continent. As Francis Mangeni and I argue in our forthcoming book, it is important that policymakers are fully aware of these dynamics and prioritize leveraging the full developmental potential of intra-African trade through rapid implementation of the AfCFTA.

Author

Related Content

-

Acknowledgements and disclosures

The author would like to thanks Professor Raphie Kaplinsky for some very earlier suggestions on an earlier version of this article. He would also like to thank Insaf Guedidii for assistance with the data for Figure 2.

-

Footnotes

- Ortiz-Ospina et. al. use the classification of UNDP (2013) (“Human Development Report 2013: The Rise of the South: Human Progress in a Diverse World,” Figure 2.1.), whereby the rich country group is defined in 1980 as: Australia, Austria, Belgium, Canada, Cyprus, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Israel, Italy, Japan, Luxembourg, Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, United Kingdom, and the United States.

- Remember that this was a period characterised by the first wave of industrialisation in the West: The concentration of manufacturing reached its zenith in the mid-1880s, when the U.K. accounted for an estimated 43% of world manufactured exports.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Why South-South trade is already greater than North-North trade—and what it means for Africa

December 11, 2023