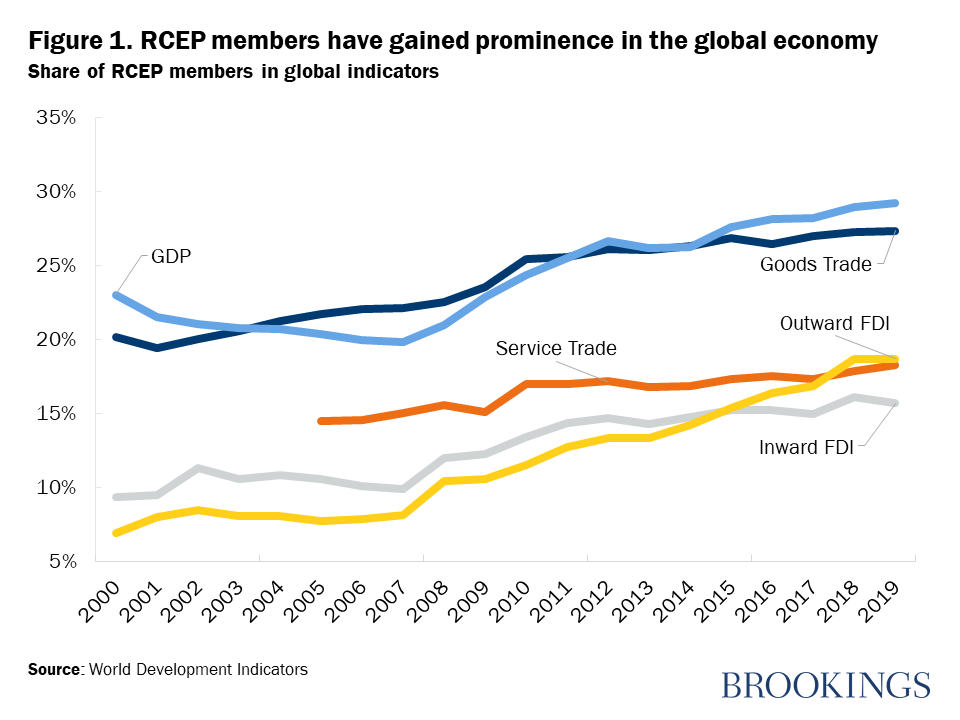

On November 15, 15 countries in East Asia and the Pacific signed the Regional Economic Partnership Agreement (RCEP), creating the world’s largest trading bloc. This signing arguably marks one of the most remarkable responses of global leaders to the global protectionist trends witnessed since 2016. RCEP negotiations started in 2012 with 16 countries including the 10 Association of Southeast Asian Nations (ASEAN) countries, China, Japan, India, South Korea, Australia, and New Zealand. Even with India’s eventual withdrawal in 2019, the agreement is still the world’s largest, encompassing 30 percent of global GDP and 27 percent of global merchandise trade (Figure 1). RCEP also comprises over 18 percent of services trade and 19 percent of foreign direct investment (FDI) outflows.

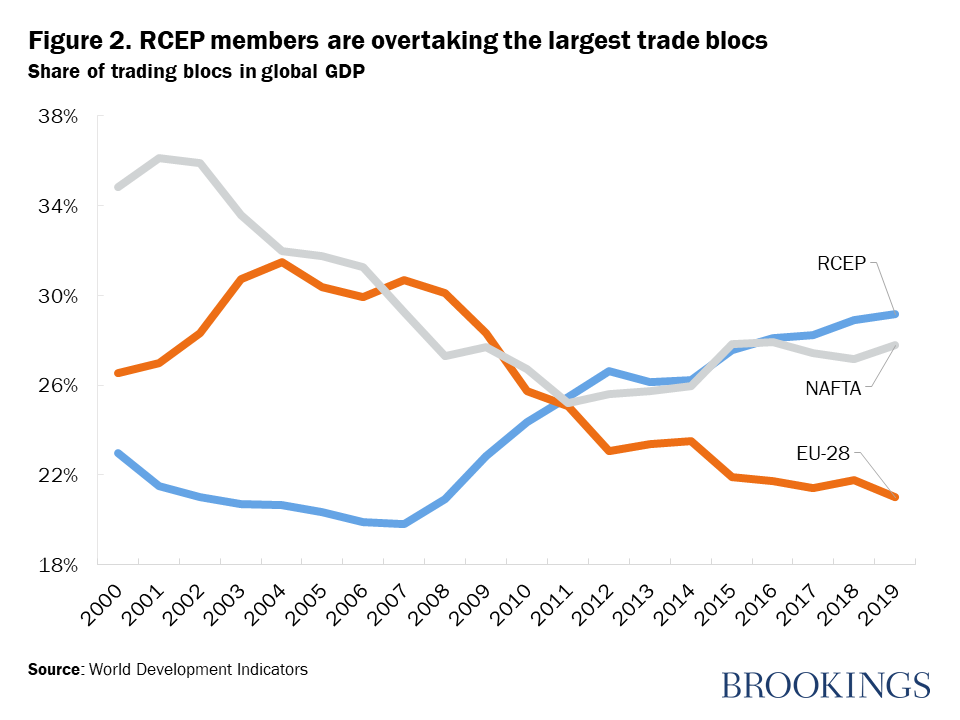

Driven by China, the RCEP trade bloc has gained prominence in global trade and investment, and has outstripped the growth of large high-income trade blocs over the past decades. The remarkable growth of China and Southeast Asian economies is reflected in the rising share of the RCEP bloc in global GDP, trade, and FDI over the past two decades (Figure 1). This has also propelled the RCEP to overtake trading blocs, which were much larger at the beginning of the century, including the North America Free Trade Agreement (NAFTA) and the European Union (Figure 2).

Good news for member countries, particularly non-ASEAN

RCEP deepens trade and investment relations between member countries mainly through reductions in non-tariff barriers (NTBs) on goods and services trade. The agreement focuses on NTBs as import tariffs were already relatively low among RCEP members. (Low import tariffs are the result of the global trend of unilateral tariff liberalization over the past decades and a web of existing trade agreements among RCEP members, such as the ASEAN-China FTA, ASEAN-Australia-New Zealand FTA, China-Australia FTA and Japan-Korea FTA.) It harmonizes the provisions imposed by countries on the trade in goods, providing more certainty for traders and investors. For example, it encourages importing countries to accept the product standards of other member countries from where the good originates if those countries provide the same level of consumer protection. As its perhaps most important feature, the agreement aligns rules of origin for all 15 countries, facilitating the integration of RCEP participants into the same production chain. This may help RCEP members attract a larger share of global value chains (GVCs) and deepen their specialization, which may be particularly important at a time when the U.S.-China trade dispute has accelerated the reconfiguration of GVCs in and out of China. RCEP covers relevant provisions in services too, including commitments by each member not to discriminate vis-à-vis other members’ investors in several service sectors. Finally, it facilitates the temporary movement of persons for investment and trade activities.

RCEP is expected to benefit its members while the gains for the rest of the world would be limited. The reduction in trade and investment barriers would increase the economic integration among RCEP member countries allowing for significant gains from trade. Recent modeling work suggests that by 2030 the agreement would increase the GDP of the trading bloc by 0.4 percent (equivalent to $170 billion), with a 0.3 percent increase for China and 0.2 percent for ASEAN members (Figure 3). The gains for member countries drive the expected mild positive effect of RCEP on the world economy (0.1 percent of GDP), although the benefits for nonmembers are likely negligible.

ASEAN countries stand to benefit less from RCEP than from other (deeper) trade agreements. ASEAN economies are set to gain the smallest benefits among RCEP signatories as they have the least scope to reduce the barriers with other members given the existing web of trade agreements. This is part of the reason why economies like Vietnam and Malaysia are expected to gain more from the recently signed Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) than from the RCEP. This is consistent with recent World Bank analysis, which suggests that the EU-Indonesia Comprehensive Economic Partnership Agreement would yield considerably larger economic benefits to Indonesia than RCEP would. These agreements are also more ambitious in scope than RCEP. For instance, unlike RCEP both CPTPP and the EU-Indonesia CEPA have provisions on Investment-State Dispute Settlement and on rules governing State Owned Enterprises.

No substitute for multilateralism

While welcome, plurilateral agreements like RCEP cannot replace an effective multilateral trading system, which remains in urgent need of reviving. RCEP and other bilateral and plurilateral agreements have proliferated given the lack of progress of the multilateral trading system in furthering global trade integration over the past two decades. However, such agreements cannot be a substitute for multilateralism. That is particularly the case for developing countries that have greatly benefited from the rules-based trade system through guarantees against trade discrimination, incentives to reform, and market access around the globe. An effective multilateral trade system remains the best tool to help resolve harmful trade disputes, such as the one ongoing between the United States and China, and to help avert future disputes.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The significance of the Regional Economic Partnership Agreement

November 20, 2020