Earlier this month, the African Economic Research Consortium held its 50th Biannual Plenary and Workshop in Cape Town. The topic was Growing with Debt in African Economies, and the discussions were energetic and educational. We presented a paper at the plenary, a preliminary version of which can be found here.

Our main points are that public debt dynamics in many countries in sub-Saharan Africa are now working against their stability and growth and, indeed, that of the subcontinent, but the story does not have to end in tears. We come to this conclusion by asking three questions: Has there been an increase in the capacity of African economies to bear higher levels of debt? Do markets and governments in emerging Africa have enough information about each other to make good decisions if there is a debt crisis? And, should we be confident that debt distress in Africa will be resolved in an orderly manner?

Our answer to each of these questions is no. This blog explains why; a companion blog will propose remedies.

1. Have African countries been getting more debt because they have improved policies and institutions over the last 10 years, or only because debt relief wiped their slates clean?

To figure this out, we looked at levels and trends in public debt, economic growth and poverty, and changes in the quality of policies and institutions for about 45 countries. The idea was to figure out whether debt has helped increase welfare, and whether countries have been borrowing more on the markets because their policies and public institutions are better. The public debt numbers are from country sources, the income and poverty numbers from the usual multilateral development institutions, and the data on the quality of country policies and institutions from the World Bank Country Policy and Institutional Assessments (CPIA) between 2007 and 2018.

We found that the quality of policies and institutions has deteriorated or not improved in most countries. The biggest deterioration is in countries that had the highest increases in public debt.

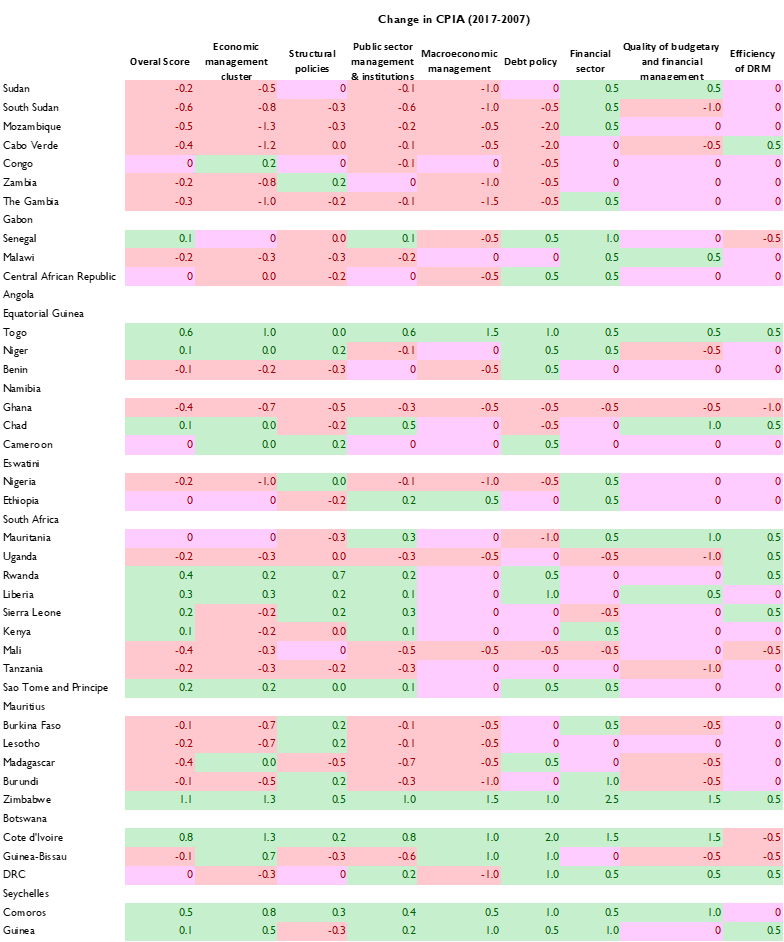

Naturally, not all policies matter equally. So, for example, a country might have worse environmental and social policies, but better macroeconomics, financial sector and trade policies, and budgetary and tax systems. That’s not hard to figure out. Table 1—which ranks countries by the extent of the increase in their public debt-to-GDP ratios during the last decade—shows the most relevant subcategories of the CPIA for all countries: macro management and debt policy, financial sector, quality of budgetary and financial management, and efficiency of domestic resource mobilization. It says three things:

Table 1: Change in quality of policies and institutions, 2007-2017

Source: Devarajan, Gill and Karakülah (2019) based on World Bank reports. Note: Red is bad, green is good.

- There are more red and pink cells than green, and the pattern gets worse as you go from countries that had moderate increases in debt to those at the top of the table.

- There are only a few countries that have had across-the-board increases in the quality of policies and institutions since 2007. They are Togo, Cote d’Ivoire, and Zimbabwe.

- The weakest areas are domestic resource mobilization, macro policies, and quality of budgetary and financial management. The only bright spot is a general improvement in financial sector policies, except in Ghana, Uganda, Mali, and Sierra Leone.

Bottom line: The World Bank’s take on the quality of policies and institutions in sub-Saharan Africa is that it has not improved since debt relief. So it is surprising that the Bank has largely been silent about African debt. It should pay more attention to its own assessments.

2. Will debt markets get to know Africa well enough to respond well when the next crisis comes?

During the Latin American debt crisis in the 1980s, there was a syndrome that came to be known as “Buenos Aires is the capital of Brazil.” If something went wrong in Argentina, investors in New York would pull out of Brazil, and so on.

The same contagion will likely afflict emerging markets in Africa. One sign is that sovereign bond spreads are clustered between 400 and 500 basis points for African economies accessing market, except South Africa. That is to be expected in a frontier region. But the main reason for expecting contagion is that the main provider of information about these economies is seriously unreliable.

In emerging markets people pay a lot of attention to what the International Monetary Fund (IMF) says and does, especially what it says about a country’s growth prospects and whether it plans to backstop a country’s economy with a program. Look at what the IMF has been doing. It has signed arrangements with 16 countries since oil prices crashed in 2014. Look also at what the Fund has been saying, especially the gap between what will happen to debt and growth in countries that are borrowing from the IMF, compared with those that are not. Table 2 summarizes the findings:

- IMF program countries are expected to reduce debt-to-GDP ratios by almost 10 percentage points between 2017 and 2024, non-program countries less than 1 percentage point.

- Program countries are projected to grow by an average of 5.2 percent annually, non-program countries by 3.7 percent. 1.5 percentage points can make the difference between sustainability and distress.

- As a reality check, we took a look also at the actual growth rates of these groups. During the high growth period of 2010 to 2015, both groups grew by 4 percent annually. IMF program countries are now expected to outperform themselves.

We cannot reasonably expect the IMF to be accurate in its projections; forecasting is a tricky business. But we should expect it to be unbiased. Instead, it seems to be supplying the market systematically bad numbers. For a region that is depending more and more on markets, this cannot be good.

Table 2: Summary of IMF projections to 2024, public debt and GDP growth

Source: Devarajan, Gill and Karakülah (2019), using IMF data. All numbers are IMF projections except the last column.

Bottom line: African researchers should be subjecting the Fund’s analysis to a lot more scrutiny. Both the growth forecasts and—what is the same thing—debt sustainability assessments of the IMF and World Bank should be treated with skepticism.

3. In countries that become distressed, will debt resolutions be reasonably orderly?

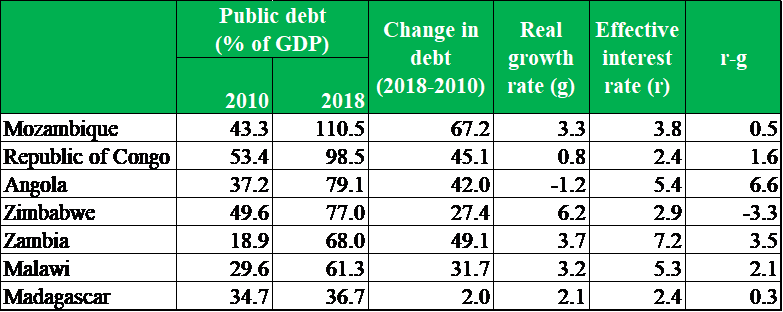

To figure this out, it seemed sensible to look at what is happening in countries that are already in crisis. We looked closely at a group of countries in what we call the belt of distress—a group of seven countries just north of South Africa. They include Madagascar, Mozambique, Zambia, Malawi, Zimbabwe, Angola, and the Republic of Congo.

Following an earlier paper that two of us have written (summarized here) we used three measures of debt sustainability—the latest debt to GDP ratios, change in this ratio over the last 9-10 years, and the difference between the rate of interest and the rate of growth during the last five years. Other than Madagascar, things look pretty bad; Zimbabwe’s national accounts are being redone, so expect its growth rate to change (Table 3).

Table 3: Debt indices in Africa’s ‘Belt of Distress’

Source: Devarajan, Gill and Karakülah (2019), using IMF data, and Ministry of Finances, Central Banks and National Statistics Offices of the countries in the table.

Contrary to common belief about this round of debt increases, a sizable part of the public debt is external; more than half usually. But, again contrary to popular perceptions, not a lot of it is owed to China (except in the Republic of Congo). The rise in external debt has been mainly because of big devaluations, in the neighborhood of 50 percent for oil-exporters like Angola. All have been running primary deficits for a long time and adding to their debt.

If you think of the three main risks as China, currency, and corruption, the serious ones involve currency and corruption. All these countries have had big devaluations (all except the Republic of Congo, which does seem to have a China problem). And all have had a worsening of corruption. There are stories of bribes being taken to provide guarantees, of hiding debt, and of undisclosed terms with lenders from China and other countries.

Bottom line: Nothing in the way that currently distressed governments have been handling their problems provides confidence that debt resolutions will be orderly. If this continues and—as we expect—soon includes Africa’s bigger economies, it could be a real mess.

For another look at Africa’s rising debt and policies to address it, see the recent Brookings Africa Growth Initiative report, Is sub-Saharan Africa facing another systemic sovereign debt crisis?

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Stressful speculations about public debt in Africa

June 19, 2019