Once thought to be sporadic and only affecting faraway places, the profile and timetable of climate change have changed dramatically to be on the calendar of every country. Take the forecast that sea levels along the U.S. coastline will rise by a foot over the next 30 years—as much as the increase in the previous 100 years—wreaking havoc in low-lying regions. Faced with such trajectories, it will no longer be enough to cope and build back after disasters, but governments, businesses, and individuals need to anticipate and “build forward”—the central message of “Risk and Resilience in the Era of Climate Change,” published on April 4.

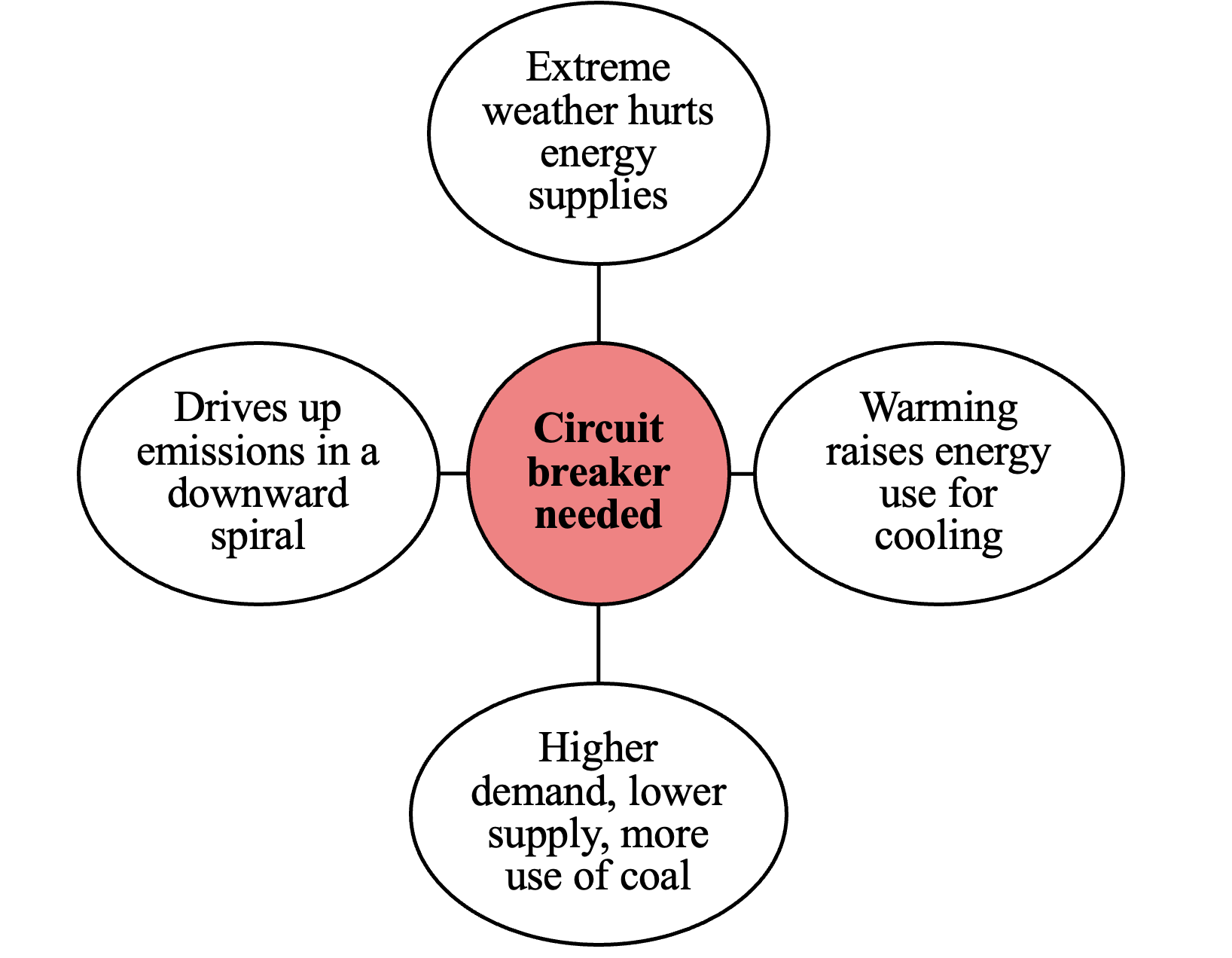

That the climate danger no longer lies over the horizon is vividly shown by extreme weather aggravated by climate change already destabilizing energy supplies and creating shortages (Figure 1). This, coupled with the demand for more cooling during unseasonably hot summers, is stoking energy insecurity, prompting even greater fossil fuel use—as Europe and South Asia have seen in recent months—driving up effluents and worsening the climate crisis. If this continues, “circuit breakers,” such as a cross-country moratorium on new oil, gas, and coal projects will be needed—and accompanied by a very aggressive push for renewable sources—to avert a full-blown climate catastrophe.

Figure 1. Climate, energy and a downward spiral

Source: Author

Precious decades have already been lost to decarbonize to a level that will avert catastrophic climate change. Now, nothing short of transformational change is needed to alter the pattern of economic growth to a more environmentally sustainable one. That includes mainstream economic policy—and the theories that go with it—to abandon the obsession with short-term gross domestic product (GDP) growth. The targeting of this at all costs led to a mentality in which any type of growth, including an ecologically destructive pattern, is deemed good. A point in case is the East Asian “miracle” during 1970-90.

The focus must shift to truer measures of growth that deduct the spillover harm from carbon-polluting industries and environmental and ecological degradation from the growth process. Ranking countries based on measures that net out this damage will help emphasize the quality of economic growth and encourage more sustainable patterns of investment.

Far-reaching change will occur only with clear accountability being assigned to the sources of the climate conundrum. It is vital to attribute climate change squarely to the relentless emissions of GHGs from using fossil fuels. Equally, it is key to communicate this link to the public and policymakers precisely when climate disasters strike. The public everywhere increasingly identifies climate change as a top global risk, but nowhere does it flag climate change as the highest priority for domestic investment, which must increase in the era of climate change.

Policymakers will need to use the economists’ toolkit to alter the trajectory of climate change. The economics of spillover harm or negative externalities, usually a section in economics textbooks, needs to become a staple of growth economics. Making it so would signal the merits of decarbonizing economies. It would, for example, motivate the use of carbon pricing via a carbon tax levied on the source of pollution—as South Korea and Singapore have done, or through carbon trading—as the European Union and China are doing.

The economics of spillover harm has wide-ranging implications for development projects. All projects must pass a test of resilience to climate change and be accompanied by legal covenants on mitigation and adaptation. Development programs should avoid the use of fossil fuels, in addition to doing away with subsidies for this pollution source. High-income countries should provide vast climate financing to low-income countries, following the minimal progress achieved on this at COP27. Climate financing would be helped if the world’s multilateral development banks were to strike an alliance on climate action—particularly those with new climate agendas, such as the International Monetary Fund, the World Bank, the Asian Development Bank, and the New Development Bank.

Global dangers from pandemics to geopolitical conflicts to global warming, when taken together, paint a picture of low-probability but high-impact risks (the so-called “black swans”) becoming high-probability and high-impact ones (“gray rhinos”). Accordingly, building resilience needs to go beyond simply coping with disasters to preventing them. Innovative approaches to resilience, such as pooling resources across boundaries and getting financing approvals ahead of disasters, are needed as countries face severe shortages of trained staff and financial resources to cope with risk and resilience challenges.

The need is greater than ever for regional and global cooperation in generating climate finance and scaling up investments in climate mitigation and adaptation, much as exhibited during COVID-19. That vast sums can be quickly mobilized to fix global problems, if public opinion is supportive, was dazzlingly demonstrated in the trillions of dollars—$ 15 trillion, by one estimate, in stimulus spending in 2020 to fight COVID-19. In the wake of the existential challenge from runaway climate change, the same political resolve and public support are called for.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Risk and resilience in the era of climate change

April 4, 2023