Investment in emerging market and developing economies (EMDEs) is projected to grow at a pace below the average rate of the past two decades through the medium term, after declining in the majority of countries during the pandemic. This outlook for investment is unwelcome news on several counts. Whether the policy priority is bolstering resilience to climate change, improving social conditions, smoothing the transition away from growth driven by natural resources, or supporting long-term per capita income growth, investment (gross fixed capital formation, or buildings, machinery, equipment, and intangible assets used for more than one year) is critical.

Broad-based investment contraction during the pandemic

As business operations were disrupted and uncertainty spiked in 2020, aggregate investment in EMDEs shrank by 1.5 percent. This was a substantially worse performance than during the previous global recession, in 2009, despite easier financial conditions and the provision of sizeable fiscal stimulus in many large EMDEs during the pandemic.

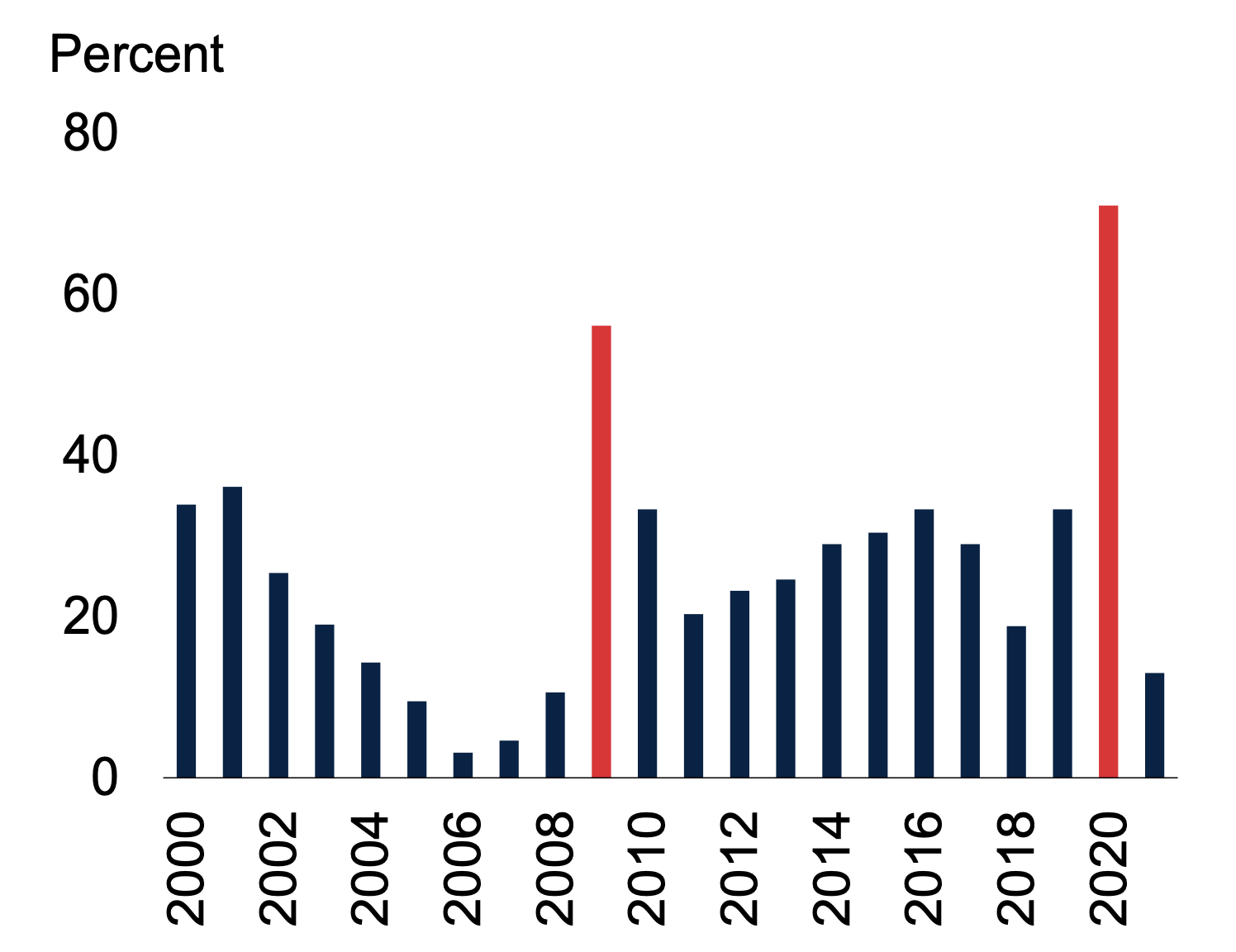

Excluding China, EMDEs suffered a far deeper investment decline in 2020, of more than 8 percent, also a worse performance than in 2009. A key difference in the experience of 2009 versus 2020 was the number of affected EMDEs. Investment contracted in about 70 percent of EMDEs in 2020, compared to 55 percent in 2009 (Figure 1).

Figure 1. Share of EMDEs with an investment contraction

Sources: Haver Analytics; World Bank; World Development Indicators.

Note: Investment refers to gross fixed capital formation.

A subdued investment recovery

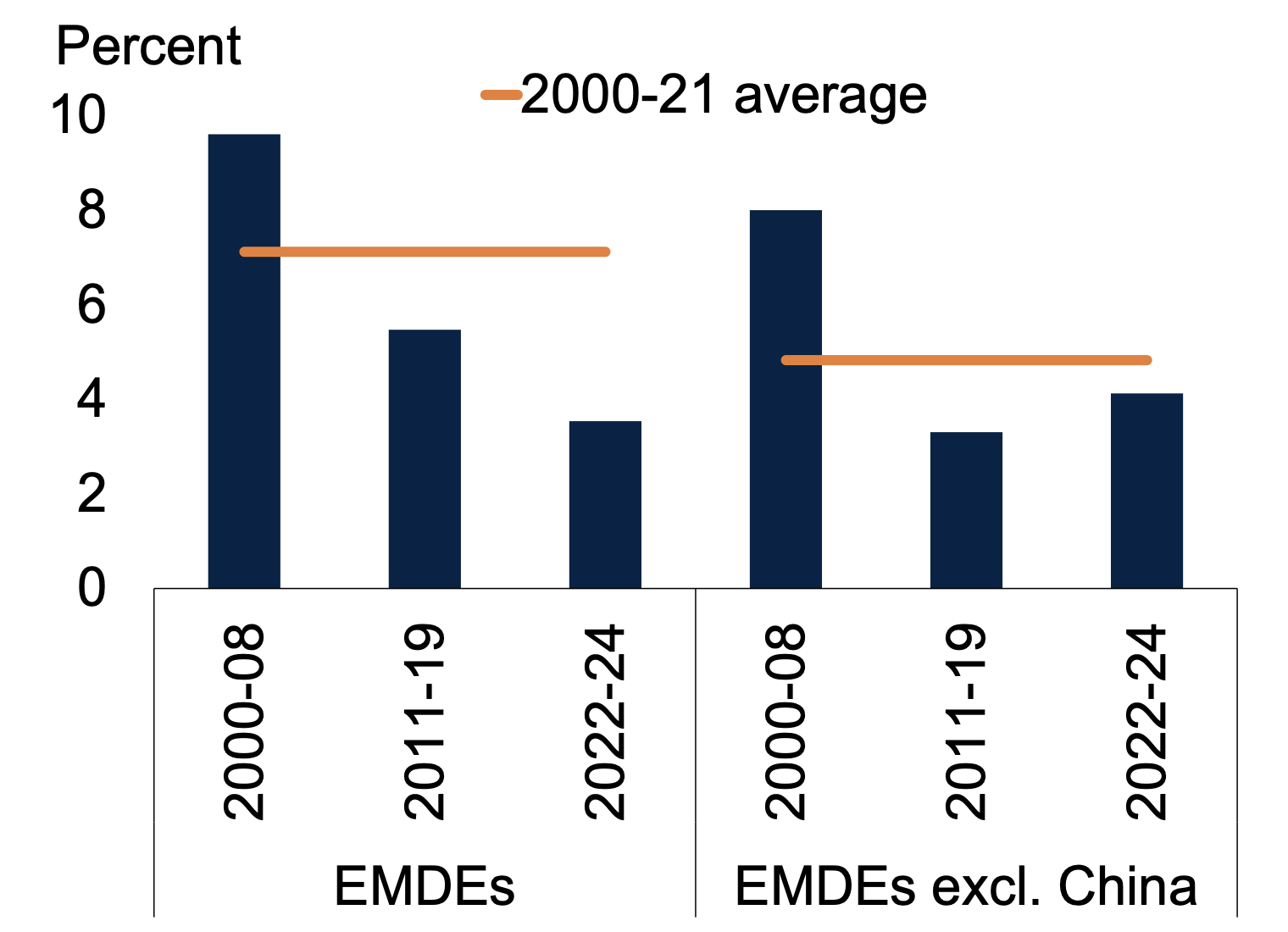

Investment growth is projected to average 3.5 percent per year in EMDEs during 2022-23, and 4.1 percent in EMDEs excluding China. These projected investment growth rates are below the long-term (2000-21) average. Moreover, the subdued outlook follows not only a sharp decline during the pandemic, but also a prolonged investment growth slowdown during the 2010s as China shifted away from investment- and trade-led growth, commodity-exporting EMDEs suffered a sharp mid-decade decline in oil and metals prices, and the effects of weak economic growth and post-global financial crisis deleveraging generated spillovers to EMDEs (Figure 2).

Figure 2. Investment growth

Sources: Haver Analytics; World Bank; World Development Indicators.

Note: Investment refers to gross fixed capital formation. Investment growth is calculated with countries’ real annual investment in constant U.S. dollars as weights. Years of global recessions and one year after (2009-10 and 2020-21) are removed from averages shown in the bars. Sample includes 69 EMDEs.

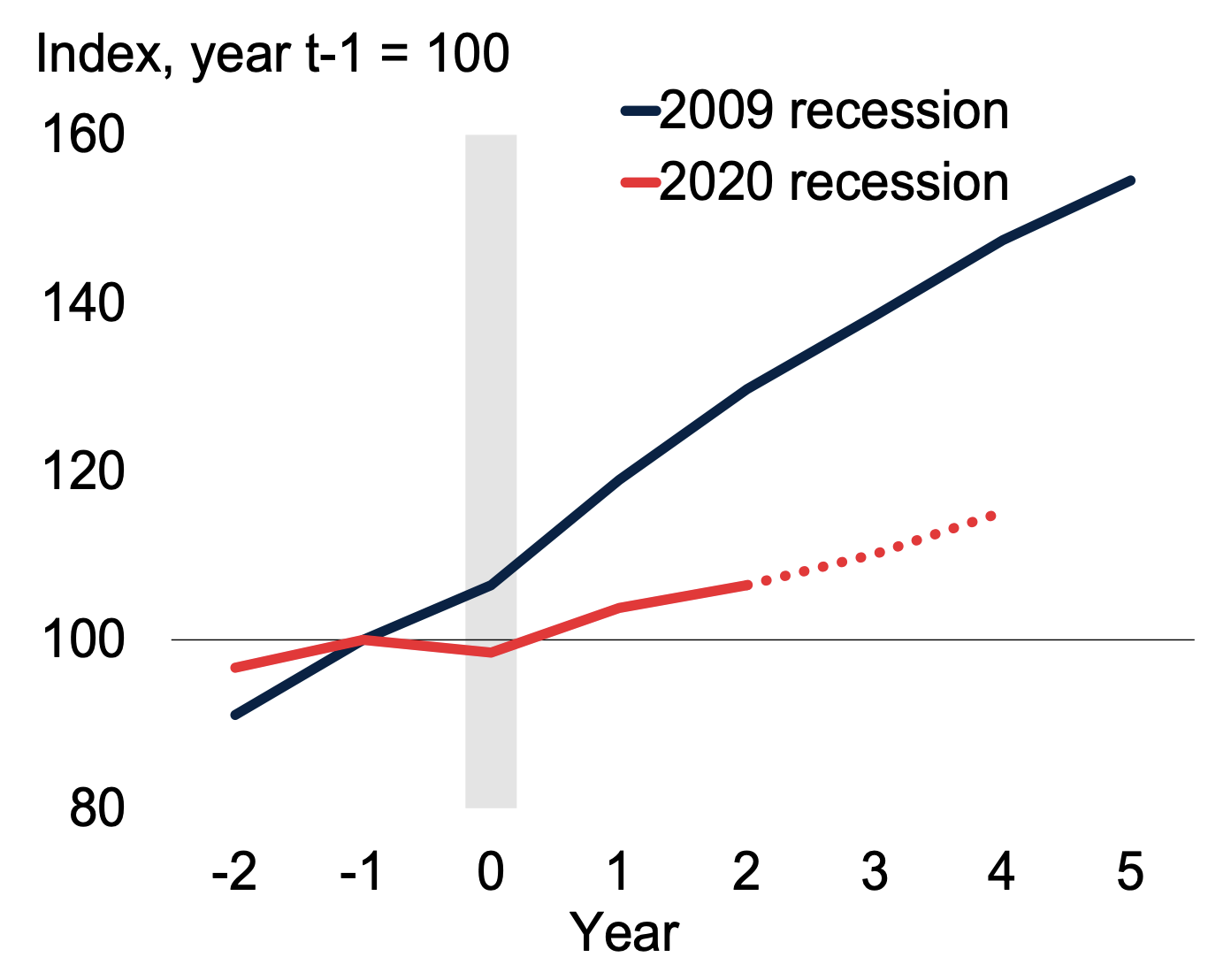

Further, the investment recovery in EMDEs following the pandemic is proceeding much more slowly than the recovery following the global financial crisis. By 2024, four years after the 2020 recession, the level of investment in EMDEs is projected to be about 15 percent above the pre-pandemic (2019) level. By comparison, four years after the 2009 recession, investment in EMDEs was already nearly 50 percent above the pre-recession level (Figure 3).

Figure 3. Investment level in EMDEs

Sources: Haver Analytics; World Bank; World Development Indicators.

Note: Investment refers to gross fixed capital formation. On the x-axis, year zero refers to the year of global recessions in 2009 and 2020. Dotted portion of the 2020 line is a forecast. Sample includes 69 EMDEs.

Large investment needs

The weak investment recovery from the 2020 global recession is particularly concerning because EMDEs’ investment needs are substantial. Building resilience to climate change and putting countries on track to reduce emissions by 70 percent compared to current levels, for instance, is estimated to require an additional investment of 1 to 10 percent of GDP annually between 2022 and 2030 in EMDEs, with higher investment needed in low-income countries. To achieve the infrastructure-related Sustainable Development Goals, EMDEs would need to invest 4.5 to 8.2 percent of GDP annually during 2015-30, depending on policy choices and infrastructure service quality. Most of this amount would go to transport and electricity.

The benefit of policy reform

A challenging global financing environment and constrained fiscal space will make boosting investment in EMDEs challenging. Yet a comprehensive set of fiscal and structural policies, tailored to country circumstances, can help.

Spending on public investment can be boosted by reallocating expenditures toward growth-enhancing investment, improving public spending efficiency, or better mobilizing domestic resources. Private sector participation in filling investment needs is crucial in most EMDEs, but attracting such investment requires a sufficient regulatory and operating environment.

Setting appropriate and predictable rules relating to investment decisions and encouraging firm formalization can promote investment. Simplification of border procedures and elimination of unnecessary duties can increase trade flows, with associated benefits for investment. Development of digital infrastructure and capabilities and modernizing infrastructure to withstand climate change, two priority areas for many EMDEs, can be advanced with private sector involvement.

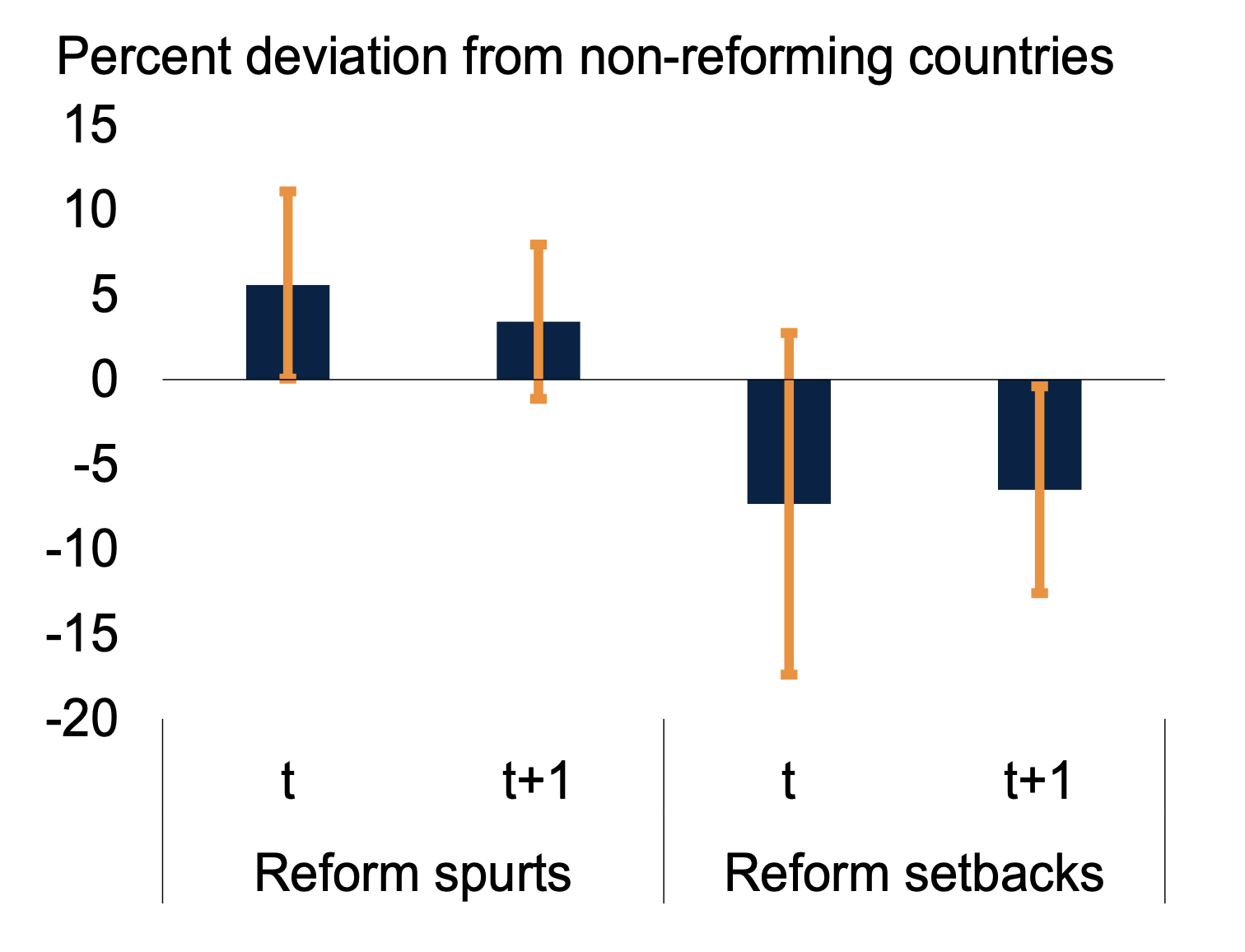

Figure 4. Investment growth in EMDEs around reforms

Source: PRS Group International Country Risk Guide (ICRG); World Bank.

Note: Investment reform events are derived from the ICRG “investment profile,” which includes three subcomponents: contract viability/expropriation, profit repatriation, and payment delays. Bars show the increase in investment growth around a reform spurt or setback at t=0 relative to the countries not experiencing a reform spurt or setback. Vertical lines show the 95 percent confidence interval.

Over the past four decades, countries with investment policy reform spurts have been found to be associated with significantly higher investment growth—by about 6 percentage points, on average—relative to non-reforming countries during the same year, while reform setbacks are associated with about 7 percentage points lower investment growth (Figure 4). Reforms do make a difference.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Investment in emerging and developing economies: Reversion to trend is not enough

February 22, 2023