Sovereign domestic debt restructurings (DDRs) have become more common in recent years and touched upon a growing share of total public debt. This, however, should not come as a surprise. While the market for international (i.e., foreign law) sovereign debt securities has a volume of roughly $1 trillion, the total outstanding amount of domestic securities is about 40 times as large. In Emerging markets and developing economies, where debt restructuring is likelier to happen, the share of domestic debt in total debt has risen from 31 to 46 percent from 2000 to 2020. During 1990–2020, there were roughly as many DDRs (30 episodes) as stand-alone external debt restructurings (EDRs) (27 episodes).

Domestic restructurings possess a distinct feature that separates them from external debt restructurings. This feature—in essence a negative externality—is that domestic restructurings impose direct costs on the local financial system, potentially reducing the (fiscal) savings for the sovereign from the debt exchange. These costs are due to the existence of a typically strong nexus between sovereign and financial institutions (especially banks), which during episodes of sovereign stress could impact the balance sheet (both asset and liability side) and income of those institutions. When internalized, this externality will result in a smaller debt relief accrued to the sovereign and, ceteris paribus, make it less likely for a domestic restructuring (relative to an external debt restructuring) to take place.

Although its degree varies across countries, the captive nature of domestic investor base affords sovereign authorities leverage over domestic investors and may have made the holdout problem less of an issue in DDR cases in recent years. Similarly, DDRs differ from EDRs in the ability of the government to restructure domestic debt by retroactively changing the legal terms of bond contracts. Greece (2012) and Barbados (2018) have used this “local law advantage” and introduced collective action clauses in their domestic law contracts prior to restructuring their domestic debt.

Domestic debt restructuring Laffer Curve

Interestingly, if recapitalization and financial stability costs of a DDR are an increasing function of haircut imposed on creditors, there is a maximum value of haircut beyond which the gross relief obtained by the sovereign from increasing the haircut are outweighed by recapitalization and financial stability costs, rendering the marginal net debt relief negative.

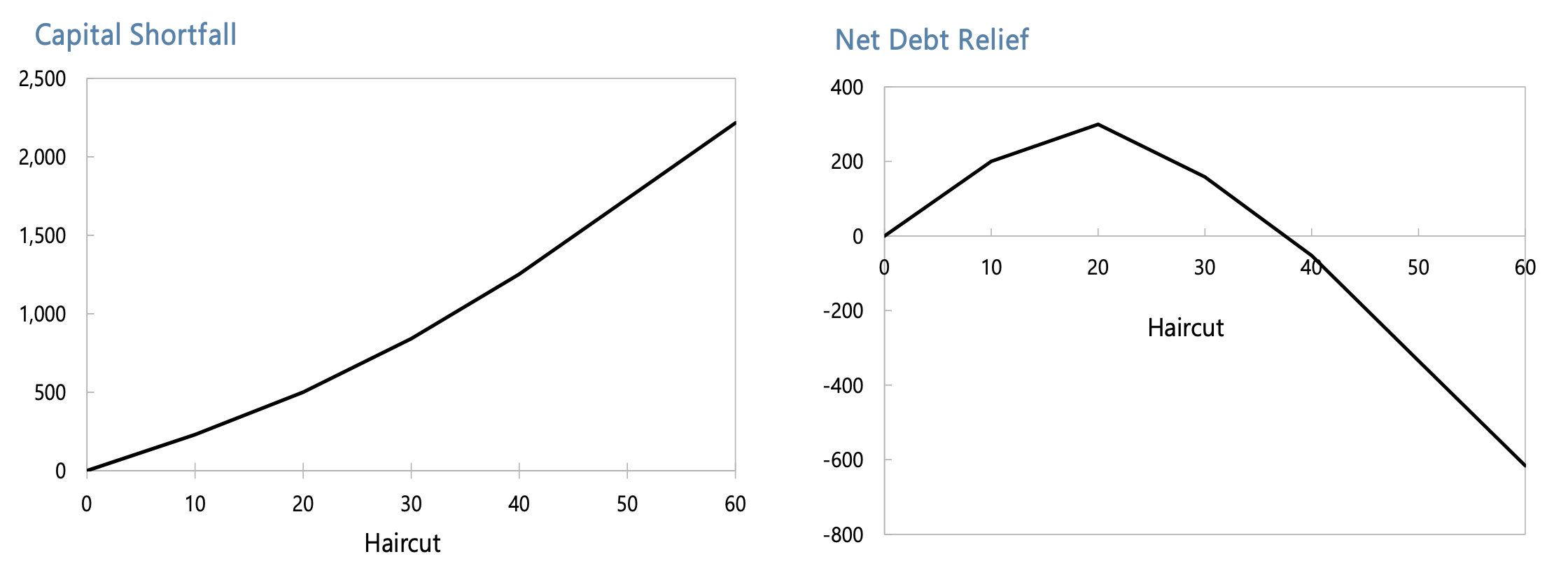

Figure 1 below depicts an outcome of stylized calculations of net debt relief (NDR) accrued to a sovereign under a variety of restructuring scenarios. Bank’s asset side can erode—directly and indirectly—with haircut because the higher the haircut required to establish debt sustainability, the more severe are the prevailing conditions faced (also) by the private sector (impacting its ability to pay), thus rendering bank loans more risky and therefore worth less. Banks may also face deposit withdrawals (increasing in intensity with economic/fiscal shock), potentially forcing them to liquidate some assets at fire-sale prices, further strengthening the (positive) correlation between haircut and bank’s asset impairment.

Figure 1. Capital shortfall and net debt relief as a function of haircut

Source: Author’s simulations.

The right panel is in essence the DDR Laffer Curve (hereafter RLC). It shows that net debt relief accrued to the sovereign increases with haircut for values of haircut below 20 percent, declines beyond 20 percent haircut, and even becomes negative (for values of haircut just below 40 percent). In this stylized example, the sovereign should not impose a haircut above 20 percent, since going beyond this threshold will reduce the NDR accrued to the sovereign (potentially even making it negative) while likely subjecting the financial sector to higher financial stability risks and imposing increasing costs to it (beyond what can be captured in ex ante calculations of the capital shortfall).

The shape of RLC may differ depending inter alia on the regulatory treatment of impaired assets as well as the structure of liabilities. For example, relaxing the assumption of zero risk weight on government securities and instead adopting weights for distressed sovereign exposures would pivot the RLC downward. On the liabilities’ side, the availability of “bail-in-able” deposits may reduce the need for public intervention (e.g., Cyprus, 2013) and thus shift the RLC upwards.

Safeguarding financing stability and recapitalizing financial institutions

The impact of a DDR on bank balance sheets (and ability to provide credit to the economy) could be significant where sovereign securities comprise a large share of bank assets. Any loss in value of government debt exposures will lead to capital losses in financial institutions at the time of the restructuring unless these have already been absorbed by loan-loss provisioning and mark-to-market accounting prior to the restructuring. Such reduction in the value of government debt portfolio could be due to any changes to the original contractual value of the debt security, such as, face-value haircut, coupon reduction, and maturity extension (with below-market coupon rates).

When banks are able to absorb losses without having to resort to a recapitalization using public funding, debt relief sought from other creditors and/or fiscal consolidation required to restore debt sustainability would be smaller. This will also reduce the probability of a financial crisis being triggered by the debt restructuring. This becomes important because debt restructurings accompanied by banking crises are typically associated with larger economic output losses. Therefore, during the design stage of a DDR, measures should be taken to safeguard financial stability and avoid financial-sector stress developing into a full-blown crisis. This can be done by both strengthening contingency planning and crisis management capabilities but also by recapitalizing affected institutions.

It should be noted that the design of the restructuring may have implications for financial stability and immediate recapitalization needs (and therefore for NDR). Specifically, restructurings involving coupon reduction or maturity extension are likely to have less of a direct impact on domestic financial institutions’ balance sheet than exchanges involving face-value haircuts.

Recognition of losses need to be followed by a strategy to restore capital buffers if those losses produce shortfalls in regulatory bank capital. If the strategy ends up requiring public funding for recapitalization, policymakers should be aware of the downsides associated with bailouts (e.g., moral hazard, etc.) and minimize them to the extent possible.

Finally, special care should be given to central banks’ holdings of domestic sovereign debt to ensure its normal operations, including the conduct of monetary policy and the payments system.

Disclaimer: This blog is based on a recent research paper entitled “Restructuring Domestic Sovereign Debt: An Analytical Illustration.” As this research represents work in progress, any comments are welcome. The intention is to encourage debate on domestic sovereign debt restructuring issues and broaden the research agenda in this area. The views in this blog are those of the author and should not be attributed to the IMF, its Executive Board, or its management.

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Restructuring domestic sovereign debt: Fiscal savings and financial stability considerations

February 13, 2023