| Growth and inflation have unexpectedly helped lower government debt-to-GDP ratios in many countries since early 2021. However, government debt is still elevated and fragile in its composition, and the magic of growth and inflation is unlikely to last long. To reduce debt in a lasting manner, growth-boosting reforms and, in some countries, debt relief are needed. |

During the 2020 global recession, government debt rose to multi-decade highs, marking the largest jump in five decades. Since early 2021, some of this government debt surge has been unwound, as the latest update of the World Bank’s Cross Country Database of Fiscal Space suggests. The decline in debt has in part reflected the impact of strong growth and elevated inflation of the past two years.

Stronger growth and higher inflation in 2021-22

2021 brought a record-strong global growth rebound from the collapse in activity in 2020. Global and advanced-economy growth in 2021 reached 25-year highs of 5.9 percent and 5.3 percent, respectively. In 2022, however, widespread and rapid monetary policy tightening and the impact of the Russian Federation’s invasion of Ukraine on commodity markets weighed heavily on the global economy. Global growth decelerated sharply by 3 percentage points to 2.9 percent in 2022.

The recovery lagged somewhat in emerging market and development economies (EMDEs) but, even in EMDEs, growth at 6.7 percent in 2021 was almost one-half above its 2000-2019 average. Like in advanced economies, growth in EMDEs also slowed sharply in 2022 but was still above its 2000-19 average in more than one-third of EMDEs. Major exceptions were China, where COVID-related measures hindered growth, and Russia and Ukraine, where the war severely disrupted activity.

Since its pandemic trough in May 2020, global inflation has risen sharply. By December 2021, global inflation had increased to 5.6 percent from 1.2 percent in May 2020 before reaching a 27-year high of 9.6 percent in October 2022. Since then, it has eased somewhat (to 9.1 percent in December 2022), but inflation is now running above target in all inflation targeting advanced economies and EMDEs.

Surprise, surprise: Debt is coming down

Government debt declined between 2020 and 2022 in nearly 65 percent of countries, including more than 70 percent of advanced economies and 60 percent of EMDEs. In advanced economies as a whole, government debt declined to 112 percent of GDP from a five-decade high of 125 percent of GDP in 2020. Among EMDEs, declines in debt in the majority of EMDEs were offset by large increases in some large EMDEs. As a result, among EMDEs as a whole, government debt remained broadly steady at 64 percent of GDP in 2022.

Strong growth and high inflation have played key roles in reducing debt-to-GDP ratios since 2020. Rapid growth and high inflation improve nominal incomes that are subject to taxation. For a given nominal government debt stock, the government of a faster-growing and higher-inflation economy is therefore in a better position to raise the revenues needed to honor obligations: It has a larger “debt-carrying capacity.” This is captured in a falling government debt-to-GDP ratio when growth and inflation are high.

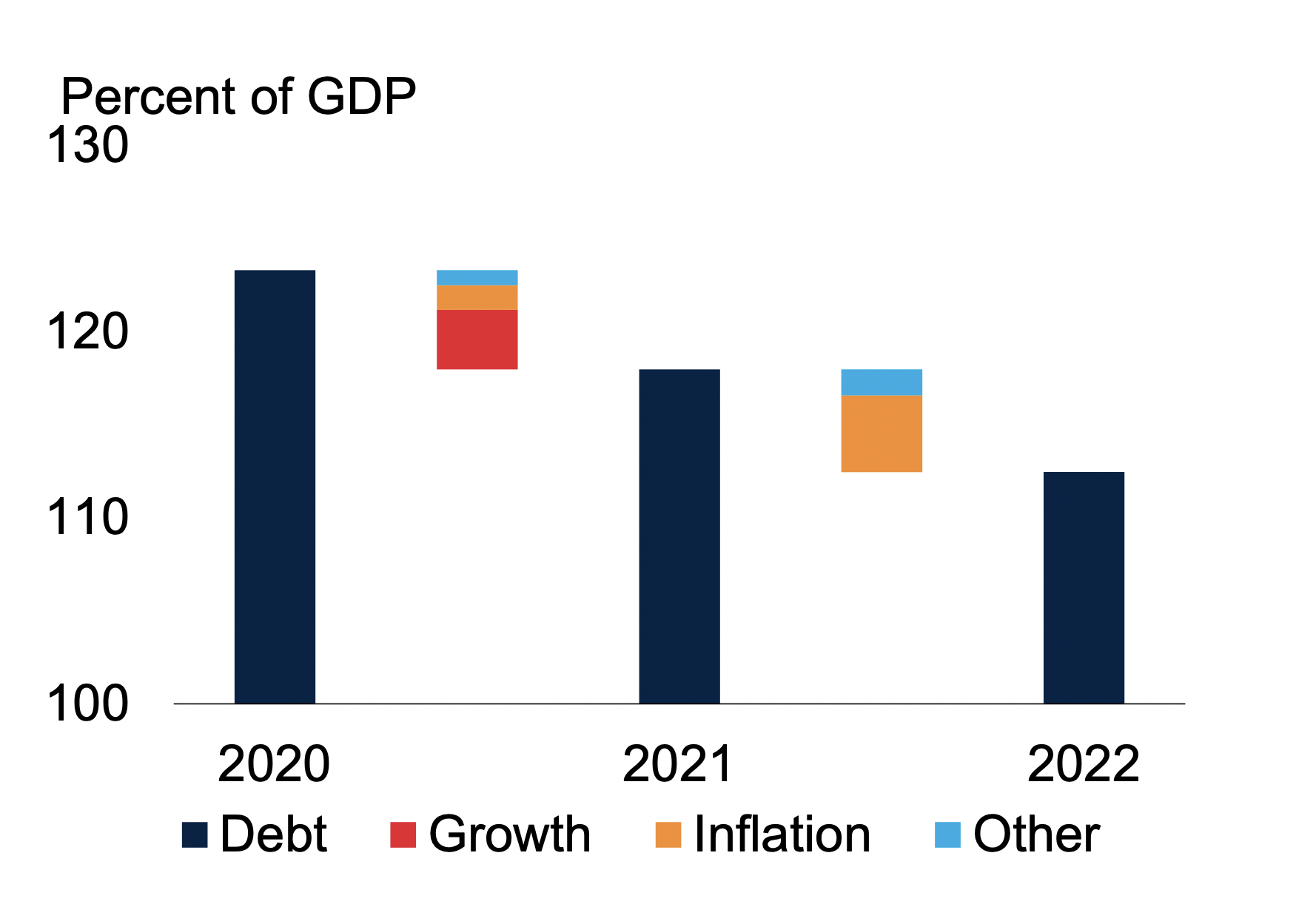

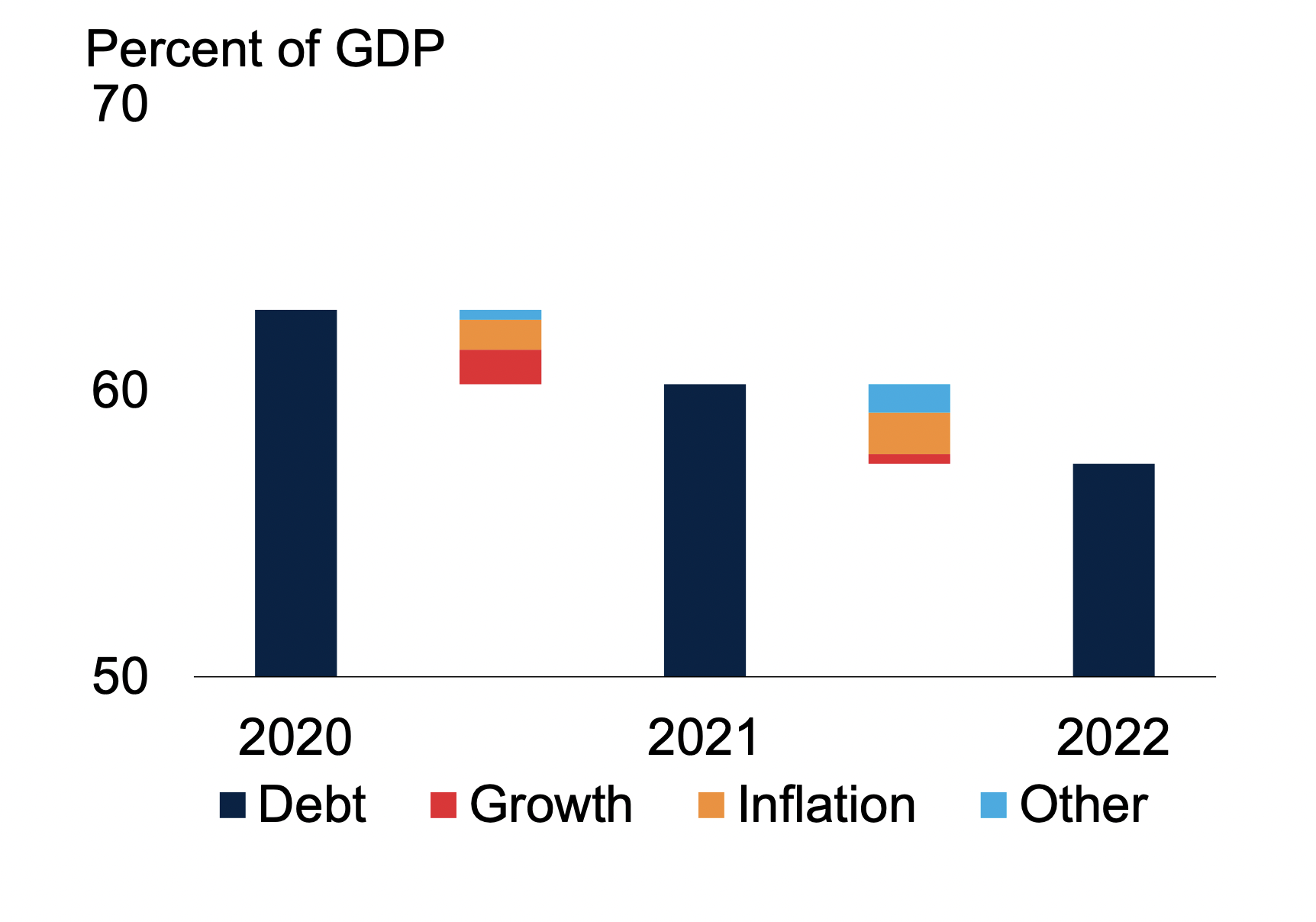

A simple accounting decomposition illustrates this impact of growth and inflation on debt. In this decomposition, two counterfactual debt-to-GDP ratios are calculated for each country: One assuming its average nominal GDP growth over 2010-19 and a second one assuming average 2010-19 real GDP growth. These counterfactuals are compared with the actual path of the debt-to-GDP ratio. The difference between the actual debt-to-GDP ratio and the second counterfactual ratio (with average 2010-19 real GDP growth) is attributed to above-average growth; the difference between the two counterfactual ratios to inflation.

This exercise suggests that, in 2021, above-average growth shaved at least 3 percentage points of GDP off advanced-economy debt (Figure 1A). In EMDEs other than China, Russia, and Ukraine, it shaved at least 1 percentage point of GDP off debt (Figure 1B). In that year, when inflation was just beginning to accelerate, above-average inflation reduced debt-to-GDP ratios by just over 1 percentage point in advanced economies and around 1 percentage point in EMDEs.

Figure 1. Contributions to government debt reduction

| A. Advanced economies | B. EMDEs excluding China, Russia, and Ukraine |

|

|

Source: Kose, Kurlat, Ohnsorge, and Sugawara (2022).

Note: The contribution of growth is defined as the difference between the change in the government debt-to-GDP ratio assuming real GDP growth had been its country-specific 2010-19 average and the actual change in the government debt-to-GDP ratio. The contribution of inflation is defined as the difference between the change in the government debt-to-GDP ratio assuming nominal GDP growth had grown at its country-specific 2010-19 average and the change in the government debt-to-GDP ratio assuming real GDP growth has been its country-specific 2010-19 average. “Other” includes factors such as fiscal consolidation and valuation changes. U.S. GDP dollar-weighted averages.

In 2022, however, as inflation soared and growth stalled, above-average inflation shaved at least 4 percentage points off government debt in advanced economies and over 1 percentage point in EMDEs. In contrast, the impact of above-average growth was negligible in advanced economies as well as EMDEs.

Over the two-year period from 2020 to 2022, inflation therefore reduced the debt-to-GDP ratio for advanced economies by almost 6 percentage points of GDP, while economic growth had about half the impact. For EMDEs excluding China, Russia, and Ukraine, above-average inflation and growth lowered debt-to-GDP ratios by more than 4 percentage points—almost 3 percentage points of GDP due to inflation and more than 1 percentage point of GDP due to growth.

This exercise assumes that the nominal stock of government debt is unchanged across scenarios. In practice, however, higher growth and inflation also helped raise revenues and narrow fiscal deficits, thus reducing the need for government borrowing. Hence, the estimates cited here can be considered lower bounds.

Don’t celebrate yet

While growth and inflation helped improve debt-to-GDP ratios over the past two years, significant debt-related challenges remain.

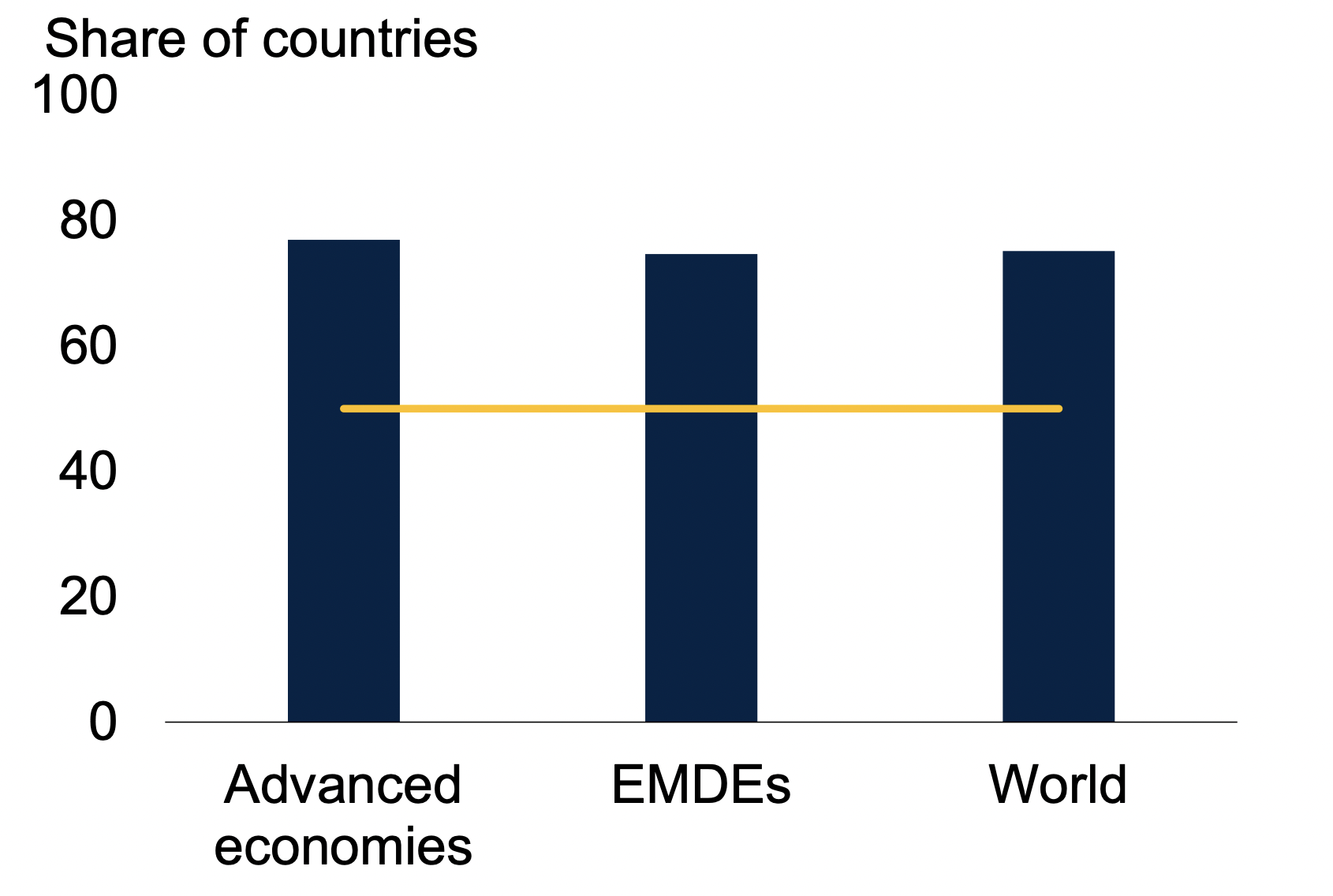

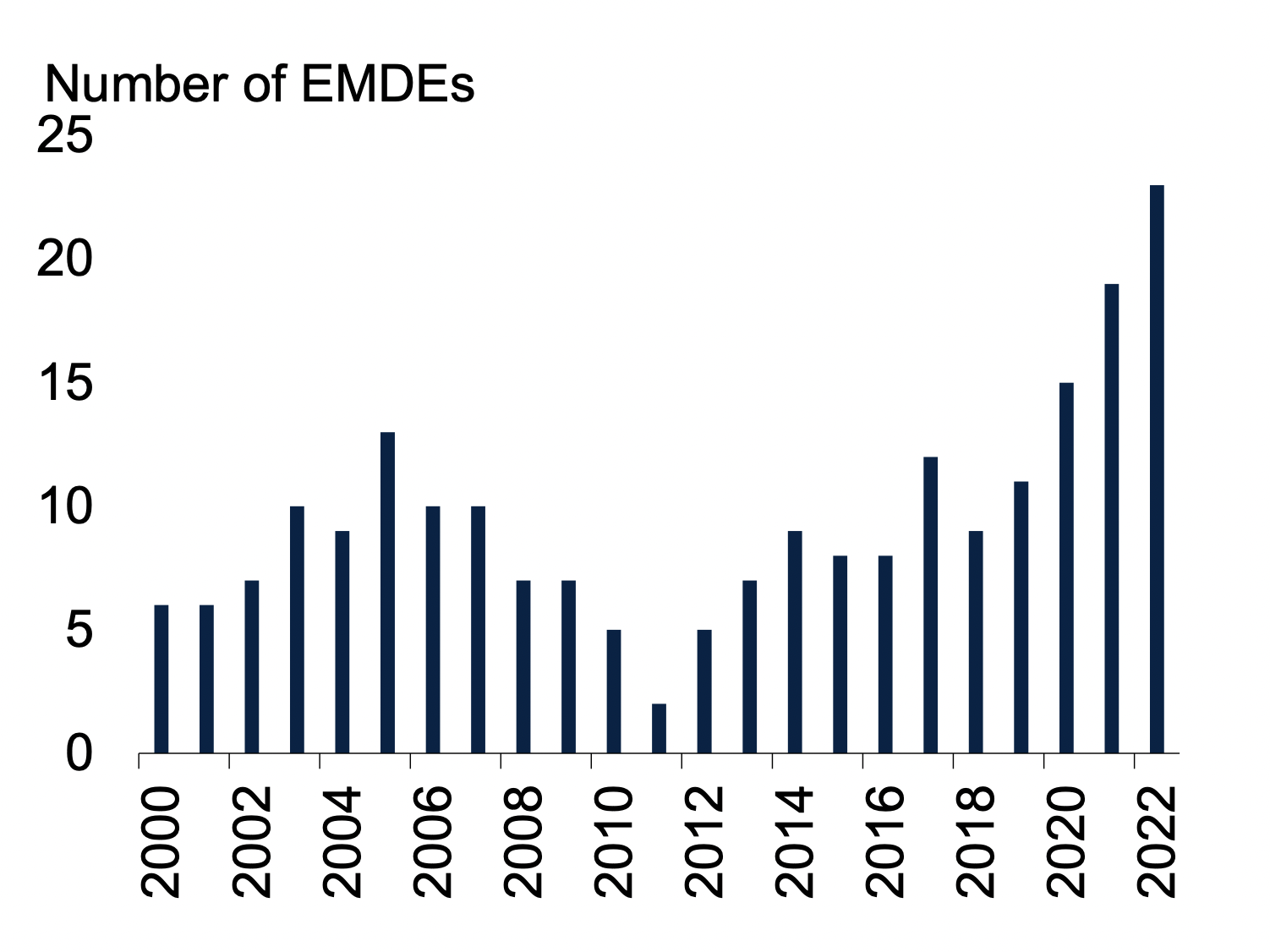

Figure 2. Rise in government debt and debt distress

| A. Countries with a higher debt-to-GDP ratio in 2022 than in 2019 | B. EMDEs in high debt distress or near high debt distress |

|

|

Sources: Kose, Kurlat, Ohnsorge, and Sugawara (2022).

Note: A. Yellow line indicates 50 percent. B. Debt distress is defined as a score of less than 6 in the average long-term foreign sovereign debt rating.

- Still elevated debt. Government debt remains higher than its 2019 level in about three-quarters of countries following the unprecedented fiscal stimulus during the COVID-19 pandemic (Figure 2A). In 2023, slowing growth and tightening financial conditions raise the risk of debt distress in EMDEs as servicing debt is becoming more costly. In fact, rating agencies already rated 23 EMDEs at being in or near debt distress at some point in 2022, the largest number of countries in more than two decades (Figure 2B). Among the poorest countries in the world, more than half of low-income developing economies are already in, or at high risk of, debt distress.

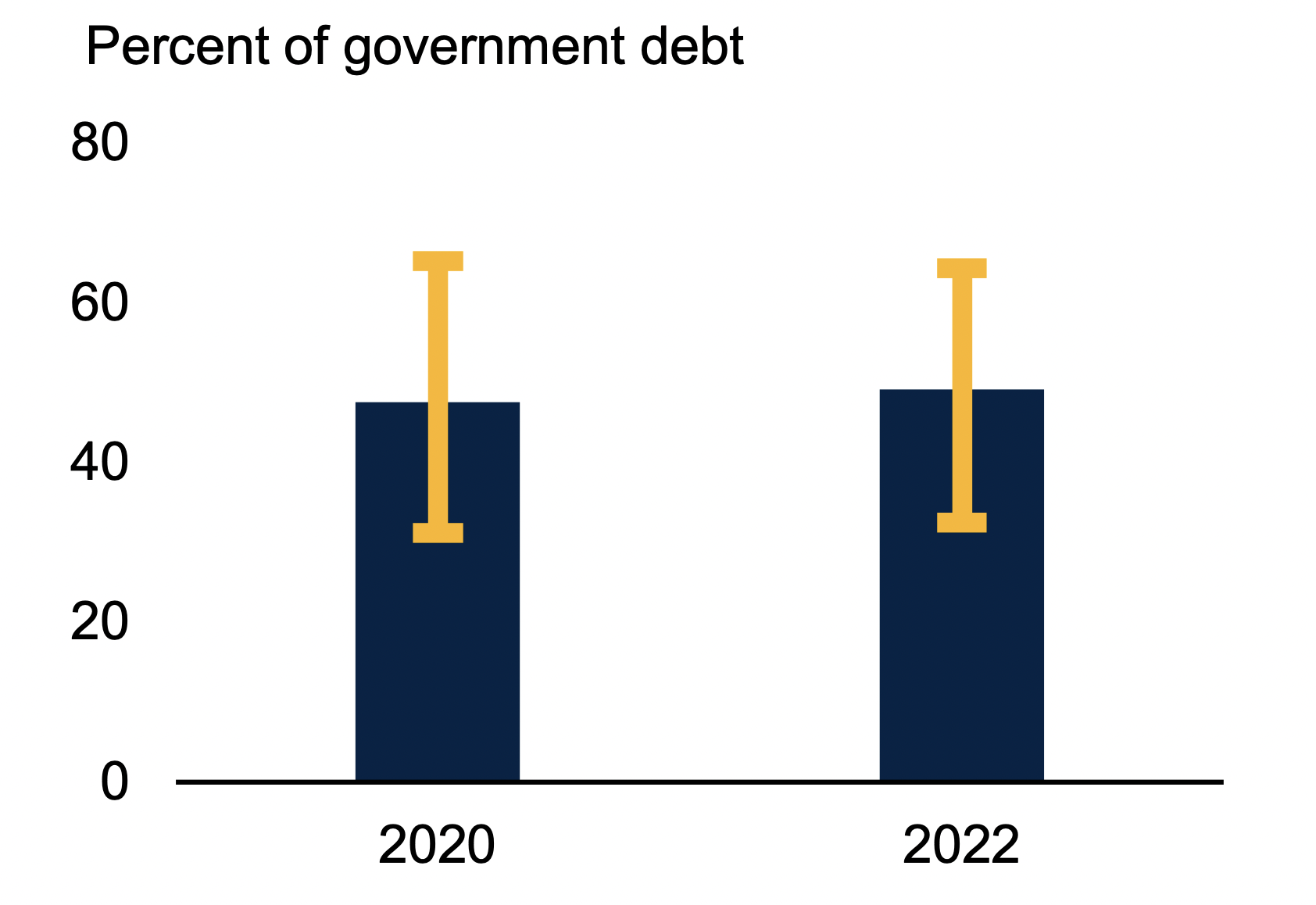

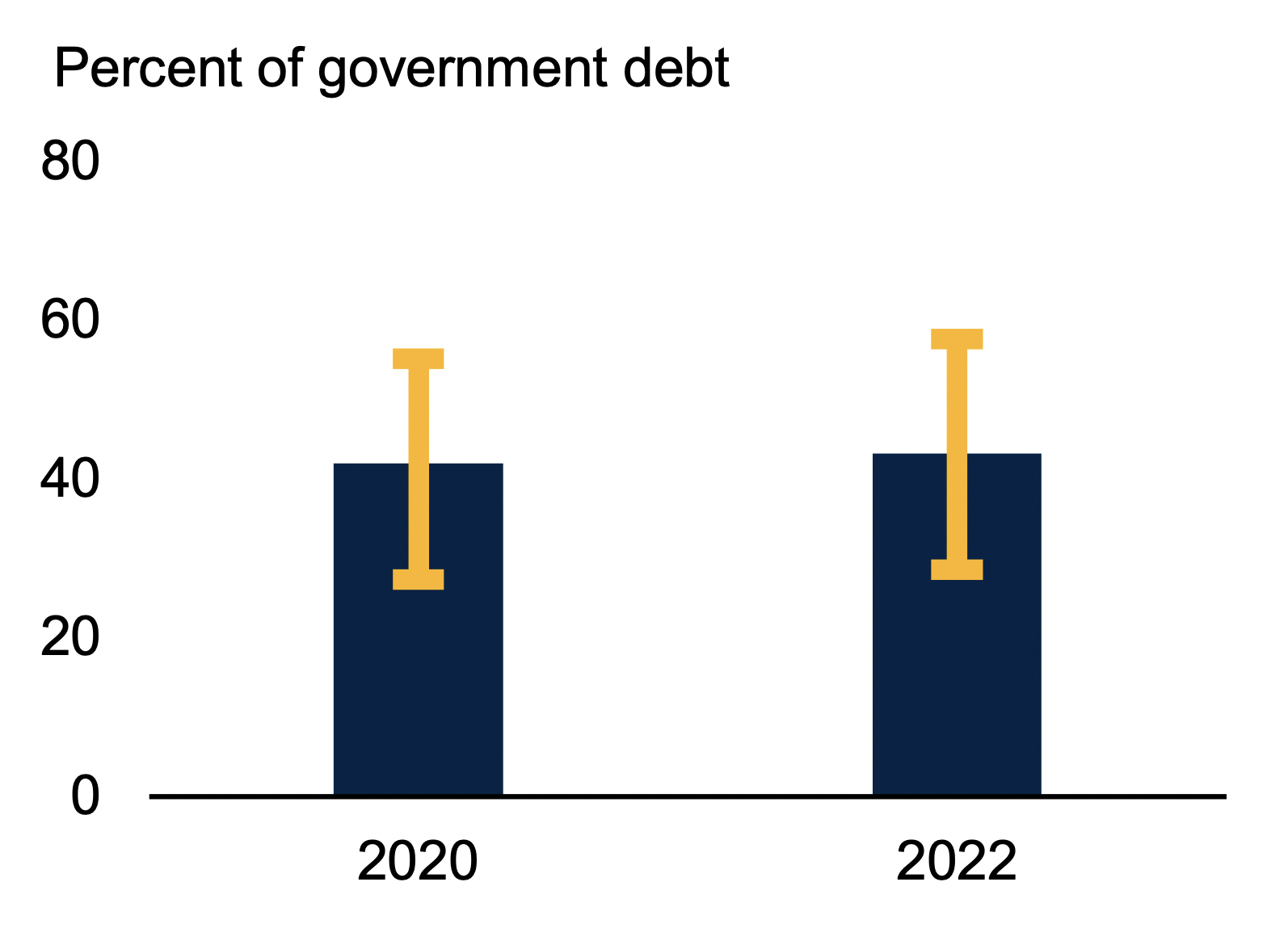

- Still risky debt. The composition of government debt has not materially improved since 2020. In the average EMDE, foreign currency-denominated debt still accounted for nearly 50 percent of government debt in 2022 (Figure 3A); nonresident-held debt accounted for about 45 percent of government debt (Figure 3B). This exposes EMDEs to the risk of rising debt servicing cost because of currency depreciation or loss of international investor confidence.

Figure 3. Composition of EMDE government debt

| A. Share of foreign currency-denominated debt | B. Share of nonresident-held debt |

|

|

Source: Kose, Kurlat, Ohnsorge, and Sugawara (2022).

Note: Blue bars denote unweighted averages, and yellow whiskers interquartile ranges. A. Data for 31 EMDEs. B. Data for 43 EMDEs.

- Weaker growth in horizon. Consensus forecasts anticipate a plunge in global growth to 1.6 percent in 2023 from 2.9 percent in 2022. Longer-term trends also point to weaker growth in the 2020s than in the 2010s. Clearly, governments will not be able to rely on growth alone to lower debt levels.

- Higher borrowing costs. Headline inflation is anticipated to fall as a result of declining energy prices and slowing growth. However, even if headline inflation declines, major central banks will likely keep interest rates high until they see a sustained decline in core inflation. This may present challenges in rolling over or servicing debt in countries with high debt. Were inflation to remain high instead, depreciation pressures and a flight to safety would likely put upward pressure on government debt in some EMDEs.

Reducing debt: What needs to be done

There is no magic bullet to reduce debt levels quickly, but domestic policymakers and the international community can take several supportive measures.

- Policy reforms to deliver strong and sustained growth. Supply-side reforms that lift growth in a lasting manner without causing inflation pressures can help sustainably lower debt. These include reforms to business climates and governance that foster private investment without incurring large fiscal cost, better spending efficiency, and domestic revenue mobilization to boost growth dividends from public spending.

- Policies to maintain low and stable inflation. Inflation cannot be a lasting solution to deal with high debt because economic agents adjust their behavior once high inflation seeps into inflation expectations. Once they reckon that high inflation is here to stay, they adjust their interest rate expectations, wage demands, and pricing strategies accordingly. Even if actual inflation eases, higher inflation expectations would make rolling over short-term debt or additional borrowing to fund fiscal deficits costly. Weaker growth and persistently high inflation rates could put debt-to-GDP ratios on a rising trajectory.

- Debt relief in some cases. The international community also needs to bolster efforts to reduce debt distress and attenuate the risk of debt crises in lower-income developing economies. Debt restructuring at an early stage can help avoid the long and costly adjustment process that sometimes accompanies more incremental efforts and can result in more favorable outcomes for both borrowers and lenders.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Government debt has declined but don’t celebrate yet

February 21, 2023