Standardized mortgage rates offered by Fannie and Freddie provide a substantial regional redistribution

Erik Hurst, Benjamin J. Keys, Amit Seru, and Joseph S. Vavra of the University of Chicago find that because Fannie Mae and Freddie Mac offer standardized mortgage interest rates across the country, regardless of regional default risk, high-risk regions are being subsidized by low-risk areas. The authors conclude that over the course of the Great Recession, this subsidy from high- to low-risk regions amounted to roughly $20.7 billion.

Macroprudential policies reduce the growth rate of credit

Using data on 119 countries between 2000 and 2013, Eugenio Cerutti, Stijn Clasessens, and Luc Laeven of the International Monetary Fund conclude that macroprudential policies generally lead to reductions in the growth rate of credit―particularly so in emerging economies, where macroprudential tools are used most frequently. Additionally, they find that these policies work best during financial cycle booms.

Tax cuts to high-income earners are less effective in generating employment

Owen M. Zidar of the University of Chicago finds that a tax cut equal to 1% of state GDP for the bottom 90% of earners boosts employment growth by 5.1 percentage points over a two year period, whereas the same tax cut for the top 10% of earners leads to only a 0.1 percentage point increase over the same period.

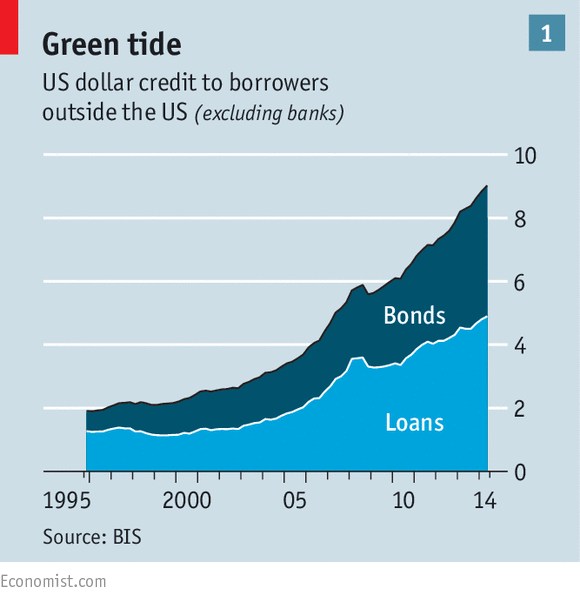

Chart of the week: US dollar credit to foreigners continues to rise sharply

Quote of the week: When the decision to raise rates is made, the federal funds rate is unlikely to follow a smooth path

“Standard interest rate projections might incline one to believe that the path of the federal funds rate after liftoff will consist of a steady rate of increase from zero to the longer-run normal nominal federal funds rate… But a smooth path upward in the federal funds rate will almost certainly not be realized, because, inevitably, the economy will encounter shocks–shocks like the unexpected decline in the price of oil, or geopolitical developments that may have major budgetary and confidence implications, or a burst of greater productivity growth, as the Fed dealt with in the mid-1990s.”

–Stanley Fischer, Vice Chairman of the Federal Reserve Board

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Mortgage Rates, Macroprudential Policies, and More

March 26, 2015