Congress instructs the Federal Reserve to aim for maximum employment and price stability. The Fed has defined price stability as inflation averaging 2%, but maximum employment doesn’t lend itself to such a simple measure. In its monetary policy strategy statement, the Federal Open Market Committee (FOMC), the Fed’s policy-setting body, says: “The maximum level of employment is a broad-based and inclusive goal that is not directly measurable and changes over time owing largely to nonmonetary factors that affect the structure and dynamics of the labor market….[T]he Committee’s policy decisions must be informed by assessments of the shortfalls of employment from its maximum level, recognizing that such assessments are necessarily uncertain and subject to revision. The Committee considers a wide range of indicators in making these assessments.”

What does that mean in practice?

What is maximum employment?

Simply put, maximum employment – sometimes called full employment – is the highest level of employment the economy can sustain without generating unwelcome inflation. It describes an economy in which nearly everyone who wants to work has a job. The unemployment rate is one important way to gauge whether an economy is at maximum employment, but not the only one.

What does the unemployment rate measure?

The headline unemployment rate (U-3) is defined by the Bureau of Labor Statistics (BLS) as the percentage of adults who do not have a job, have actively sought work in the last four weeks, and are currently able to work. The unemployment rate is a percentage of the labor force, the sum of the unemployed plus the employed.

This measure doesn’t, however, account for all idle workers and isn’t a sufficient measure of what’s called slack in the labor market. It doesn’t, for instance, count workers who have given up looking for work or those who work part-time because they can’t find a full-time job. The BLS publishes several alternative measures. The U-6 measure, for instance, counts the unemployed plus discouraged workers (those who’d like to work but have given up looking because they believe there are no jobs available for them), those who are marginally attached to the labor force (those who’d like to work but have stopped looking for work for any other reason), and those working part-time who’d prefer full-time jobs.

Why doesn’t the Fed just look at the unemployment rate?

Primarily because for much of the past decade, the unemployment rate fell and inflation didn’t rise. “Although the unemployment rate is a very informative aggregate indicator, it provides only one narrow measure of where the labor market is relative to maximum employment,” Fed Governor Lael Brainard has said. “For nearly four decades, monetary policy was guided by a strong presumption that accommodation should be reduced preemptively when the unemployment rate nears its normal rate in anticipation that high inflation would otherwise soon follow. But changes in economic relationships over the past decade have led trend inflation to run persistently somewhat below target and inflation to be relatively insensitive to resource utilization.”

In a subtle but significant change to its monetary policy strategy statement, the Fed said in August 2020 that it would respond to “shortfalls of employment from its maximum level” rather than the previous “deviations from its maximum level.” This indicated that the Fed would no longer preemptively tighten monetary policy only because unemployment was approaching or even falling below estimates of the unemployment rate that economist models suggest are consistent with stable inflation. “This change signals that high employment, in the absence of unwanted increases in inflation or other risks that could impede the attainment of the Committee’s goals, will not by itself be a cause for policy concern,” the Fed said.

What does “broad-based and inclusive” mean?

The Fed defines the maximum level of employment as a “broad-based and inclusive goal.” When Fed Chair Jerome Powell announced the addition of that phrase to the Fed’s strategy statement, he said it “reflects our appreciation for the benefits of a strong job market, particularly for many in low- and moderate-income communities.” This reflects calls for the Fed to keep interest rates lower as a way to boost employment in communities, including communities of color, where people are more likely to be unemployed. It also argues for looking beyond the overall unemployment rate to decide whether the economy is at maximum employment. What this means is practice for Fed policy remains to be seen. Some observers have argued that the Fed should keep interest rates low until the Black unemployment rate falls. But Powell has said, “The point of the broad and inclusive goal was not to target a particular unemployment rate for any particular group… And one of the things we look at is unemployment rates and participation rates and wages for different demographic and age groups and that kind of thing.”

Among the other measures of the labor market that the Fed and others track are the following.

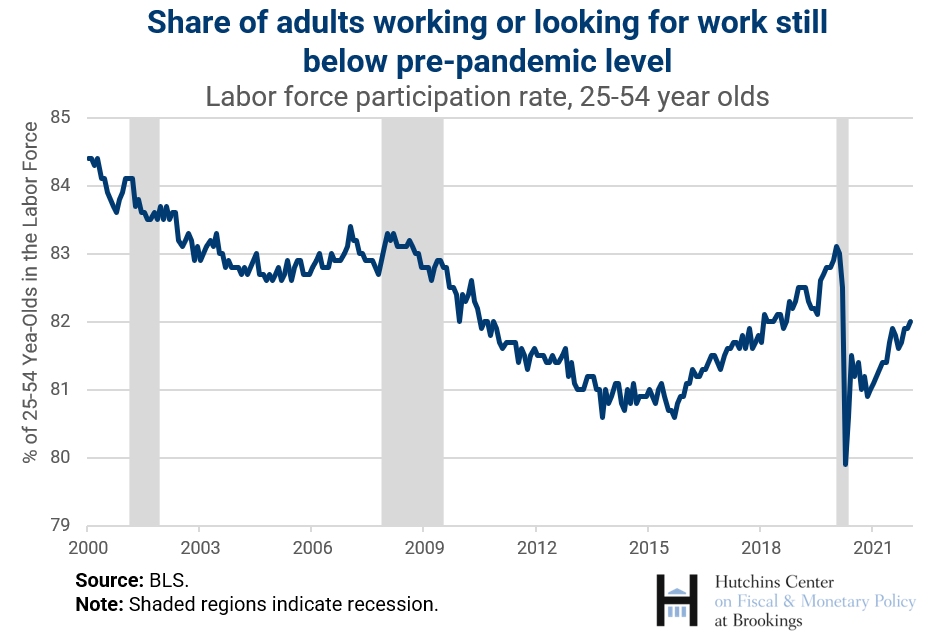

What is the Labor Force Participation rate?

The Labor Force Participation (LFP) rate is the number of employed people plus the officially unemployed divided by the civilian non-institutionalized population older than 16.

In recent years, the LFP rate has been declining as the Baby Boomer generation ages and retires. To look beyond that demographic change, economists often focus on the LFP for people between the ages of 25 and 54, so-called “prime age” because people in this age group are more likely to be available to work. When the prime age LFP rate falls, it means there are more workers on the sidelines of the economy who aren’t counted as unemployed but who may be drawn into the labor force.

In economic downturns, LFP often declines as people stop looking for work. During the pandemic, the LFP rate fell sharply as many parents (particularly mothers) left the labor force due to childcare facility closures and schools shifting to distance learning, and others dropped out for fear of COVID or other reasons, and still others took early retirement. The Fed and other economists have been surprised that the LFP didn’t rebound more quickly when vaccines became available and lockdowns ended.

The failure of the LFP rate to return quickly to pre-pandemic levels led the Fed in late 2021 and early 2022 to judge that the economy was closer to maximum employment than it had anticipated. Powell noted that Fed officials hope “the level of maximum employment… consistent with stable prices may increase… as [labor force] participation gradually rises.”

What is the employment to population ratio?

The employment to population ratio is the employed as a percentage of the civilian noninstitutionalized population. It reflects those people who are counted as unemployed and those who are not working for some other reason—those who are retired as well as those who have given up looking for work.

What are quits?

Using a sample of 16,000 employers, the Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey (JOLTS) measures the number of people who have left their jobs.

The quits rate counts workers who voluntarily left their job as a percent of total employment. The layoffs and discharges rate includes all involuntary separations initiated by the employer. Retirements, transfers, deaths, and disability-related separations are counted in the other separations rate.

Workers are more likely to quit when they feel confident they can obtain another job, so a rising quit rate is a sign of a very strong job market.

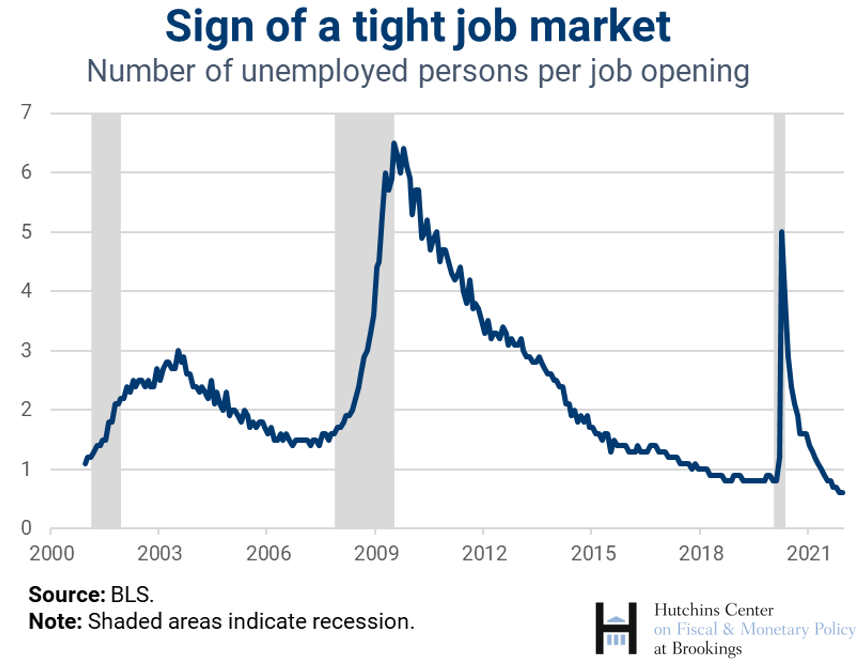

What are job openings?

JOLTS also counts the number of positions for which employers are actively recruiting and would start within 30 days of hire. The number of unfilled jobs is a measure of the unmet demand for labor. The ratio of the number of unemployed per job opening is a way to gauge the strength of the job market; the lower this ratio, the closer the economy is to maximum employment.

What is the Beveridge Curve?

Named for William Beveridge, a 20th-century British labor economist and politician (though he apparently never drew it), the Beveridge Curve charts the number of job postings (as a percentage of all filled and unfilled jobs) against unemployment rate. The Bureau of Labor Statistics updates the chart monthly here. The line generally slopes downward because a higher rate of unemployment usually coincides with a lower rate of vacancies, since there are more people looking for jobs.

Outward shifts in the curve (that is, up and to the right) show a given level of job postings is associated with higher rates of unemployment. They are seen as indicators of unwelcome change in the labor market—an increase in mismatches between the skills of workers and the demands of employers, for instance, or a reluctance of jobless workers to take available jobs. The Beveridge Curve did shift outward following the Great Recession. It shifted further outward during and after the COVID-19 pandemic; in other words, employers found it harder to hire at given rates of unemployment than they had in the recent past. When the unemployment rate fell to 4.2% in November 2021, the job openings rate was 6.6%. In September 2017, when the unemployment rate also hit 4.2%, the job openings rate was 4.1%.

What is the NAIRU?

The NAIRU (Non-Accelerating Inflation Rate of Unemployment) is an estimate of the lowest the unemployment rate can go without leading to rising inflation. The logic is that when there aren’t very many unemployed workers, employers raise wages and that leads to rising prices. The NAIRU is difficult to estimate precisely and can change over time as, among other factors, demographics, union strength, and the pace of productivity change.

Did the Fed consider the U.S. to be at maximum employment at the beginning of 2022?

At his January 2022 press conference, amid growing concern about rising inflation, Powell said that “most FOMC participants agree that labor market conditions are consistent with maximum employment,” which he defined as “the highest level of employment that is consistent with price stability.” The issue, Powell added, is “whether we can raise [interest] rates and move to a less accommodative [monetary policy]… without hurting the labor market.”

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How does the Fed define “maximum employment”?

February 23, 2022