By the end of next year, COVID-19’s economic sting is likely to be an ugly but fading memory for the world’s wealthiest economies: Their GDP levels are forecast to be somewhat higher than pre-pandemic projections indicated they would be by 2023. Not so for most emerging market and developing economies (EMDEs), which will remain debilitated well into this decade.

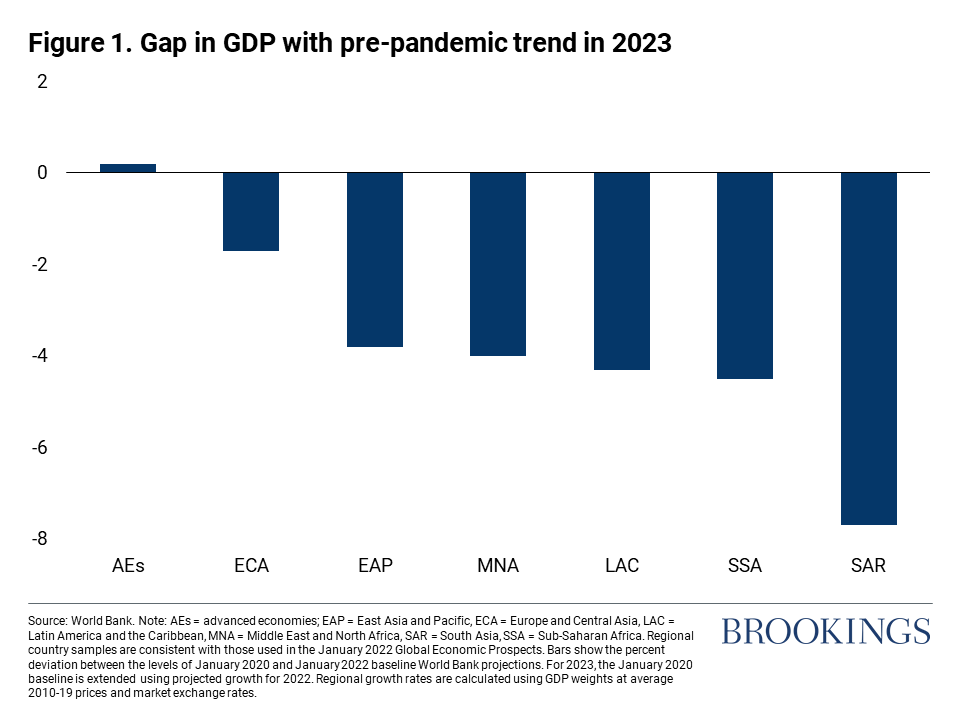

The World Bank’s latest Global Economic Prospects report forecasts that by 2023, just one EMDE region—Europe and Central Asia—will come anywhere close to regaining the GDP level that had been expected before the pandemic (Figure 1). In Latin America and the Caribbean, the Middle East and North Africa, and sub-Saharan Africa, the gap with the pre-pandemic projection is expected to be 4 percent or more. South Asia will be the farthest behind, with its GDP level nearly 8 percent below where it might have been but for COVID-19.

Each of these regions has been hit in ways that warrant customized responses. Four factors make these six regions different, and also provide the clues for quicker recovery and convergence.

Vaccine delays

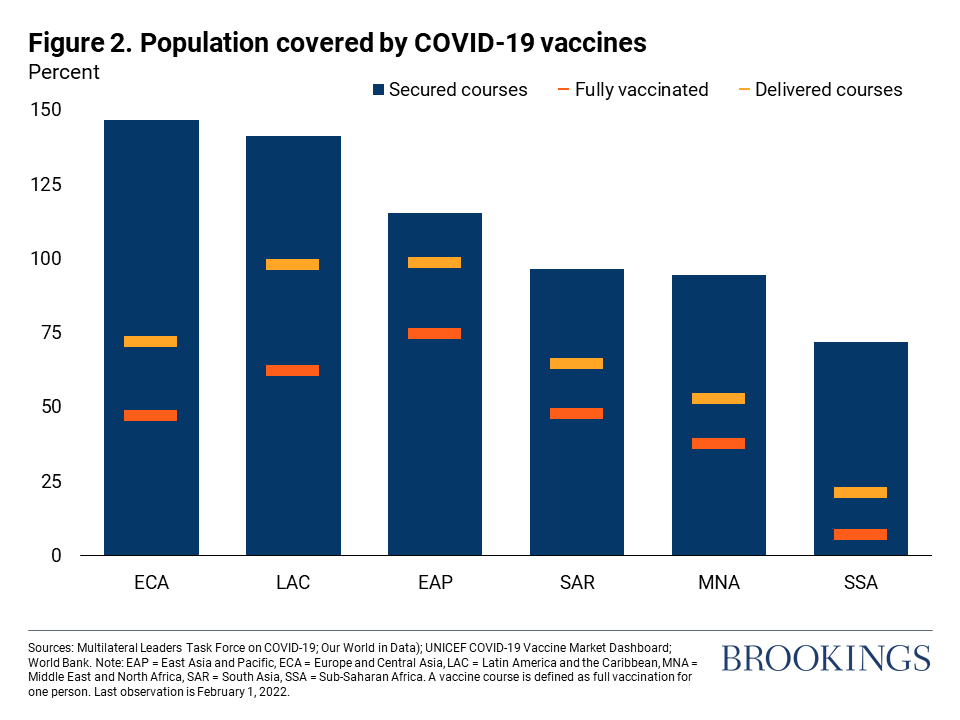

For many countries, vaccine delays are prolonging the pandemic and forestalling a full economic recovery. In all regions except one, large gaps persist between the quantities of vaccine doses contracted and the amounts delivered. The exception is East Asia and the Pacific—and even there, the gap remains large in many countries other than China.

In sub-Saharan Africa, only about 7 percent of the population was fully vaccinated in early February—compared to more than 50 percent of the population of all EMDEs (Figure 2). That reflects delivery delays and financial constraints, predominantly, but also in-country logistical challenges such as insufficient vaccine storage and vaccine sites and difficulties distributing vaccines to rural populations.

For all EMDE regions, the top priority must be to overcome vaccine challenges—quickly. Success will depend on greater global cooperation, including a swift expansion of vaccine donations by nations that enjoy a vaccine surplus. Wealthy countries should also channel additional financial resources—through international financial institutions and regional development banks—to help poor countries improve their access to vaccines.

Rising Financial Stress

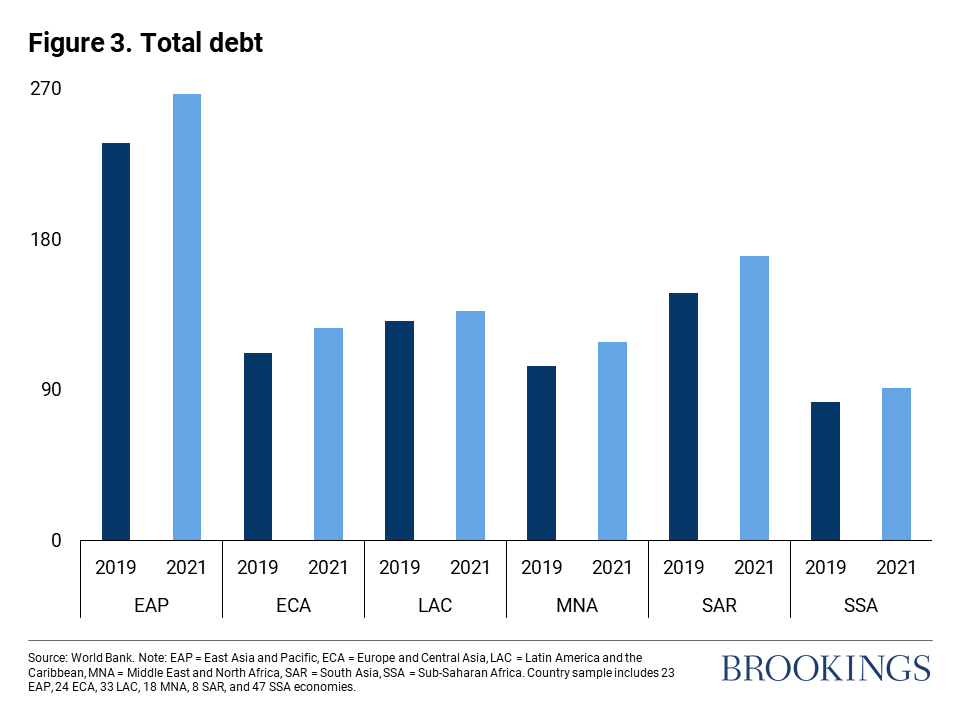

By the end of 2021, GDP-weighted total debt in EMDEs was more than 200 percent of GDP, a 50-year record. The uptick in debt during the pandemic follows a decadelong wave of debt accumulation. In East Asia and the Pacific, business and household debt are at record levels, as is the volume of nonperforming loans held by banks. In Latin America and the Caribbean, South Asia, and sub-Saharan Africa, the largest debt-related risks are in the public sector (Figure 3).

Growing indebtedness means that debt-service burdens in some economies are rising rapidly. At the same time, inflation spiked in 2021 in many EMDEs as energy and food prices rose, demand rebounded along with easing pandemic-related restrictions, and global supply-chain challenges continued. Already, about 40 percent of EMDEs have increased policy interest rates in response. In the near term, central banks in major advanced economies are on the verge of raising interest rates and unwinding exceptional monetary policy support extended during the pandemic. This combination of record-high debt and tightening global financial conditions is perilous, as it makes EMDEs vulnerable to a sudden change in risk sentiment in markets.

Under the circumstances, EMDEs need to carefully formulate their fiscal and monetary policies, focus on rebuilding foreign exchange reserves, keep a close eye on currency risks, and strengthen macroprudential policies. They should also step up efforts to mobilize domestic resources and broaden their tax base.

Volatile Commodity Markets

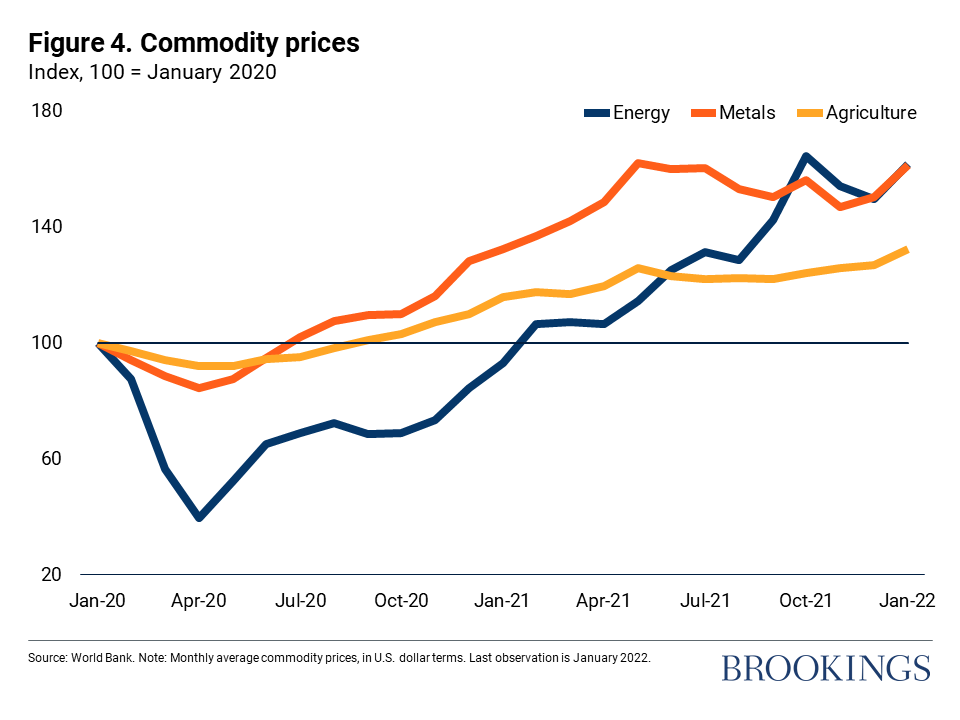

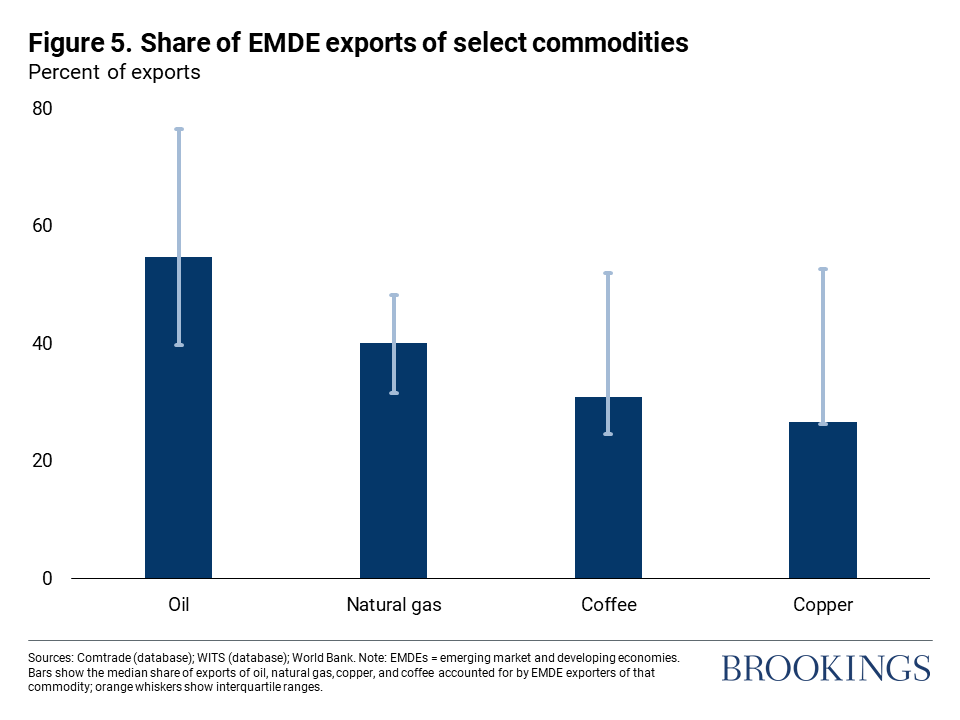

Two-thirds of EMDEs rely on commodity exports for growth and development. These countries—concentrated in Europe and Central Asia, Latin America, the Middle East and North Africa, and sub-Saharan Africa—are regularly buffeted by boom-and-bust cycles, the causes of which are typically beyond their control. More than half the world’s extreme poor live in some of these commodity-exporting countries. After a sharp decline during the early stages of the pandemic, commodity prices have soared (Figure 4).

Governments in commodity-dependent economies can take advantage of the recent uptick in prices to prepare for the inevitable commodity price bust. One imperative is diversification. These countries also need to institute fiscal stabilization, build human capital, promote competition, strengthen institutions, and reduce distorting subsidies. Some commodities represent a large share of total exports, as well as a hefty portion of government revenues (Figure 5). Oil-exporting economies in the Middle East and North Africa, for example, can build their tourism, financial, and high-tech manufacturing sectors. Metal and mineral exporters in Latin America, sub-Saharan Africa, and elsewhere can capitalize on the growing demand for inputs crucial for the longer-term transition to green energy.

Rising Inequality

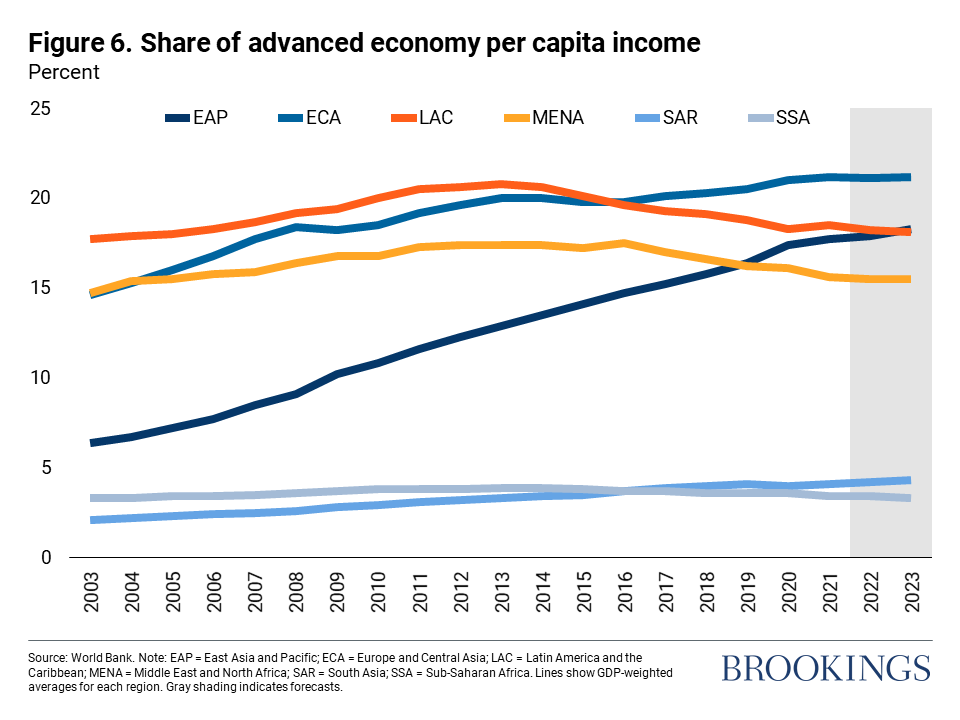

COVID-19 brought an end to a remarkable era of shared prosperity that started in the 1990s: when the income of the poorest nations began to catch up with those of the wealthiest. Today, inequality in incomes between countries is at levels not seen in a decade. Within-country inequality, which was already higher in EMDEs than in wealthy ones before the pandemic, has also risen. That reflects severe job and income losses, especially among vulnerable groups, including low-income people, youth, women, and informal workers. Latin America and the Caribbean and Sub-Saharan Africa face particularly elevated levels of within-country inequality.

Rising inequality should worry us all. Widening income gaps pose risks to social and political stability. Addressing inequality is all the more important when considering that some regions such as Sub-Saharan Africa have made little progress over the past two decades on catching up to advanced-economy levels of income, while the gains in others (Latin America and Middle East and North Africa) have been partly reversed (Figure 6).

Overcoming the detrimental economic effects of the pandemic will not be easy. But it can be done—and the restoration must start now. Some of these challenges underscore the importance of strengthening global cooperation to foster rapid and equitable vaccine distribution, support health and economic policies, enhance debt sustainability in the poorest countries, and tackle the mounting costs of climate change.

National policymakers can achieve much by prioritizing investment in health and education, and by introducing policies that reduce the number of school dropouts and facilitate the reentry into the workforce for those who lost jobs because of the pandemic. Careful calibration of monetary and fiscal policy given the global financial landscape, as well as quick reactions in the case of financial market stress, could help prevent debt crises. Policy efforts that will pay off in the long term—those encouraging diversification and inclusion—must not be laid aside despite the host of near-term challenges.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Getting out of the coronavirus economic contraction

February 16, 2022