Background

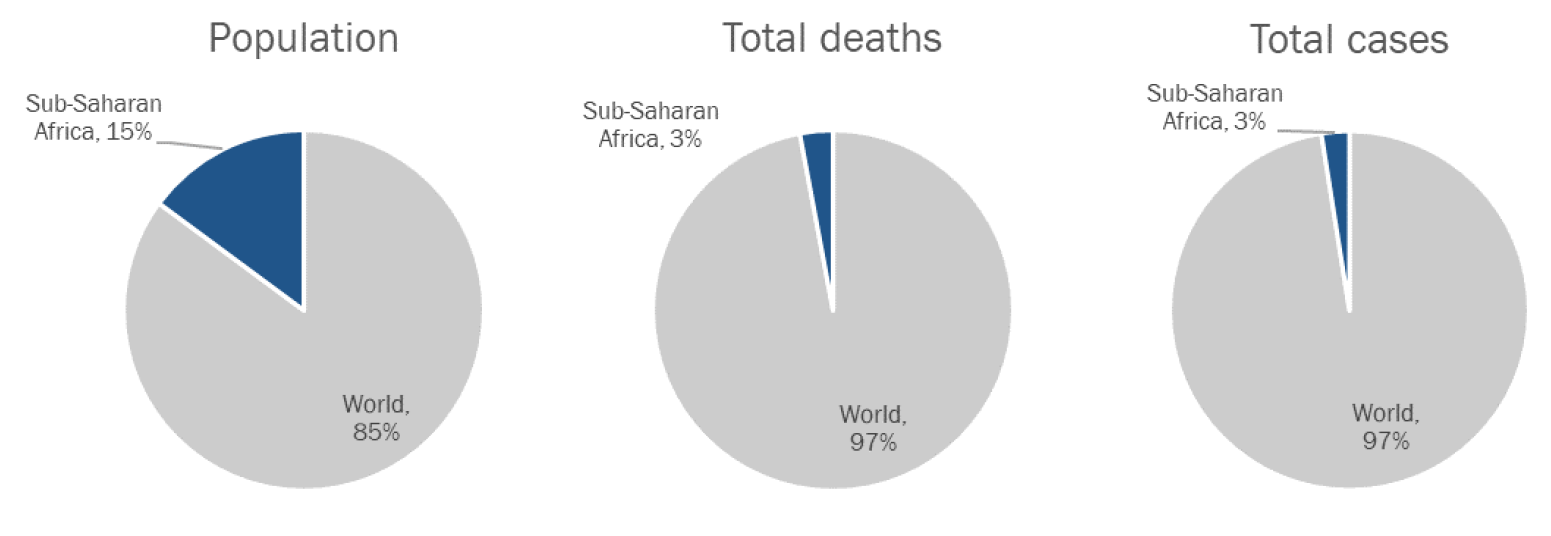

The COVID-19 pandemic has, thus far, spared Africa from the high number of cases and deaths seen in other regions in the world (Figure 1). As of April 2021, sub-Saharan Africa accounted for just 3 percent of the world’s cases and 4 percent of its deaths. Some experts attribute the relatively low case counts in sub-Saharan Africa to the region’s extremely young population or, importantly, the swift and preemptive lockdowns that many countries implemented in March 2020. While these lockdowns have likely saved lives, they have also left significant scars on the fiscal position of sub-Saharan Africa and the market conditions it faces. Dwindling revenues following the fall in global trade met a wave of unemployment among a population that lacks widespread access to safety nets and health infrastructure.

Figure 1. Population, COVID cases, and COVID deaths, sub-Saharan Africa vs. world

Source: Our World in Data, 2021. Data taken on September 1, 2021.

In response, African governments have, by and large, borrowed to finance stimulus packages to support at-risk groups, struggling businesses, creative education solutions, and health-related infrastructure. International and regional financial institutions, such as the World Bank, International Monetary Fund (IMF), African Development Bank (AfDB), and European Union (EU) countries (both bilaterally and multilaterally) have responded through debt relief measures and restructurings. The fiscal and monetary responses of sub-Saharan Africa and various financial institutions will have important consequences for indebtedness, debt servicing capacity, and debt sustainability more broadly.

Debt was an increasing problem across all income groups of African countries prior to COVID-19, and the pandemic has only exacerbated the problem. In fact, African countries had been borrowing heavily in the global financial markets in recent years—a trend that has created both new opportunities and new challenges. Rising debt levels have corresponded with rising debt service cost, but countries have not necessarily improved their ability to finance such obligations. Indeed, failure to meet debt service obligations will have devastating impacts, including downgrading of credit ratings (and, hence, future higher costs), heightened pressure on foreign exchange reserves and domestic currency depreciation, and the real possibility of being rationed out of the market—and negative reputational consequences.

This paper utilizes new data to study the impact of the COVID-19 pandemic on debt sustainability and vulnerability in sub-Saharan Africa and sheds light on the channels through which these impacts have taken place. We find that debt levels have risen substantially in sub-Saharan Africa since the onset of the COVID-19 pandemic. We utilize IMF projections as a comparison to analyze the impacts on the pandemic on debt levels and how they covary with key determinants of growth and fiscal space.

Related Content

In particular, sub-Saharan Africa experienced a 4.5 percent increase in “pandemic debt”—the debt taken on above and beyond projections due to the COVID-19 crisis. HIPC countries in particular saw large increases in pandemic debt, with levels 8.5 percent higher than projected. Non-HIPC countries took on mostly planned debt and borrowed from both private and official (that is, bilateral or multilateral) credit markets alike. HIPC countries, on the other hand, were largely shut out of private credit markets and instead relied on official credit to fund increases in (largely unplanned) debt. We also find that the domestic bond market played a more important role in private borrowing than it has in recent years and that eurobond issuance was relatively scarce. Countries that rely on metal exports issued less pandemic debt than did those that rely on oil, thanks to the strong growth and relative stability of metal prices during the pandemic.

Despite taking on substantial pandemic debt, HIPC countries experienced less extreme drops in GDP compared to their non-HIPC counterparts, underscoring the need for HIPC countries to accelerate financial sector development and enhance public-sector financial management, including mitigating financial leakages, curbing illicit follows, and galvanizing domestic resource mobilization. Looking forward, this paper argues that both sub-Saharan Africa’s recovery and debt sustainability depend on two factors: the success of the African Continental Free Trade Agreement (AfCFTA) and obtaining the participation of private partners in debt restructuring. Economic recovery, in this regard, will affect the millions of informal workers that have lost their jobs at the hands of the pandemic as well as revenue levels that coincide to some degree with the workers’ eventual participation in the formal economy.

Key findings

- Debt levels in 2020 were 4.5 percent higher in sub-Saharan Africa than projections. The increase was particularly acute in HIPC countries, whose debt had mirrored non-HIPC countries the decade prior.

- Non-HIPC countries and especially upper-middle-income countries retained access to credit markets and used a mixture of private and official creditors to finance increases in debt (which were largely in line with projections).

- HIPC countries were largely shut out of private debt markets and instead relied on unplanned borrowing from official creditors.

- Domestic bond markets played a relatively more important role in private borrowing. Eurobond issuance dropped sharply.

- Some resource-rich countries saw sharp increases in bond yields despite having comparatively low yields pre-pandemic.

- Metal prices showed more stability and higher growth than oil prices during the pandemic. Consequently, top metal exporters took on less debt than top oil-exporting countries.

- Many sectors, especially manufacturing, witnessed “formalization” of employment during the pandemic.

Policy recommendations

- Obtain full participation of all creditors, including private ones, in debt restructuring

- Accelerate financial sector development

- Enhance public financial management and internal resource mobilization

- Mitigate financial leakages and illicit flows

- Harness and accelerate opportunities afforded by AfCFTA

- Design incentive-compatible and state-contingent contracts

- Revisit existing institutional mechanisms for debt resolution

This paper is organized as follows. Section 2 begins by taking brief stock of the region’s debt landscape prior to the advent of COVID-19, before illustrating how the debt burden has changed during the pandemic. It also reviews key reasons why indebtedness has risen, including stimulus packages, current account deficits, and borrowing costs. Section 3 examines key economic channels along which the pandemic shock unfolded. Section 4 considers the magnitude of revenue loss and the vulnerability of the informal workers during the pandemic. Section 5 discusses attempts to rectify the unexpected, unsustainable increases in debt (or “pandemic debt”) and explores important considerations of which effective policies must take account. Section 6 recommends a number of policies and the way forward.

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).