In 2015 and 2016, economic growth in sub-Saharan Africa’s largest economies (Nigeria and South Africa) stagnated or declined, leading to a deceleration in overall growth for the region. A new paper from the International Monetary Fund’s Spillover Task Force, titled, “Regional Spillovers in Sub-Saharan Africa: Exploring Different Channels,” examines the extent to which regional spillovers through trade, banking, financial, remittance, investment, fiscal, and security channels have influenced recent patterns of economic growth throughout the continent. It also ascertains which countries are more likely to generate and be affected by spillovers through these various channels.

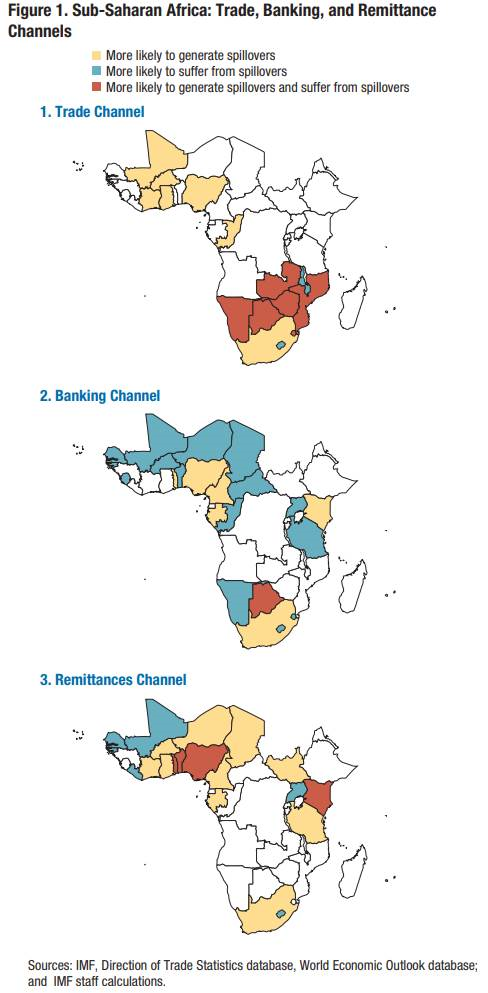

Figure 1 presents the countries where spillovers in trade, banking, and remittances are more likely to originate from and which countries are more likely to be exposed to the spillovers. According to the report, “intraregional trade and remittance flows are an important channel for growth spillovers, while banking channels are less important but will remain a risk going forward.” Notably, the countries with the potential to generate the largest trade spillovers are highly concentrated, with just 10 countries accounting for 65 percent of total regional demand—of which South Africa, Botswana, and Namibia represent the largest shares. Declines in economic growth in these countries could lead demand for intraregional exports to weaken, leading to negative effects on growth in exporting countries.

Meanwhile, a few countries that are home to pan-African banks and subregional banks, are more likely to generate spillovers in the banking sector, while the countries exposed to these spillovers are more widespread. The report argues that financial development and deepening have generally had positive implications for growth in sub-Saharan Africa. However, it notes that negative spillovers from credit supply and solvency issues can affect cross-border entities depending on the structure of the banking group.

Furthermore, remittances within sub-Saharan Africa are a growing source of financing, quickly surpassing other external sources of financing such as aid, foreign direct investment (FDI), and remittances from elsewhere in the world. The key players in regional remittance outflows include Côte d’Ivoire and Ghana as sources for West Africa, and South Africa as an important source for Southern and East Africa. According to regression results in the report, growth in countries sending remittances can spill over into the receiving countries, with a 1 percent increase in GDP growth in the origin countries associated with a 0.1 percent increase in growth in the receiving country (for origin countries that belong to the same region). As costs to send money across borders continue to fall, there could be scope for even greater increases in regional remittances.

In summary, the report finds that sub-Saharan African countries are more interdependent than generally acknowledged, and the potential for both positive and negative spillovers through a variety of channels is higher than assumed. The largest economies on the continent generate a diverse array of spillovers: for South Africa, through trade, banking, and remittance channels, and for Nigeria, mainly banking and trade. The report therefore suggests that further research on spillovers should focus not only on traditional bilateral analysis, but continue to focus on regional spillover analysis as well.

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Figure of the week: Exploring economic growth spillover channels in Africa

August 10, 2018