The COVID-19 pandemic triggered the largest global economic crisis in more than a century. Many of the households that faced sudden income losses and health expenses were ill-prepared to withstand shocks of that scale and duration. Women, in particular, were affected because they were likelier to be employed in sectors with lockdowns and social distancing measures, and were often needed to increase their family caregiving responsibilities. Digital government payments—into accounts, cards, and phones—provided critical financial support to such people in need while following public health safety advice at the same time.

When the economic crisis brought on by COVID-19 left many seeking help from the government, countries with digital public infrastructure such as broadband connectivity, identification, and payment systems, along with infrastructure for data sharing, were able to reach more of their poorest residents in a targeted and transparent manner. A recent paper on the role of digital systems during the first year of the COVID-19 pandemic shows that among 85 countries, those that were able to leverage digital databases and trusted data-sharing reached on average around half of their populations. Digital government payments provided a lifeline for millions, some of whom may have also benefited from a path to financial inclusion.

Leveraging digital infrastructure offers a range of benefits for governments and recipients. For governments, sending payments directly into financial institution accounts (including mobile money accounts) not only enables them to reach more people quickly and safely, but it also reduces the leakage and corruption that can result from distributing cash. For recipients, government payments can create a pathway to financial inclusion and economic empowerment, especially for underserved groups such as women and youth. Global Findex data finds that 865 million account owners in developing countries (18 percent of adults), including 423 million women, opened their first financial institution account for the purpose of receiving money from the government.

People receive money from the government for a variety of reasons: transfer payments for educational or medical expenses, unemployment benefits or subsidy payments, as well as pensions and public-sector wages. Among those who received government transfers (excluding pensions and wages) in developing economies, 64 percent received a payment digitally and 15 percent did so in cash. The remaining 20 percent of government transfer recipients received their payment neither digitally nor in cash, likely through a voucher or one-time passcode; in-kind payments are also possible.

Increasing usage of digital payments among government transfer recipients

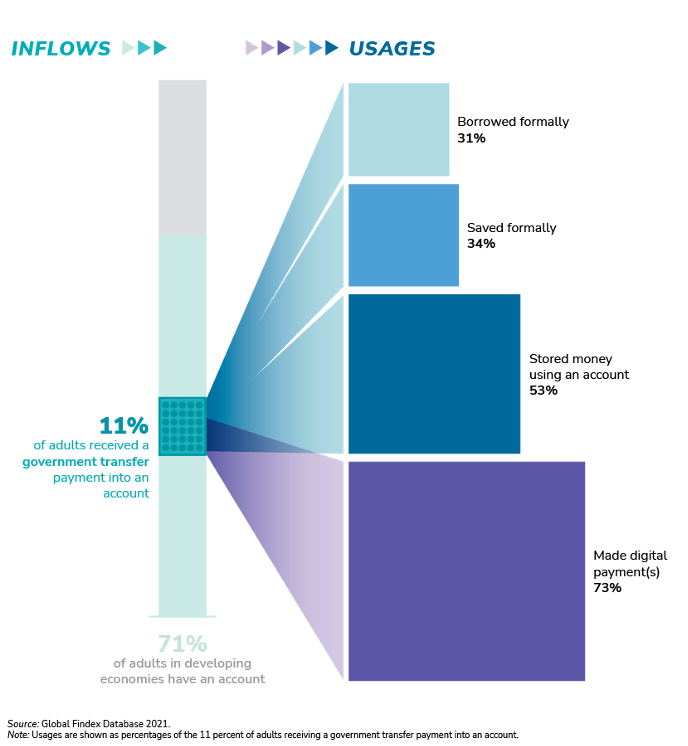

Access to an account and receiving payments are necessary steps toward financial inclusion. As important is ongoing usage of financial services. Here, too, the data show that among government transfer recipients, around seven out of every 10 who received their payment into an account also made a digital payment—an increase from only about half of the recipients in 2017. Such payments included using the internet to pay bills or to buy something (49 percent) or using an account to make in-store purchases (54 percent). Beyond digital payments, 34 percent of those digital government transfer recipients also saved at a formal financial institution or mobile money account. The increased use of accounts by government transfer recipients indicates strong progress toward bridging the gap from access to usage of formal financial services.

Figure 1. Adults in developing countries who receive a government transfer payment into an account

While we have come a long way in recent years, there is still a big opportunity to further digitize government payments to help bring a share of the 1.4 billion adults that remain unbanked into the formal financial system. The G2Px Initiative is one of many efforts by the World Bank Group, in partnership with the Bill & Melinda Gates Foundation and Norad, to support governments in radically improving government payments. Closing the gap will require that governments complement payment digitalization with programs that build digital and financial literacy. The goal would be to adopt policy and design choices that put recipients of such payments at the center along with establishing a strong consumer protection framework. A multi-pronged approach will be essential to ensuring that everyone, including women, those with disabilities and other marginalized groups, can access and use their accounts or make digital payments with confidence.

Among the unbanked, we know that at least 61 million adults in developing economies receive government transfer payments in cash, including 35 million women. Digitizing government transfers can play an important role in these people’s journey toward financial inclusion.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Does digitizing government payments increase financial access and usage?

November 15, 2022