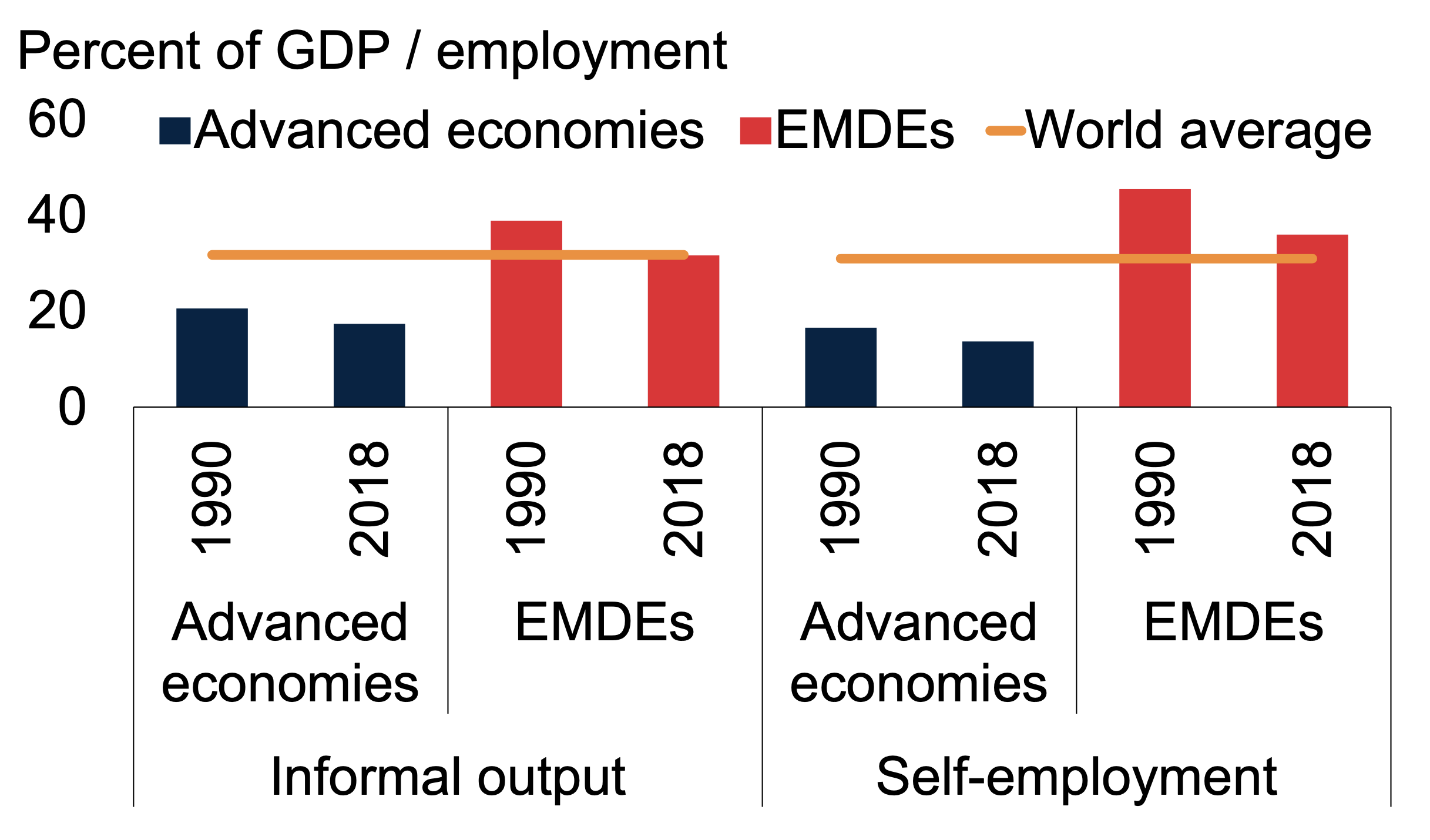

Informal economic activity is widespread around the world. On average, such activity accounts for about one-third of output, and informal employment captures almost one-third of total employment (Figure 1). It undermines revenue collections, stunts productivity, hinders investment, and traps some of the most vulnerable workers in low-paying, unproductive employment. For policymakers in countries with widespread informality, it is a formidable challenge.

Figure 1. Informality around the world

Sources: Elgin et al. (2021).

Note: Bars are simple averages. “EMDEs” stands for emerging market and developing economies. Informal output is proxied by dynamic general equilibrium (DGE) model-based estimates in percent of official GDP. Self-employment, a common proxy for informal employment, is in percent of total employment. World averages between 1990-2018 are in orange.

Underdeveloped financial systems have often been identified as a potential cause of informality but the direction of causality has been difficult to pin down. Financial development can influence the benefits and costs of informal economic activity undertaken by firms and households. Firms in the informal sector are typically characterized by small scale, low capital-to-labor ratios, lack of investment, low productivity, a low propensity to implement new technologies, and unskilled managers. By influencing firms’ investment strategies, financial development promotes the transition of informal firms into the formal sector and, ultimately, encourages capital accumulation and productivity improvements.

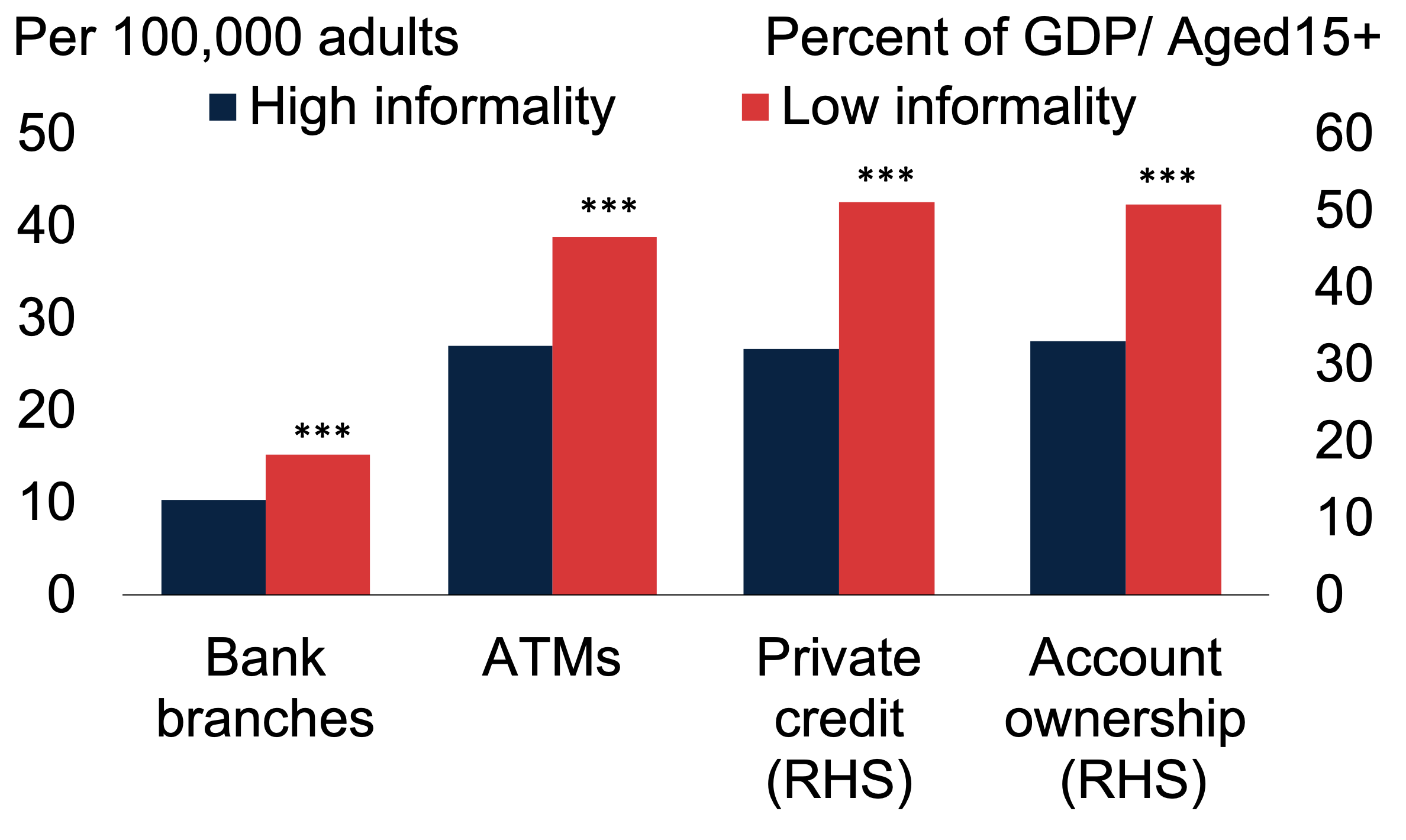

Plenty of empirical evidence shows that financial development is correlated with lower informality. Many empirical studies have found a robust and significant result, for different sets of countries, time periods, and definitions of financial development and informality, and controlling for numerous factors: Greater financial development is associated with less informality (Figure 2).

Figure 2. Financial development and informality

Sources: Ohnsorge and Yu (2022).

Sources: Ohnsorge and Yu (2022).

Note: Bars show simple averages for EMDEs over the period 2010-18. “High informality” (“Low informality”) are emerging market and developing economies (EMDEs) with above-median (below-median) dynamic general equilibrium (DGE)-based informal output measures. “Bank branches” measures the number of commercial bank branches per 100,000 adults. “ATMs” measures the number of automated teller machines (ATMs) per 100,000 adults. “Private credit” measures domestic credit to private sector in percent of GDP. “Account ownership” is the percentage of survey respondents (aged 15 and above) who report having an account (by themselves or together with someone else) at a bank or other financial institution, or report personally using a mobile money service in the past 12 months. *** indicates group differences are not zero at 10 percent significance level.

From correlations to causality

But is it financial development that lowers informality or vice versa? The literature is divided on this question.

Several theoretical studies have identified the various channels that may give rise to a negative relationship between financial development and informality, with causality that may be running in either direction. These studies essentially compare the costs of operating informally, such as more costly access to external financing, with the benefits, such as avoiding regulatory and tax compliance burdens.

The main notion behind most of the studies arguing for a causal link from financial development to informality is that, in the presence of information asymmetries, informal firms and workers face a higher cost of credit since they are more opaque to external creditors. High financing cost, in turn, reduces the attractiveness of formal-sector activity. As financial markets develop, the cost of credit decreases, and formal-sector activity becomes more attractive. And yet, there are also arguments to support the idea that the causality runs from informality to lower financial development. Specifically, more pervasive informality lowers aggregate investment and this, in turn, is accompanied by shallower capital markets.

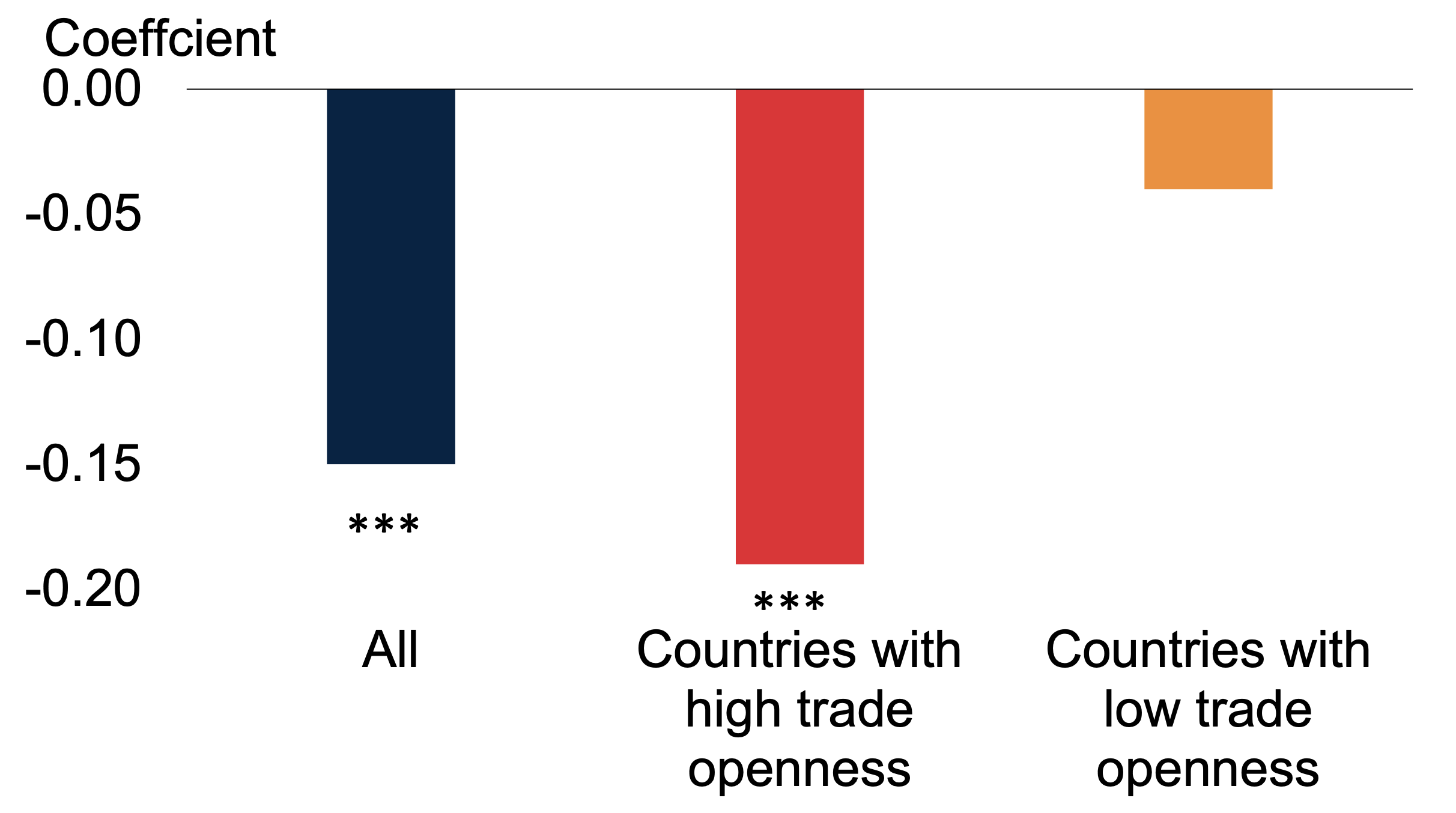

This approach shows that greater financial development indeed lowers informal sector activity. This causal link is stronger in countries with greater trade openness and capital account openness.

In our new study, we employ an instrumental variable approach to show that the direction of causality runs from greater financial development to lower informal-sector activity. Specifically, the approach exploits one aspect of financial development that is likely to be most relevant for the vast majority of informal workers and firms: relationship banking. Relationship banking requires close interactions between the bank and the borrower and typically also requires the presence of bank branches where these relationships can be established and nurtured. Inspired by a large body of literature that documents the link between domestic and foreign banking sector development, we use the strength of branch networks in geographically close countries as an instrument for financial development.

This approach shows that greater financial development indeed lowers informal sector activity. This causal link is stronger in countries with greater trade openness and capital account openness (Figure 3). The findings are robust to the use of alternative indicators of informality and financial development.

Figure 3. The impact of bank sector development on informality

Sources: Capasso, Ohnsorge, and Yu (2022)

Sources: Capasso, Ohnsorge, and Yu (2022)

Note: Bars show estimated coefficients for commercial bank branches (used as a proxy for bank sector development) when regressing against DGE-based informal output as a share of official GDP. “High (low) trade openness” are countries where trade flow (i.e., imports plus exports) as a share of GDP is above (below) median. Commercial bank branches are per 100,000 adults and instrumented by the average number of bank branches in the region (excluding the country under consideration; discounted by distance). Data are between 2004 and 2018. *** indicates that the coefficients are significant at 10 percent significance level.

Policy promise

For policymakers, this is a promising finding. Our results suggest that efforts to strengthen financial development, which are typically undertaken for reasons unrelated to informality, may also be an effective tool to lower informality.

A wide range of policy tools has been identified to foster financial development and financial inclusion. Such policies have often aimed at increasing domestic savings and investment, reducing poverty, and reducing financial vulnerabilities. They have included, among many others, measures to strengthen credit registries; broaden mobile payment and banking systems; digitize transactions and records; and increase competition among financial service providers while strengthening regulation and supervision. Our results show that such policies can also increase the attractiveness of operating formally, in part by removing information asymmetries and reducing financing costs. Hence, financial development can be an effective part of a broader policy agenda to reduce informality.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Financial development to formalize economies

September 30, 2022