The radical social, economic, and employment changes spurred by the COVID-19 pandemic resulted in many people rethinking their living arrangements. These changes substantially affected the U.S. housing market, though not always in the same way. For example, homeowners may have been reluctant to list their properties for sale and home buyers may have been reluctant to shop for homes during the pandemic out of fear of actually catching COVID-19. At the same time, housing demand increased as the pandemic forced people to spend more time at home and thus increased the demand for housing. Limited empirical research investigates these trends in detail or explores how these trends have differed over the course of the pandemic and across different geographies. To address those questions, we present an analysis of home price dynamics at different stages of the pandemic which differed based on geographic characteristics—geography and urbanicity.

To examine housing market dynamics during the COVID-19 pandemic, we utilize Zillow’s Home Value Index (ZHVI), a seasonally adjusted measure of home values aggregated at the ZIP code area level. We selected 12 core-based statistical areas (CBSA) from major metropolitan areas in the United States and categorized them into four metro types: Established (Boston, New York, Philadelphia, D.C.), Growing (Denver, Portland, San Francisco, Seattle), Rust Belt (Baltimore, Cleveland, Detroit, St. Louis), and Sun Belt (Dallas, Houston, Nashville, Phoenix) metropolitan areas. We use the NCHS Rural-Urban Classification Scheme for Counties to categorize the ZIP code areas of interest into urban and suburban metro areas. To understand how different stages of the pandemic affected home prices in these areas, we divide the pandemic into five phases—Pre-COVID-19 (Feb 2019—Feb 2020); COVID-19 Outbreak (Mar 2020—Oct 2020); COVID-19, Vaccine (Nov 2020—Jun 2021); COVID-19, Delta variant (Jul 2021—Dec 2021); COVID-19, Omicron variant (Jan 2022—Mar 2022).

How did property values change during the COVID-19 pandemic?

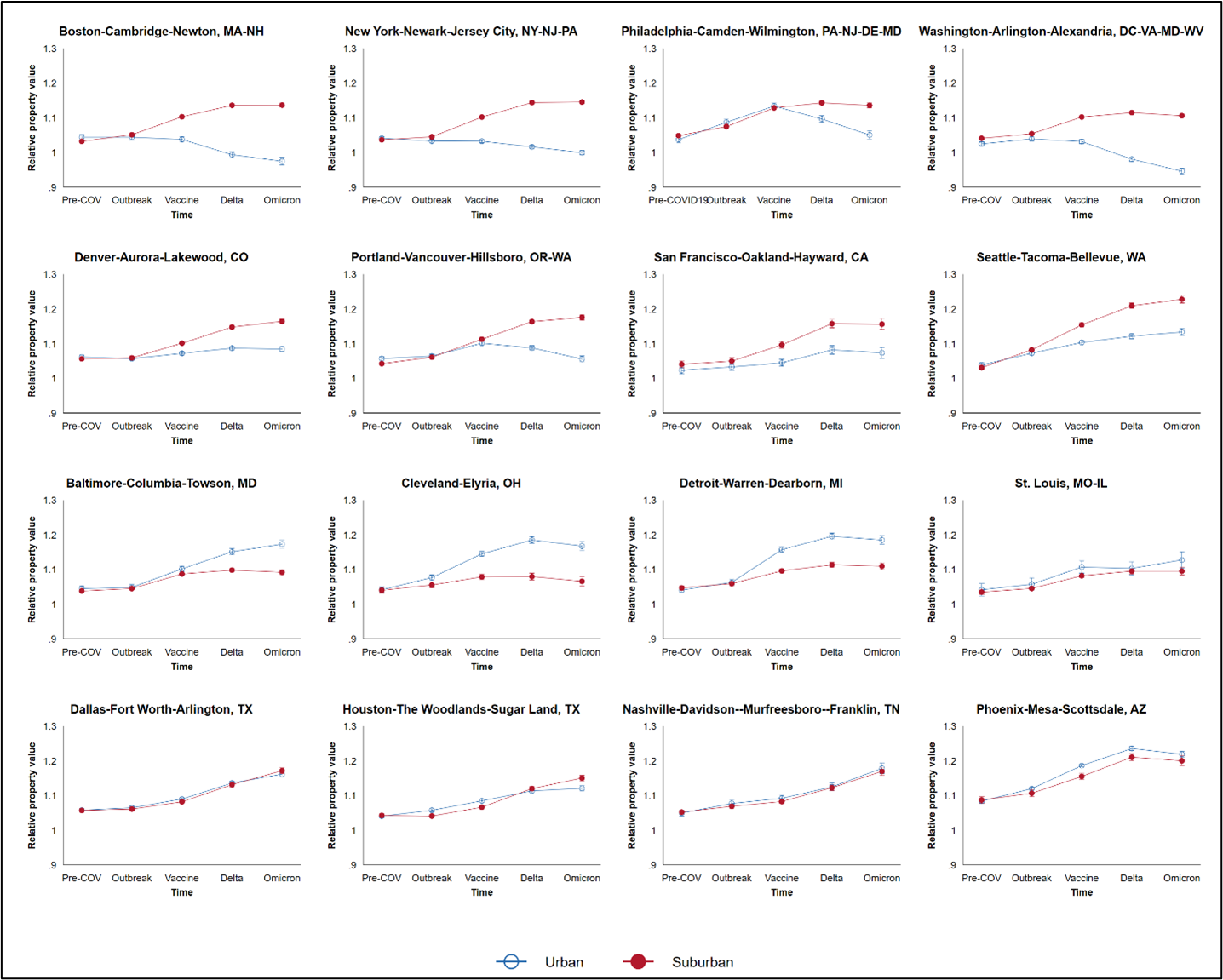

Figure 1 displays relative housing price estimates (baseline period: February 2020) during the pandemic controlling local COVID-19 severity and macroeconomic dynamics in the U.S. during the study period. Overall, the property values significantly increased in most study areas during the pandemic (i.e., relative property value is greater than 1). Property value changes accelerated after COVID-19 vaccine distribution and slowed later in the pandemic (Omicron variant).

Interestingly, the shapes of the change vary across geography as well as urbanicity. Established metropolitan areas exhibited significant gaps in property value changes between urban and suburban property markets. In New York, for instance, the property values increased in suburban areas (including upstate New York, Long Island, and New Jersey), whereas those in New York City subtly decreased. Further, the gap between the two areas—urban and suburban—widened as the pandemic prolonged. The Boston and D.C. areas showed a more pronounced version of this trend, experiencing significant price drops in their urban center(s) during the pandemic. Although the gap between urban and suburban property markets is narrower than in the other three areas, the Philadelphia metropolitan area displayed a significant price gap between the two in the later pandemic stage. The four growing cities in the West displayed similar patterns; the property value change gap between urban and suburban areas became significant from the COVID-19 vaccine distribution (Denver, San Francisco, and Seattle) or the delta variant (Portland). Unlike some established metropolitan areas in the East, however, the price change gaps in West Coast cities were not because of price drops in urban centers. Rather, the gaps in the West Coast cities were driven by the rapid market value increases in their suburban areas.

The latter two types of metropolitan areas were somewhat different from the previous two. To some extent, both urban and suburban areas in the Rust Belt experienced market inflations during the pandemic. Interestingly, unlike established metros in the East and growing cities in the West, the property value increases in the urban cores of four Rust Belt metropolitan areas outpaced those in their suburban counterparts. In Baltimore, Cleveland, and Detroit, the urban-suburban gap became significant from the relatively early stages of the pandemic (outbreak and vaccine periods). On the other hand, in St. Louis, the property value changes between the two have been parallel, but their gap was not significant. Lastly, the four metropolitan areas in the Sun Belt showed very different price patterns during the pandemic. Unlike the other three types of cities, which exhibited significant price change gaps between urban and suburban areas, both urban and suburban areas in the Southern metropolitan areas displayed steady increases in property values during the pandemic. Notably, although the Phoenix metropolitan area showed a significant gap in property value changes, there was no significant gap between them in the latest period (Omicron).

Figure 1. Relative property value changes (baseline period: February 2020)

Notes: 95% confidence intervals plotted; Random effect models at the Zipcode level (monthly) controlling COVID-19 death, CPI, and unemployment rate; Seasonality adjusted; The relative value baseline is February 2020.

Data sources: Zillow (housing price), New York Times (COVID-19 deaths), and Bureau of Labor Statistics (CPI and unemployment rate).

Conclusions

Our findings have important implications for both the U.S. labor and housing markets. First, the labor market. The housing market inflations in previously stagnant urban areas in Midwest and in suburban regions in the West and East imply that employees may have migrated to these areas during the pandemic as an environment of more flexible work arrangements took hold. In turn, employers seeking to return to pre-pandemic workplace policies with more required on-site time may face challenges. Residential moves are time-consuming and involve significant costs; employees who have made such moves and adjusted to remote working environments may be unwilling to return to locations near their workplaces. While the future trajectory of these trends remains to be studied, they suggest a decoupling of workplace location and residential preferences that will likely require adjustments from employers in the largest urban counties.

Second, the housing market. The decoupling of workplace location and residential preferences suggests that home buyers may prefer homes in smaller and less dense counties that offer lower living costs and larger living spaces during and even after the pandemic. On the one hand, they signal opportunities for the local economy—especially in Rust Belt urban centers that have seen decades of population loss—seeking to capitalize on newly increased housing demand. On the other hand, however, they become a crisis for existing residents in the overheated areas—especially potential first-time home buyers as well as renters. Given that rising housing prices outpace wage growth, the housing market inflation in previously (relatively) affordable neighborhoods would make these areas less- or unaffordable, especially for lower-income families. It is clear that the COVID-19 pandemic drastically altered the geography of the U.S. housing market as well as the labor market, but the accompanying economic, social, and demographic shifts are only beginning to come into focus.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Did the pandemic advance new suburbanization?

May 23, 2022