Candidate Trump promised to label China a currency manipulator on day one in the White House. In recent months, however, China has been intervening to keep its currency high, not low. It turned in another good growth performance in 2016, with a 6.7 percent expansion. But it took a lot of credit to generate this growth—as a result, risks are building up in China. One risk is of a classic financial crisis; another risk is unruly devaluation of the currency driven by market forces. China can probably avoid a hard landing this year, but it is relying on ad hoc measures that throw sand in the wheels of normal commerce.

Mind the gap

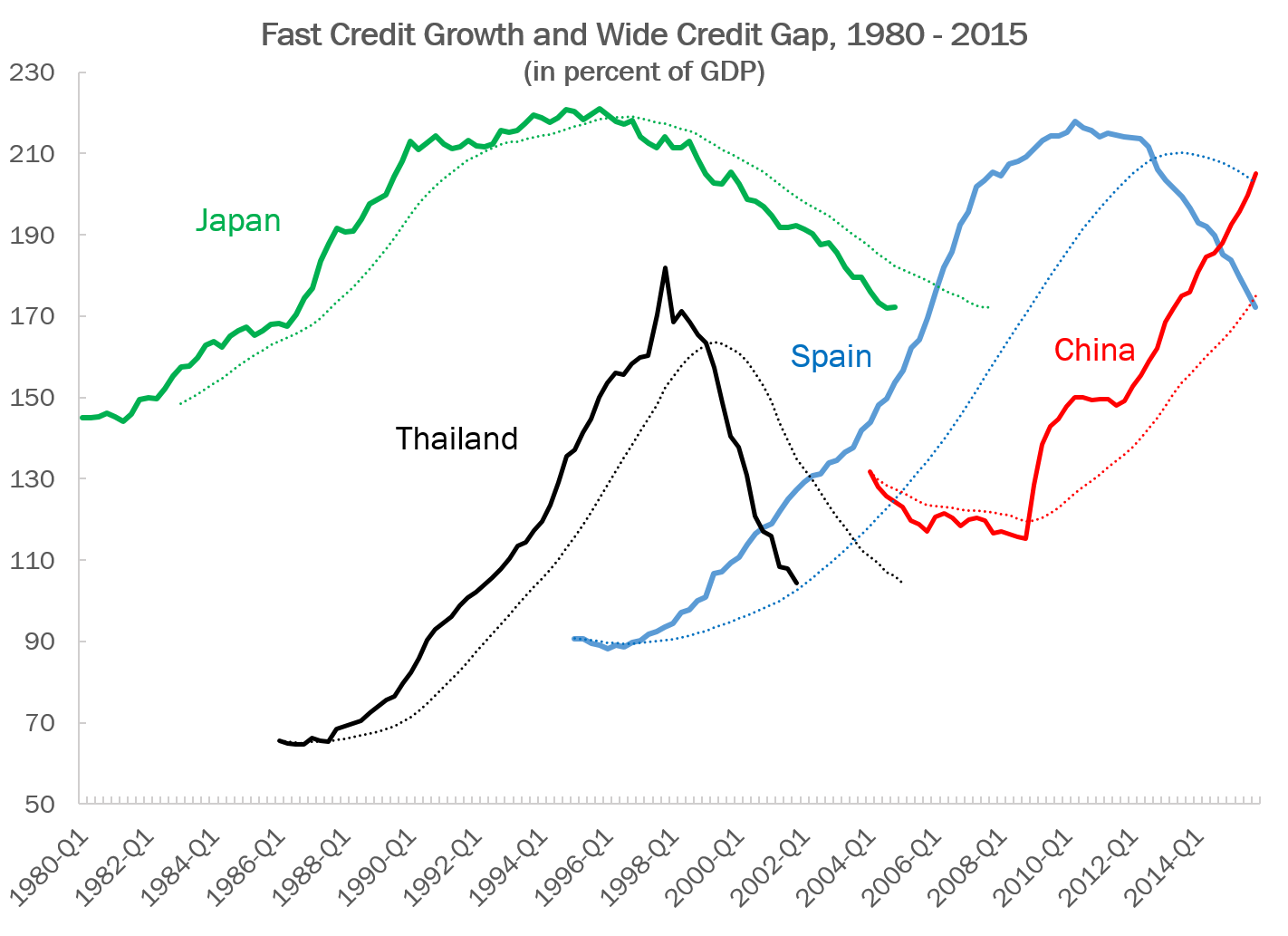

Excessively fast credit growth is a good predictor of financial crises. The Bank for International Settlements (BIS) calculates the “credit gap” as the difference between actual credit growth and trend.

The figure above shows the evolution of the credit gap in China and in a number of previous, well-known cases that ended in financial crisis: Japan in the late 1980s and early 1990s; Thailand in 1997 and 1998; and Spain in 2007 and 2008. The measure here is credit to the private, non-financial sector, both households and corporates. (In China’s case, credit to state enterprises is counted as part of the “private, non-financial sector.”) In the three earlier crises, credit growth ran well ahead of trend for a few years. There was an investment boom that was somewhat different in each case, but with a similar end result: that a lot of poor investments were financed. Eventually, these investments failed to provide sufficient return to service the loans, bad loans became manifest both in banking and in bond defaults, and a financial crisis ensued. One of the key features of these crises is that, as bad loans start to build up, banks are unsure about which clients will fail and tend to restrict lending, even to potentially good clients. That drying up of credit is a key reason that the real impact of these crises is so severe. In each of the previous cases, it can be seen that the crisis is followed by a period of deleveraging in which the stock of credit relative to GDP falls sharply.

In China’s case, the BIS calculates a credit gap of about 30 percentage points of GDP; that is, the actual build-up of the outstanding credit stock is about 30 percentage points of GDP higher than would have been predicted by trend. This is alarming, and Chinese officials have spoken of the need to reduce leverage (most famously, in an unsigned People’s Daily article by an “authoritative person” in May 2016). Yet credit growth continues to grow much faster than the growth of nominal GDP.

While many outside analysts worry about a financial crisis in China, there are reasons to think that it will not take the predictable form. There are some special features of the Chinese financial system. First, this credit growth is domestically financed. China has a very high savings rate, around 50 percent of GDP. So, China does not rely on external financing in any meaningful way. In the earlier crises of Thailand and Spain, their credit booms were largely funded by external capital; as their crises unfolded, capital outflow accelerated their credit contraction. Japan’s case was more similar to contemporary China in that the country’s credit and investment boom was self-financed. A second, related feature of China is that the main backing for credit expansion is household deposits in banks, which tend to be very stable. This is somewhat less true in the past year, as financing from non-bank institutions (shadow banking) has played a big role in credit expansion. The formal banking system primarily consists of state-owned banks lending to state-owned enterprises, including local government investment vehicles. It is hard to see a traditional banking crisis in this sector. Already many state-owned enterprises are in distress and cannot service their loans. But banks continue to lend to them, and it is hard to see households losing confidence in the system and withdrawing their deposits. What is less clear is how the shadow banking system will operate in an incipient crisis. As some of the wealth management products backing shadow lending start to fail, it is possible that households will withdraw significant amounts from these products and that the non-bank lending will contract. But given the state’s role in the financial sector, it seems unlikely that overall financing would contract as in a traditional financial crisis.

While the state’s intervention works against a traditional financial crisis, it creates other problems. There are lots of examples of central and local authorities intervening to keep open state enterprises that are essentially bankrupt. Recently, Chinese authorities announced a new fund, with 350 billion yuan of capital, that would be used to help distressed state firms. The money is coming from state enterprises that are doing well, so the state is essentially taxing the more successful firms to subsidize the unproductive ones. These kinds of measures will keep the average productivity of investment low and contribute to ongoing problems of generating total factor productivity growth. In other words, state interventions may prevent a large, visible financial crisis, but they are likely to lead to continuing slowdown in the growth rate.

Capital outflows on the rise

A second, growing risk concerns China’s exchange rate and capital account. Until recently, China had a current account surplus and a capital account surplus, as foreign direct investment flowed into permitted sectors (mostly manufacturing). The twin surpluses created balance of payments problems for China, since large-scale reserve accumulation was required to prevent rapid appreciation of the Chinese currency. China had pegged its currency to the dollar at a rate of 8.3:1 in 1994, not an unreasonable choice for a developing economy. But by the mid-2000s, productivity growth in China meant the currency was increasingly undervalued. China moved off the peg in 2005.

Over the last decade, China’s effective exchange rate has appreciated more than any other major currency, rising a total of more than 40 percent. The fact that the dollar had no trend between 2006 and 2013 means that the yuan was rising against the dollar during this period. China’s balance of payments situation began to change around 2014. First, the dollar began rising quite sharply against other currencies with an effective appreciation of about 20 percent over a year. Initially, China followed the dollar up, but began to worry that the appreciation was too much, especially if the Federal Reserve was going to raise interest rates. Second, the capital account entered a deficit. With excess capacity in many sectors of China’s economy and declining profitability, China’s capital account began to be dominated by state enterprises going out for investment and private Chinese capital moving some assets abroad. For a short period in 2014, the net capital outflow roughly matched the continuing current account surplus: China’s exchange rate was stable without any significant central bank intervention. But as 2015 began, the net capital outflows accelerated and China started selling reserves in order to prevent the currency from depreciating.

In August 2015, China carried out a “mini-devaluation” that was poorly executed and communicated. The small, discrete devaluation spooked global markets. It was taken as a sign that China’s economy was much weaker than previously thought and as a herald of a new exchange rate policy. Capital outflows accelerated. In a little more than a year, China’s reserve holdings went from $4 trillion to $3 trillion. It’s ironic that U.S. officials continue to call China a currency manipulator when it has been intervening to keep the value of its currency high, not low.

It’s ironic that U.S. officials continue to call China a currency manipulator when it has been intervening to keep the value of its currency high, not low.

Enter: capital controls

Chinese officials have said publicly and privately that they have no intention to devalue the currency to spur exports and that they see no foundation for sustained depreciation of the currency. In terms of fundamentals, they are right that there is no foundation for depreciation. China has a large and rising current account surplus, and its share of global exports hit a new historical high in 2015. Clearly there is no competitiveness problem. Given China’s large trade surplus, any significant depreciation now would be disruptive to the world economy and could well spark trade protection from China’s partners.

The problem that the country faces is that it is still fighting large capital outflows. The national savings rate has come down only slightly from 50 percent of GDP, and it is likely that saving behavior will change only slowly. With diminishing investment opportunities within the country, it makes sense that significant amounts of capital are trying to leave. The reserve loss and the outflow pressure also create a reasonable fear that, whatever authorities say, they may not be able to prevent a large depreciation. That just encourages capital to try to leave sooner.

Related Books

During 2016, the balance of payments stabilized to some extent. Capital outflow pressures were eased by authorities’ clear communication that devaluation wouldn’t happen, as well as the somewhat better data from the real economy and ongoing stimulus of investment. It also seemed that the government tightened up on its capital controls to make moving money more difficult.

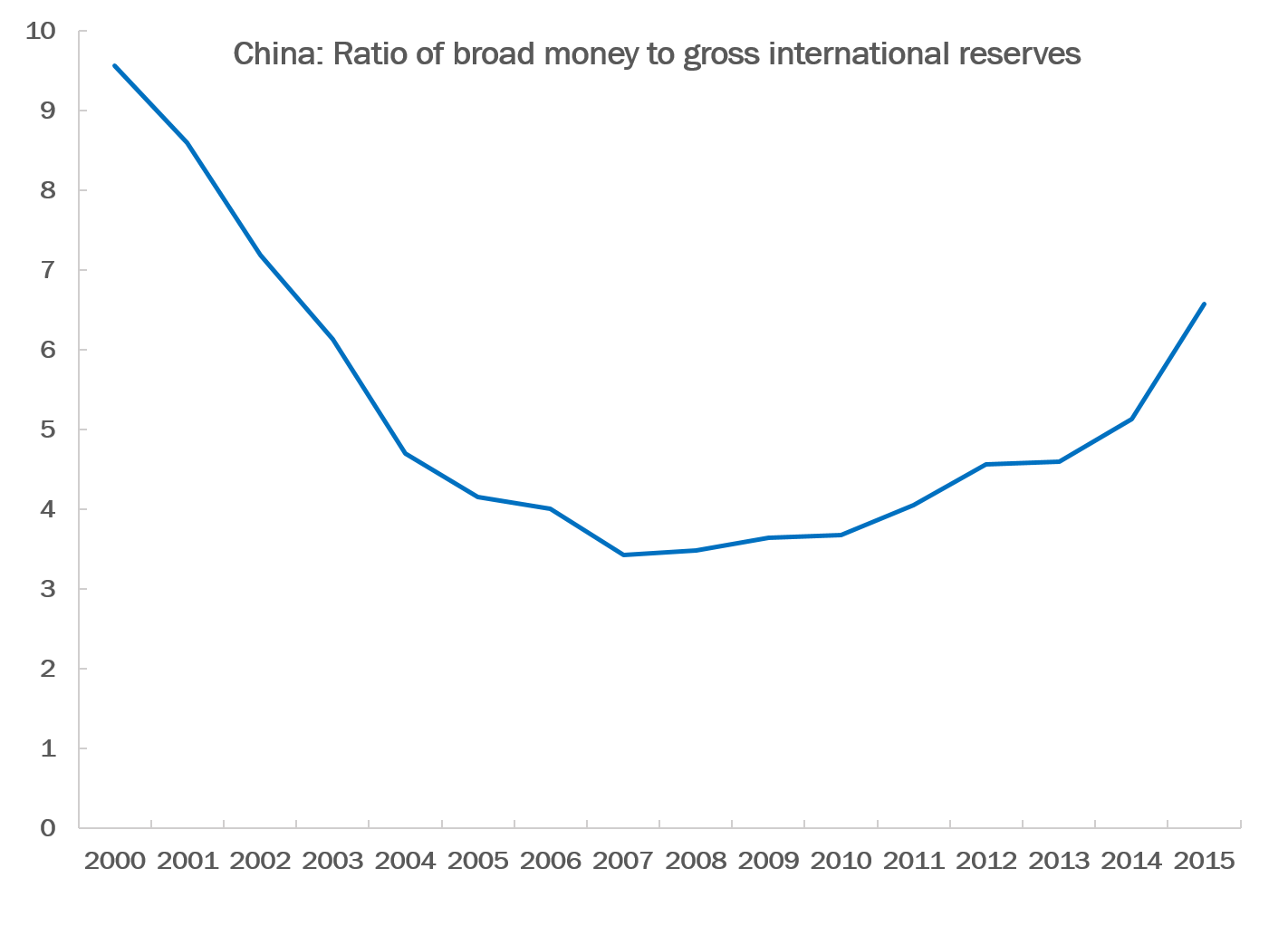

The issue of capital controls is of crucial importance. The IMF considers a ratio of broad money to reserves of 5:1 a warning level for a country with bank-dominated finance and an open capital account. The figure below shows the evolution over time of broad money to reserves for China. The ratio was very high in the early 2000s, but that was when China had extensive capital controls. The ratio came down in the mid-2000s as China built up reserves and as credit growth aligned with nominal GDP. Since 2010, however, there has been an alarming rise in the ratio from below 4 to nearly 7. China would be at risk of a currency crisis if it had an open capital account. Hence, it is no surprise that China has tightened up its capital controls over the past year.

If one accepts that the investment rate needs to come down as part of the control of leverage and in response to diminishing returns, then the savings rate needs to come down as well in order to prevent the capital outflow from expanding to levels that would be destabilizing for China and the world economy. In a subsequent post, I will consider some policy options that could encourage consumption and reduce the national savings rate. In the meantime, China will tighten its capital controls as necessary to maintain control of its exchange rate. Firms are already complaining that it has become harder to move money in and out of the country for normal trade purposes. The micro-management of foreign exchange transactions is analogous to government actions to prevent firms from closing, discussed above; it throws sand in the wheels of normal commerce. China can probably avoid an exchange rate crisis, but it will pay a price in terms of the efficiency and growth of the economy.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

China is struggling to keep its currency high, not low

January 26, 2017