Editor’s Note: On January 29, Joshua Meltzer testified before the United States International Trade Commission on deepening the U.S.-Africa trade and investment relationship.

Introduction

The United States trade relationship with sub-Saharan Africa remains underdeveloped. In fact, U.S. trade with Africa has been declining since 2011. Currently, only approximately 1.5 percent of U.S. exports are to sub-Saharan Africa. At the same time, economic growth in Africa from 2004 to 2014 averaged 5.8 percent, though in 2015 growth was only 3.75 percent, in large part reflecting the decline in commodity prices—a key export for many Africa countries—in response to the slowing growth rates in China. [1]

Robust economic growth rates in sub-Saharan Africa will be key if the continent—where over 40 percent are still living in poverty—is to achieve the Sustainable Development Goals. One important way of supporting African growth and opportunity is through increasing African engagement with the international economy through increased participation in international trade.

U.S.-Africa trade

The African Growth and Opportunity Act (AGOA) underpins U.S. trade with sub-Saharan Africa. AGOA has been extended and reauthorized on four occasions, most recently in 2015 until 2025.

AGOA provides exports from sub-Saharan Africa preferential access to the U.S. market. The U.S. also provided preferential access for sub-Saharan Africa exports under its Generalized System of Preferences (GSP), a program that applies to exports from most developing countries. The GSP expired in 2013, but under AGOA GSP preferences remain available for AGOA-eligible countries. AGOA, combined with the GSP, provides duty-free access to the U.S. for 6,400 product lines from 38 countries in sub-Saharan Africa. Of total U.S. imports from AGOA countries, around 70 percent enter under AGOA.

From 2001 to 2013, exports under AGOA increased from $7.6 billion to $24.8 billion but declined over 50 percent in 2014 to $11.6 billion mainly due to reduced petroleum exports to the U.S. Anecdotal and survey-based evidence has found that African businesses view AGOA as very important for their trade with the U.S.

By enabling increased trade, AGOA supports local businesses and their integration into the global economy. AGOA has also stimulated foreign investment in sub-Saharan Africa, often by companies taking advantage of the new market access opportunities back in the U.S. For instance, U.S. retailers such as Gap, Target, and Old Navy source goods in Africa for export to the U.S.[2]

AGOA is also an important tool for achieving broader U.S. goals such as promoting market reforms and building democracy. These goals are achieved through its role in strengthening growth opportunities in sub-Saharan Africa broadly. In fact, in order for a country to be eligible to receive AGOA’s trade preferences, compliance with the following conditions is necessary:

- The country must be making progress towards a market-based economy, enhanced rule of law, elimination of trade barriers and systems to combat corruption, and the protection of worker’s rights;

- The country must not be engaging in activities that undermine U.S. national security;

- The country must not be engaging in gross violations of human rights.

AGOA-eligible countries in sub-Saharan Africa are making significant economic reforms that are improving their capacity to grow and providing new opportunities to deepen their economic relationship with the U.S. The 2015 World Bank Ease of Doing Business Report found that sub-Saharan Africa accounted for the largest number globally of regulatory reforms that reduced the cost of doing business.[3] Democratic governance is also on the rise in sub-Saharan Africa. According to a Freedom House report, the largest gains in freedom over the last five years have been in sub-Saharan Africa.[4]

Notwithstanding the growth in U.S.-African trade since AGOA, there remains significant scope to increase its depth and range. For instance, Africa exports 10 times as much to Europe as it does to the U.S. The European “equivalent” trade scheme—the “Everything but Arms” initiative—has a higher utilization rate than AGOA and is estimated to have generated almost twice as many exports than AGOA.[5] The conclusion by the European Union of Economic Partnership Agreements with a number of countries in sub-Saharan Africa is also providing enhanced market access.

The composition of U.S.-Africa trade

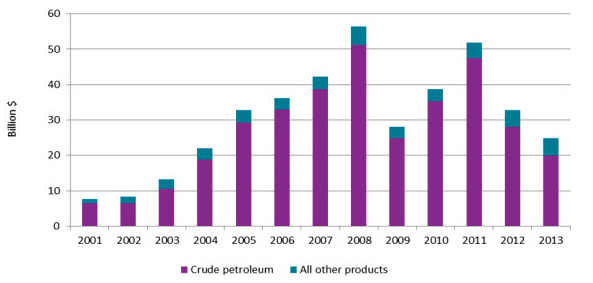

As Figure 1 demonstrates, U.S. trade with Africa is dominated by crude petroleum exports, which account for approximately 90 percent of all U.S.-Africa trade. The impact of AGOA on crude oil exports to the U.S. has been limited as these products were entering the U.S. duty free under the GSP anyway.

Figure 1: U.S. imports under AGOA, 2001-2013

Source: United States International Trade Commission (USITC) DataWeb/USDOC.

Since 2011, exports of crude oil to the U.S. have declined and the most data shows a continuation of this decrease due to increases in the U.S.’ production of oil. Given this trend, failure to grow sub-Saharan Africa’s non-oil exports to the U.S. could see a significant deterioration in the overall economic relationship.

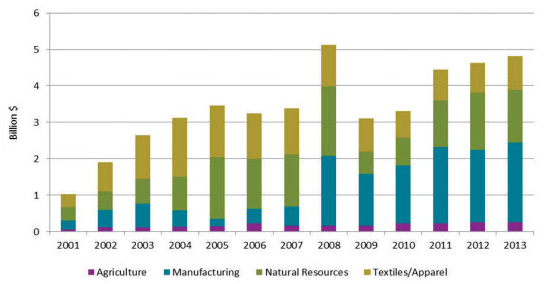

The following graph disaggregates exports to the U.S. other than crude oil. Growth here has been significant, from around $1 billion in 2001 to over $4.7 billion in 2013, peaking at over $5 billion in 2008 just prior to the financial crisis.

Figure 2: U.S. imports under AGOA, excluding crude petroleum, 2001-2013

Source: USITC DataWeb/USDOC.

Note: “Agriculture” includes all agricultural products; “manufacturing” includes electronics, machinery, transportation equipment, chemicals, miscellaneous manufacturing, and special provisions items; “natural resources” includes energy products (except crude petroleum), minerals and metals, and forest products; and “textiles/apparel” includes textiles, apparel, and footwear.

As Figure 2 shows, the most significant impacts of AGOA on non-petroleum exports have been in apparel, which grew over 250 percent from $355 million in 2001 to over $907 million in 2013. Exports of apparel are also, however, down from their peak of $1.13 billion in 2008 as cost-competitive apparel manufacturers in East Asia have gained market access in the U.S. This trend has been due to the phase out of the World Trade Organization (WTO) Multi-fiber Agreement in 2005, which capped exports of textile and apparel, as well as the phase out of other restrictions on textile exports from China under its WTO accession agreement.

On the manufactured goods side, the growth in manufacturing exports has also been very significant and is accounted for almost entirely by growth in motor vehicle exports.

Agriculture exports to the U.S. have grown significantly since AGOA, from $59 million in 2001 to $261 million in 2014. The main exports of agriculture products to the U.S. are cocoa paste and powder, citrus fruits, edible nuts, wine, unmanufactured tobacco, and vegetables. As noted above, despite this increase in agriculture goods, exports trade remains small in absolute terms.

Notwithstanding the growth in sub-Saharan Africa agriculture exports to the U.S., as a share of non-oil exports to the U.S. under AGOA, agriculture has declined from 6.2 percent in 2001 to 2.2 percent in 2014. Yet this is true for all non-oil exports (except for motor vehicles) from sub-Saharan Africa to the U.S., whose export shares have also declined despite increased exports, reflecting the growth during this period of crude oil exports to the U.S.

Growing U.S. trade with sub-Saharan Africa

There is much room for growth in U.S.-Africa trade. One area that needs attention is the expanding trade in agricultural goods. Current agriculture exports to the U.S. are less than 3 percent of total exports under AGOA. Expanding opportunities for sub-Saharan African agriculture exports to the U.S. will produce a range of benefits:

- It will help drive growth and employment in the agriculture sector in sub-Saharan Africa, which is responsible for 30 percent of GDP and 70 percent of employment. This growth will also create employment opportunities for woman, as they comprise about 50 percent of the agriculture labor force in the region;

- The labor intensity of agriculture in sub-Saharan Africa means that policies to promote growth in the agriculture sector will be most effective at reducing poverty[6]

- Growth in the agriculture sector will help address growing youth unemployment in sub-Saharan Africa.[7] This is particularly important given sub-Saharan Africa’s so-called youth bulge, in which increasing numbers of young people are entering the job market this decade.[8]

Growth in trade in manufactured goods and services are other potential growth areas. Making progress here should including supporting the capacity of African businesses to engage in digital trade—to sell goods and services online to customers in the U.S. and globally. This would include support to increase access to the Internet—where growth is mainly in the mobile sector—as well as developing the rules, regulations, and institutions that can enable digital trade to flourish. This would include:

- Building greater understanding of the need for data flows for digital trade;

- Improving logistics and customs processes (including by ratifying the WTO Trade Facilitation Agreement);

- Increasing access to online payment mechanisms;

- Regulatory developments to increase trust by consumers and business in purchasing goods and services online from African businesses.[9]

Making progress here will diversify U.S. trade with sub-Saharan Africa, which is currently dominated by oil and gas exports.

AGOA itself provides various mechanisms for developing strategies to expand trade in manufactured products. Of significance is the requirement in AGOA for African governments to develop “AGOA utilization strategies” for increasing exports by AGOA-eligible countries of manufactured goods. The Office of the United States Trade Representative (USTR) is required to post such strategies on its website. AGOA also calls on USTR to assess the prospect of a free trade agreement (FTA) with Africa.

A changing international trading environment

Any consideration of how to expand U.S.-African trade needs to consider the changing international trading environment being created by the focus of the U.S. on large FTAs, the most important being conclusion in October 2015 of the Trans Pacific Partnership (TPP) agreement. Comprising 12 countries including the United States, Japan, Canada, Mexico, Australia, Vietnam, Malaysia, and Chile, TPP countries represent 40 percent of global GDP, 25 percent of global exports, and 30 percent of global imports.

The U.S. is also negotiating with the European Union the Transatlantic Trade and Investment Partnership (TTIP) agreement, which, combined with the TPP, will cover nearly 60 percent of global GDP. The effect of two such significant FTAs is that their rules will become de facto global standards. Moreover, the U.S., the EU, Japan, and 21 other countries are negotiating the Trade in Services agreement—an FTA focused on liberalizing barriers to trade in services. Finally, the Association of Southeast Asian Nations (ASEAN) plus China, Japan, Korea, India, Australia, and New Zealand are negotiating the Regional Comprehensive Economic Partnership agreement.

Africa is not a party to any of these mega-regional trade negotiations. At the same time, little progress is being achieved on completing the WTO Doha Round multilateral trade negotiations. This means that there is currently no large global trade negotiation where Africa’s views can be considered and progress can be made. The risk for Africa in this is that new rules and market access preferences agreed under the mega-regional FTAs will make it increasingly difficult for African businesses to compete globally, confining Africa to a shrinking share of international trade and diminishing its attractiveness as a destination for investment

African trade initiatives

At the same time, Africa is also embarking on an ambitious program of trade integration. In 2008, negotiations commenced on the Tripartite FTA (TFTA) between three major regional African economic communities. The TFTA is expected to come into force in early 2016 and ultimately will comprise 26 countries, 640 million people, and have a total GDP of $1.2 trillion. So far, however, the proposed TFTA only covers trade in goods.

The TFTA is also the building block towards a Continental FTA (CFTA). The Africa Union has committed to completing the CFTA by 2017, incorporating 54 African countries representing over 1 billion people and $3 trillion in GDP. In fact, successfully finishing the CFTA could stimulate intra-African trade by around 50 percent ($35 billion) by 2022.

Any efforts to expand and broaden U.S. trade with Africa needs to consider how the TPP in particular will affect the competiveness of African exports into the U.S. The TFTA and potential CFTA also demonstrate a continent-wide appreciation of the need to make progress on trade liberalization. This trade-liberalizing energy by African governments should be encouraged and where opportunities exist, supported by the U.S.

These African trade negotiations also provide opportunities for the U.S. to help ensure that the process builds towards, a set of rules and market access opportunities that is consistent with and builds bridges between, Africa and other U.S.-led trade initiatives such as the TPP. This could include working to develop the capacity of African standards organizations, making progress on 21st century issues such as digital trade and improving understanding within Africa of the TPP’s trade and labor standards.

In parallel, the WTO should remain a focus for U.S. and Africa trade negotiations. The fact is that the WTO Doha Round is dead, a reality confirmed at the recent WTO Ministerial meeting in Nairobi, in December 2015, where the U.S. and other developed country members refused to reaffirm the Doha mandates. At the same time progress was made in Nairobi on issues of importance to African countries, such as on preferential treatment of service suppliers from least-developed countries (LDCs), including extension of the waiver for granting preferences to LDC services exports and further steps such as technical assistance.[10]

Growing sub-Saharan Africa’s exports of agriculture products

Going forward, a U.S.-Africa trade relationship based solely on unilateral preferences is no longer a sufficient basis for building more robust trade relations. Progress in expanding trade in manufactured goods, services, and digital trade more broadly is needed.

In the short term and for the reasons outlined above, expanding access for agriculture exports from sub-Sahara countries is something that would deliver immediate growth and support development outcomes. The following outlines specific measures that the U.S. government should consider:

Reduce to zero all tariffs on agriculture exports from AGOA-eligible countries: Most agriculture exports from sub-Saharan Africa already enter the U.S. tariff-free. There are, however, a number of products where the U.S. retains high tariffs, such as sugar and cotton, and that, if reduced, would stimulate further trade. According to one study, complete elimination of tariffs on agriculture exports from sub-Saharan Africa would increase exports over $105 million compared to what it would otherwise be in 2025, with large gains in areas such as sugar and fish exports. Moreover, the impact of removing all tariffs would only reduce U.S. production by $9.6 million.[11]

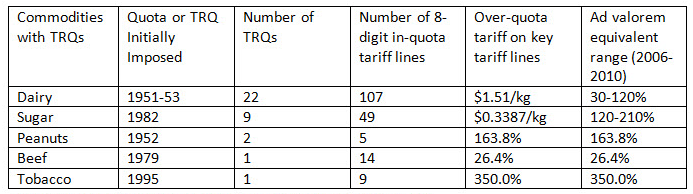

Eliminate quotas on agriculture exports from AGOA-eligible countries; or at least from those countries in sub-Saharan Africa that LDCs. This move would be consistent with U.S. obligations under the U.N. Millennium Development Goals and would fulfill a key demand from these countries in the WTO Doha Round negotiations. Tariff rate quotas (TRQs) are another area where significant trade barriers remain for agriculture exports from sub-Saharan Africa to the U.S. A TRQ is a lower-level tariff for a specific volume of imports over a given period and a higher tariff for import volumes over the quota. The U.S. maintains 46 TRQs on seven commodities: sugar, tobacco, dairy, beef, peanuts, cotton, and green olives.

Except for imports of sugar and cotton, imports under AGOA that are in-quota enter the U.S. at zero tariffs. The following table lists U.S. TRQs on the main agriculture commodities of export interest for sub-Saharan Africa.

Table 1: U.S. tariff rate quotas

Source: International Food and Agriculture Trade Policy Council

As this table shows, over-quota tariffs on exports of agriculture products from sub-Saharan Africa are high, ranging from 26 percent for beef to 350 percent for tobacco imports. These rates make exports of over-quota agriculture products uncompetitive in the U.S. As a result, access to quotas is key to growing agriculture exports.

The share of in-quota TRQs allocated to AGOA-eligible countries is very low. This is because the allocation of quotas among U.S. trading partners reflects historical trading patterns and quota access deals under U.S. FTAs. The lack of access to quotas locks out African agriculture producers from U.S. markets.

U.S. quotas on agriculture exports exist on a range of products that African producers already export to Europe and where their revealed comparative advantage suggests that they could successfully export to the U.S. if access to quotas was expanded. This would include goods such as dairy products, sugar, peanuts, and beef (assuming sanitary and phytosanitary (SPS) issues are overcome—see below).

There are a number of ways that the lack of access to quotas can be addressed. Some reallocation of quotas can be done by the administration. However, the scope for action depends on U.S. commitments in its FTAs and at the WTO. In other cases, quotas on particular agriculture exports are not fulfilled each year, but there is no mechanism that would allocate these quotas to countries that are AGOA-eligible. A number of agriculture imports into the U.S. also have an “other” category for quotas allocated on a first-come, first-served basis, which could be reserved for AGOA-eligible countries.

Assist African countries in complying with U.S. SPS requirements: In order to enable African exporters to maximize the opportunities under AGOA, U.S. SPS requirements raise the cost of African exports, at times enough to offset any additional competiveness gained through lower tariffs. Progress here would not mean lowering U.S. SPS standards, but instead working with African governments and producers to help them meet U.S. standards.

References

[1] Sy, A. “Managing Economic Shocks: African Prospects in the Evolving External Environment”, Foresight Africa 2015, Africa Growth Initiative, Brookings Institution.

[2] Schneidman, W. (2012), “The African Growth and Opportunity Act: Looking Back, Looking Forward”, Africa Growth Initiative, Brookings Institution, July 2012.

[3] World Bank Doing Business 2015: Going Beyond Efficiency, World Bank 2014.

[4] Freedom in the World 2015, Freedom House.

[5] E. Davies and L. Nilsson (2013), “A Comparative Analysis of EU and US Trade Preferences for the LDCs and the AGOA Beneficiaries”, European Commission Chief Economist Note, Ref Ares(2013)157432 – 07/02/2013.

[6] Loayza, N. and D. Raddatz (2006),” The Composition of Growth Matters for Poverty Alleviation”, World Bank Policy Research Paper 4077.

[7] Filmer, D. et al. (2014) “Agriculture as a Sector of Opportunity for Young Africans”, in Youth Employment in Sub-Saharan Africa (Vol. 2): Full Report (World Bank Group 2014).

[8] Agbor J., Olumide. T, and Jessica Smith, Saharan Africa’s Youth Bulge: A Demographic Dividend or Disaster? in Foresight Africa 2012, Brookings Press 2012 .

[9] Meltzer, Joshua P. 2016 “Maximizing the Opportunities of the Internet for International Trade” E15 Expert Group on the Digital Economy – Policy Options Paper. E15Initiative. Geneva: International Center for Trade and Sustainable Development ad World Economic Forum.

[10] WTO Ministerial Conference, Nairobi, “Implementation of Preferential Treatment in Favour of Services and Service Suppliers of Least Developed Countries and Increasing LDC Participation in Services Trade”, WT/MIN(15)/48, 21 December 2015.

[11] Mevel, S., et al (2013), “The African Growth and Opportunity Act: An Empirical Analysis of the Possibilities Post-2015”, Economic Commission for Africa and Brookings 2013.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

TestimonyDeepening the United States-Africa trade and investment relationship

January 28, 2016