This analysis is part of The Leonard D. Schaeffer Initiative for Innovation in Health Policy, which is a partnership between the Center for Health Policy at Brookings and the USC Schaeffer Center for Health Policy & Economics. The Initiative aims to inform the national health care debate with rigorous, evidence-based analysis leading to practical recommendations using the collaborative strengths of USC and Brookings.

Late Monday night, House Republican leaders unveiled a “manager’s amendment” that makes several changes to the American Health Care Act (AHCA). The House is currently scheduled to vote on an amended version of the AHCA sometime on Thursday.

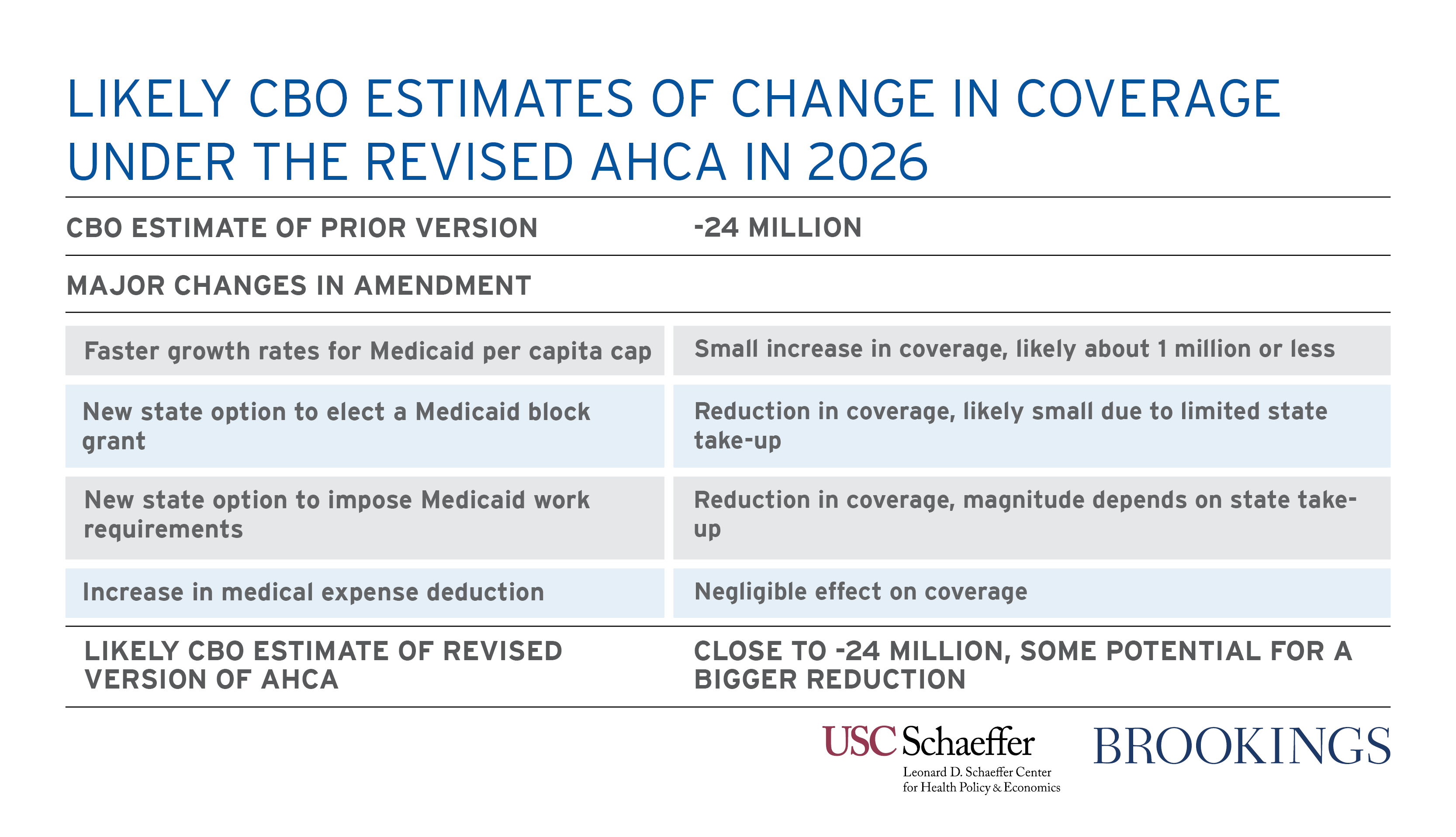

It remains unclear whether a Congressional Budget Office (CBO) score of the revised legislation will be available before the House vote, and a score is very unlikely to be available before the bill’s markup in the House Rules Committee. In this analysis, we use CBO’s score of the earlier version of the AHCA as well as other CBO analyses to assess how the changes made in the manager’s amendment are likely to change CBO’s estimates of the effect of the AHCA on health insurance coverage.

We conclude that the changes made by the manager’s amendment will not meaningfully alter CBO’s earlier prediction that the AHCA would substantially reduce insurance coverage. While one provision of the manager’s amendment would slightly relax the “per capita cap” on state Medicaid spending created under the AHCA and thereby modestly increase CBO’s estimate of insurance coverage under the AHCA, the work requirement and block grant options created by the manager’s amendment have the potential to cause additional coverage losses that largely or more than offset this improvement, at least if states take up these options.

The change to the medical expense deduction in the manager’s amendment is likely to have a negligible effect on CBO’s coverage estimates. Some reports have suggested that this provision was inserted as a placeholder and that the intent of Republican leaders is for the Senate to remove this provision and use the savings—roughly $75 billion over ten years—to increase individual market tax credits for older enrollees in some unspecified way. Naturally, unspecified future changes will not be incorporated in CBO’s analysis of the current version of the legislation. However, given the relatively limited amount of money involved, we conclude that future changes along these lines would be likely to only marginally increase CBO’s estimate of the level of insurance coverage under the AHCA.

In light of the considerations discussed above, we expect that CBO’s updated estimate of the reduction in insurance coverage under the revised AHCA in 2026 is unlikely to be much below its prior estimate of 24 million, and it is possible that its revised estimate could be somewhat higher. The remainder of this analysis examines each of the major modifications made by the manager’s amendment in greater detail. The table below summarizes our conclusions regarding each major provision.

Higher Annual Growth Rate for Certain Populations Under the Medicaid Per Capita Cap

The AHCA would impose a “per capita cap” on state Medicaid programs starting in fiscal year 2020. This proposal set a spending target for each beneficiary the state enrolled in its Medicaid program. Different targets would be set for each of five categories of beneficiaries (elderly beneficiaries, disabled beneficiaries, children, ACA expansion enrollees, and other adults), with the level of the target based on the state’s per enrollee spending for that group in fiscal year 2016. If a state’s total spending across all beneficiaries exceeded the total of the target amounts across all of its enrollees, the excess would not be eligible for federal matching funds. Under current law, federal matching funds cover 57 percent of spending, on average, for most categories of Medicaid enrollees.

The manager’s amendment changes how the per enrollee spending targets are updated over time. Under the prior version of the AHCA, the spending targets for all five beneficiary categories would have been updated based on the annual growth in the Consumer Price Index for Medical Care (CPI-M). The manager’s amendment would increase this growth rate to CPI-M plus one percentage point for elderly beneficiaries and disabled beneficiaries. Because spending for elderly and disabled beneficiaries accounts for more than half of total Medicaid spending, this change somewhat lessens the stringency of the per capita cap.

We expect that CBO’s updated estimate of the reduction in insurance coverage under the revised AHCA in 2026 is unlikely to be much below its prior estimate of 24 million, and it is possible that its revised estimate could be somewhat higher.

However, this modification is likely to only modestly affect CBO’s estimates of how many people would have insurance coverage under the AHCA. Of the overall 14 million person reduction in Medicaid coverage CBO projected under the prior version of the AHCA in 2026, more than 9 million can be accounted for by CBO’s estimate that fewer states would be operating Medicaid expansions and at least a couple million more can be accounted for by elimination of the individual mandate.[1] Furthermore, our rough estimate is that the indexing change would reduce the overall impact of the per capita cap by only around one-third. Putting this all together implies that the change to the per capita cap is unlikely to reduce CBO’s estimate of the coverage losses under the AHCA by much more than 1 million, and the effect could be smaller.

New State Option to Elect a Medicaid Block Grant Instead of a Per Capita Cap

As an alternative to the per capita cap structure discussed above, the manager’s amendment would allow states to elect to receive a block grant: a fixed aggregate payment from the federal government for the coverage of certain Medicaid populations in lieu of ordinary federal matching funding. States could elect to receive a block grant for children and non-expansion adult enrollees, but not for elderly, disabled, or expansion enrollees. The block grant option would start in 2020, the same year as the per capita cap.

Related Books

In the first year the block grant is available, the block grant would equal the federal allotment a state would have received for the relevant population under the per capita cap (that is, the state’s aggregate federal matching funding for the elected population in fiscal year 2016, adjusted for changes in enrollment and growth in the CPI-M through 2019). After its first year, the block grant amount would grow only with the change in the overall Consumer Price Index, a slower rate than the CPI-M, and without any adjustment for population growth or other sources of enrollment growth. States choosing the block grant option would also have wider flexibility to set eligibility rules and the scope of services covered under its Medicaid program than under current law.

In states that selected the block grant option, CBO would likely project substantial reductions in Medicaid enrollment since these states would have much stronger incentives to reduce enrollment than under a per capita cap. Under a block grant, a state that reduces Medicaid enrollment captures all of the resulting cost savings. By contrast, under a per capita cap, a state that reduced Medicaid enrollment captures—at most—part of those savings since reducing enrollment tightens its overall spending cap.

However, it is doubtful that CBO will expect many states to elect this new option.[2] Because the block grant amount would grow much more slowly than the matching funds received under the per capita cap proposal, states choosing the block grant option would generally receive much less federal funding under the block grant option than under the per capita cap (with the exception of states that wish to dramatically reduce Medicaid enrollment). This would tend to cause relatively few states to choose this option, particularly since they would be required to commit to the block grant option for a 10-year period.

In summary, if CBO expects any states to take up this option, it is clear that CBO will expect this provision to reduce insurance coverage. However, since we expect CBO to project relatively limited take-up, we expect that magnitude of any reduction in insurance coverage to be relatively small.

New State Option to Impose Work Requirements on Medicaid Beneficiaries

The manager’s amendment would also allow states to impose “work requirements” in their Medicaid programs starting in fiscal year 2018. Under this provision, states would be permitted to bar non-disabled, non-elderly adults who are not working or engaged in work-related activities from enrolling in Medicaid, with certain exceptions. Work requirements currently exist in some other federal programs, notably the Temporary Assistance for Needy Families program, but are not currently permitted in Medicaid.

Because some states have expressed interest in imposing such requirements in the past, CBO is likely to expect that some states would adopt this option. In those states, CBO seems likely conclude that the requirement will reduce insurance coverage, for two reasons. First, although it appears that the substantial majority of current Medicaid beneficiaries would satisfy such a requirement, some beneficiaries likely would not. Second, and potentially more important, some individuals who do satisfy the requirement might fail to adequately document that fact and lose eligibility as a result.

CBO is thus likely to expect that this provision reduces insurance coverage. CBO will likely expect only a minority of states to adopt such a requirement and that only a fraction of individuals in states imposing work requirements will lose coverage. Nevertheless, with about 20 million non-disabled adults projected to be enrolled in Medicaid in 2026 (after accounting for reductions in Medicaid enrollment attributable to AHCA’s other provisions), meaningful coverage losses from this provision are possible.

Expanding the Medical Expense Deduction

The manager’s amendment would also expand the medical expense deduction, which allows tax filers to deduct a portion of their medical spending (including premiums, cost sharing, and other expenses) from their income for income tax purposes. Under current law, the deduction applies to expenses in excess of 10 percent of adjusted gross income (AGI). The prior draft of the AHCA reduced this threshold to 7.5 percent of AGI, where it stood before the ACA. The manager’s amendment reduces the threshold to 5.8 percent of AGI.

While this policy will have a significant fiscal cost—the cost relative to the prior version of the AHCA has been rumored at around $75 billion over ten years—it is unlikely to have a meaningful effect on CBO’s health insurance coverage estimates. Taxpayers can only benefit from this deduction if they itemize deductions on their tax returns and have taxable income left after taking their other deductions. Furthermore, like all tax deductions, the value of the deduction for those who can benefit from it at all is larger for people in higher income tax brackets. This fact means that the benefits of expanding the medical expense deduction overwhelmingly flow toward higher income households. Indeed, when the Tax Policy Center analyzed the expansion of the medical expense deduction that was included in the prior version of the AHCA, it concluded that over 80 percent of the benefits of this expansion would flow to the top 40 percent of households, with essentially no benefit accruing to the bottom 40 percent of households.

Since coverage rates are already quite high at these income levels and, closely related, CBO generally assumes that the coverage decisions are not particularly responsive to additional subsidies for people in this income range, it seems doubtful that this expansion will have a meaningful effect on CBO’s coverage estimates. Consistent with this, CBO does not appear to have assigned any coverage benefit to the expansion of the medical expense deduction included in the prior version of the AHCA and did not even categorize this provision as one of the AHCA’s “coverage provisions.” It therefore seems safe to assume that the expansion of this deduction will also have a negligible effect on CBO’s estimates.

Some reports have suggested that this provision is merely a placeholder that the Senate will swap out for an expansion of tax credits for older enrollees. While not relevant to CBO’s analysis of this legislation, such a swap could, in principle, help reduce CBO’s estimates of the coverage losses under the AHCA. However, repurposing the estimated $75 billion devoted to this provision would only be sufficient to offset around one-quarter of the $312 billion overall reduction in individual market subsidies under the under the prior version of the AHCA, so this funding would go only a small way toward addressing reductions in the generosity of subsidies available to those purchasing individual market coverage under the AHCA. Furthermore, a significant majority of the AHCA’s coverage losses are attributable to the combination of its Medicaid provisions and the repeal of the individual mandate, and restoring a portion of the reduction in individual market subsidies would do nothing to address these other sources of coverage losses.

Conclusion

The changes to the AHCA included in the manager’s amendment unveiled on Monday night will not meaningfully change CBO’s conclusion that the AHCA will cause large reductions in insurance coverage. While the slight relaxation of the AHCA’s Medicaid per capita cap in the manager’s amendment will modestly reduce coverage losses, the other changes to Medicaid in the manager’s amendment have the potential to cause additional coverage losses. On net, CBO is likely to put the reduction in insurance coverage under the amended version of the AHCA at level similar to or even somewhat higher than its prior estimate that 24 million people would lose insurance coverage in 2026.

[1] CBO’s prior estimate reported that Medicaid expansion states would encompass only 30 percent of the expansion-eligible population under the AHCA in 2026, compared to 80 percent under current law. CBO’s March 2016 baseline projected that there would be 15 million total expansion enrollees in 2026, so this reduction in the prevalence of Medicaid expansion corresponds to an enrollment reduction of 9.4 million.

[2] CBO published a letter last week predicting that some states would opt for a block grant option if it were offered. However, CBO’s letter appeared to contemplate a block grant that would be far more generous to states that the one included in the manager’s amendment, so the relevance of CBO’s prior statements is likely limited.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The House GOP amended its health care bill, but CBO estimates of coverage losses are not likely to meaningfully improve

March 21, 2017