It’s been well documented that assets such as cash savings or real estate are essential to economic mobility. They provide a cushion in emergencies and allow people to become homeowners, start businesses, and pursue advanced education. Yet one in four families with low-incomes do not have the assets needed to cover even three months of basic living expenses without income.

For these families, the opportunity to build assets is out of reach, as anti-poverty programs often discourage or penalize savings—a symptom of the systemic and historic barriers that have long prevented Black, Latino or Hispanic, and multi-racial families from building wealth.

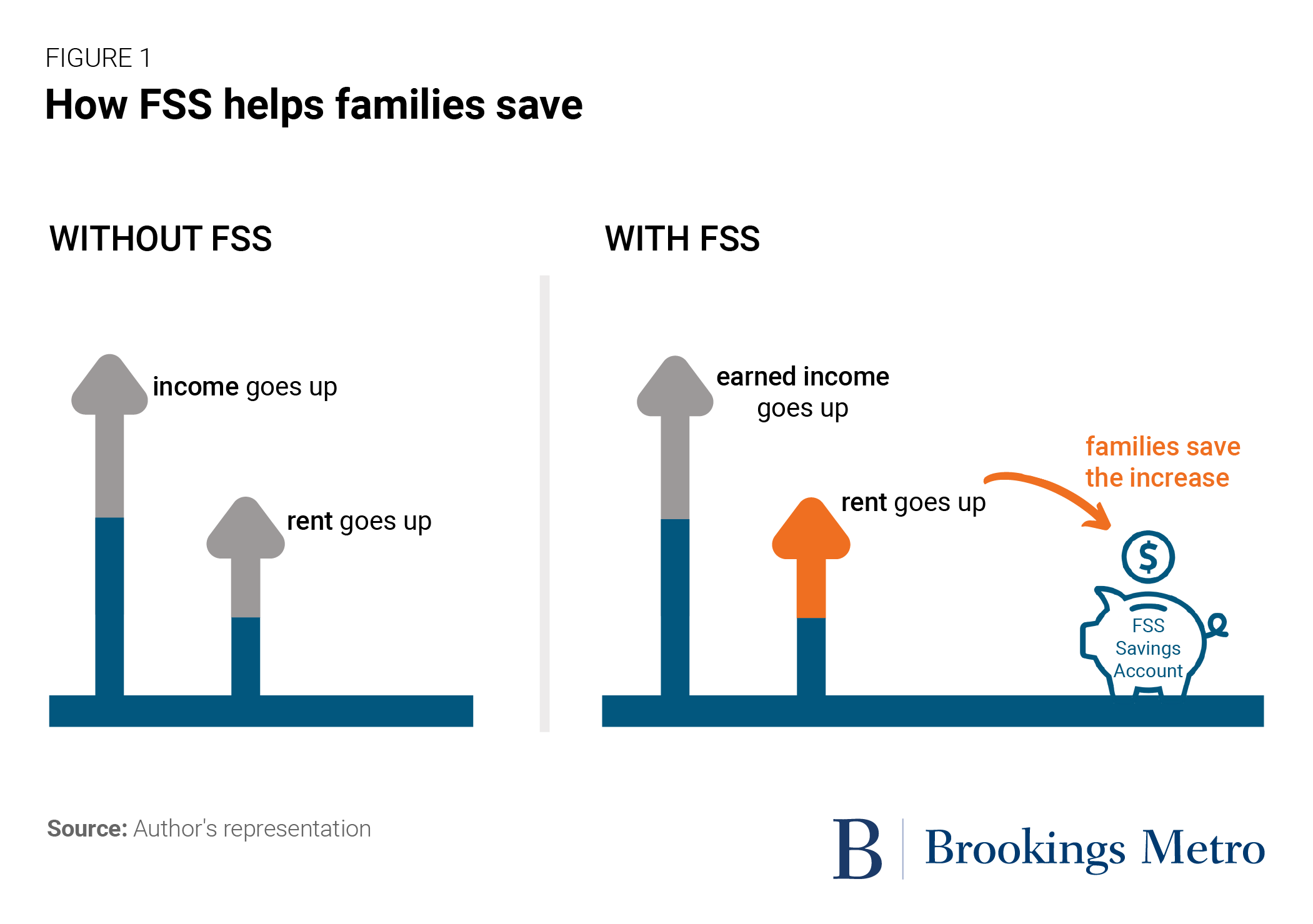

However, there’s an underutilized federal program with tremendous potential to change this for millions of families: the Department of Housing and Urban Development’s (HUD) Family Self-Sufficiency (FSS) program. FSS is a savings incentive program for families living in HUD-assisted housing that enables participants to save a portion of their rent payment when they earn more money at work.

How affordable housing can prevent families from building savings

In some types of HUD-assisted housing, a household’s rent is based on income. Therefore, if a household earns more money, their rent increases proportionately. Although designed to keep housing affordable, this structure can discourage families from increasing their income, since they would pay more in rent and potentially lose other benefits with income limits, such as the Supplemental Nutrition Assistance Program (SNAP).

This rent calculation effectively functions as a marginal tax on increased earnings, which also makes it difficult to build savings. But when households enroll in FSS, if their rent increases because they earn more money at work, the non-utilized portion of their previous housing subsidy goes into a savings account. These savings build over time, and once participants “graduate” from the program, they can put the money to use for financial goals such as buying a home, going to college, or improving their credit. To graduate from FSS, participants must demonstrate progress toward those goals, participants must be working, and no adults in the household can be receiving cash welfare assistance at the time of graduation.

Although FSS was established in 1990, only 3% of the estimated 2.2 million eligible households currently participate. In other words, there is a large, untapped pool of federal funds that could help close the asset gap for lower-income Americans. Barriers to enrollment include limited resources for marketing and program administration as well as residents’ concern that the program seems “too good to be true.”

An asset-building model proven to help families save thousands of dollars

But it’s not too good to be true. My organization, Compass Working Capital, has spent over a decade proving just that. Since 2010, our financial services nonprofit has partnered with housing providers to run the FSS program for residents.

To date, Compass has helped nearly 4,500 families build over $12.5 million in savings through FSS. These are families that have gone on to start businesses, buy homes, and save for their children’s future. A 2021 study of our FSS programs by Abt Associates found that participants earned more and received less public assistance than comparable households not enrolled in FSS. On average, participants graduate with over $8,000 in savings—proving that well-run FSS programs can set families on the pathway to financial stability.

Expanding access to FSS through an opt-out model

HUD has recently implemented new rules for FSS to improve families’ abilities to build savings by easing some graduation requirements and increasing the length of the program. But we need more creative policy measures to make meaningful strides toward closing the participation gap.

Compass advocates for an opt-out model for FSS, which would enable households to automatically build rent-based savings without navigating time-intensive and potentially discouraging upfront enrollment requirements. An opt-out model could also decrease administrative costs related to marketing, enrollment, program management, and service provision. Compass partnered with the Cambridge, Mass. Housing Authority to pilot an opt-out model called Rent-to-Save in two public housing properties. Both properties saw significantly higher FSS participation rates (51.4% and 82.3%), indicating that opt-out models are successful in expanding program access.

An opt-out model holds promise for scaling the FSS program to reach the more than 2 million households nationally that could participate. And, because about half of all HUD-assisted households are headed by Black, Latino or Hispanic, and multi-racial women, FSS is a tool could help narrow racial and gender wealth divides.

The next step: securing permission from HUD to build more expansive opt-out pilots that demonstrate the model’s potential at a greater scale. This would be a step toward a broader vision—when the opportunity to build assets is the norm, and not the exception, in our nation’s anti-poverty work.

Authors

Commentary

Helping renters build assets and move out of poverty by scaling HUD’s best kept secret

January 9, 2023