The COVID-19 pandemic is a difficult environment for tax administrators. On the one hand, they need to show understanding of the difficult circumstances faced by many taxpayers. On the other hand, strengthening tax compliance becomes even more important during a crisis. Just as the economic base is collapsing, additional funding is needed for economic support packages to help those most heavily affected by the pandemic. A commitment toward strengthening public finances can persuade investors to finance rising public debt. It is only fair that all taxpayers show solidarity and share in the burden of fighting the crisis.

In this context, a key question facing tax administrators is how to communicate with taxpayers. Many studies have shown that targeted letters, emails, and text messages sent to taxpayers can lead to more truthful tax declarations and more timely tax payments. But what about during the current pandemic? Are taxpayers still responsive to such communications? Can messages encourage tax compliance? What type of messaging works best in the context of the crisis?

A recent taxpayer communications pilot in Albania offers new insights. In fall 2019, the Albanian tax administration started a new initiative to leverage behavioral insights and rigorous impact evaluations to identify what works on the ground in the Albanian context. In doing so, Albania’s tax administration joined the 202 institutions worldwide that the OECD has identified as already applying behavioral insights to inform the design of public policies. As a first step, the Albanian tax administration designed a randomized controlled trial (RCT) to test the effectiveness of taxpayer communication “nudges” in tackling the under-declaration of worker salaries in monthly payrolls submitted by businesses to the tax authority.

For this impact evaluation, the tax administration selected a sample of businesses suspected of under-declaring monthly payrolls in key occupations. It then designed letters with two different types of messages to be sent to the firms. The first message highlighted the public goods nature of truthful payroll declarations. The second message emphasized the threat of enforcement actions if caught committing tax fraud. Both letter types were designed using behavioral insights to improve readability (e.g., by including clear calls to action in the letter headers and eliminating technical language). The pilot then randomly assigned firms into three groups: a treatment group receiving the letter with a public goods message, a treatment group receiving an enforcement message, and a control group not receiving any letter.

Table 1. Letters on firm payroll declarations

In the pilot, letters addressed to employers emphasized either (i) the public goods nature of truthful tax declarations or (ii) enforcement action in case of noncompliance.

| Treatment letter emphasizing the public goods nature of tax compliance | “You should know that undeclared wages for your employees are detrimental to their well-being: this deprives them of future retirement, of the health and unemployment benefits they have earned through their work, while reducing the quality of public services that benefit your business, family and community. As taxpayers of this country, we have the responsibility and civic obligation to meet our tax obligations.” |

| Treatment letter emphasizing enforcement action | “The tax administration constantly verifies wages, comparing what is declared by employers with the wages found in the market. We would like to inform you that the tax administration will continue to monitor the declaration of your salaries and will address the irregularities by applying the sanctions provided by law. Please take action as soon as possible to correct the payroll declaration, as we will also monitor your response to this letter.” |

The letters were prepared at the end of February 2020 – leading firms to receive the communications in early March just when the COVID crisis escalated in Europe. By mid-March, Albania was in a lockdown that only ended in late May.

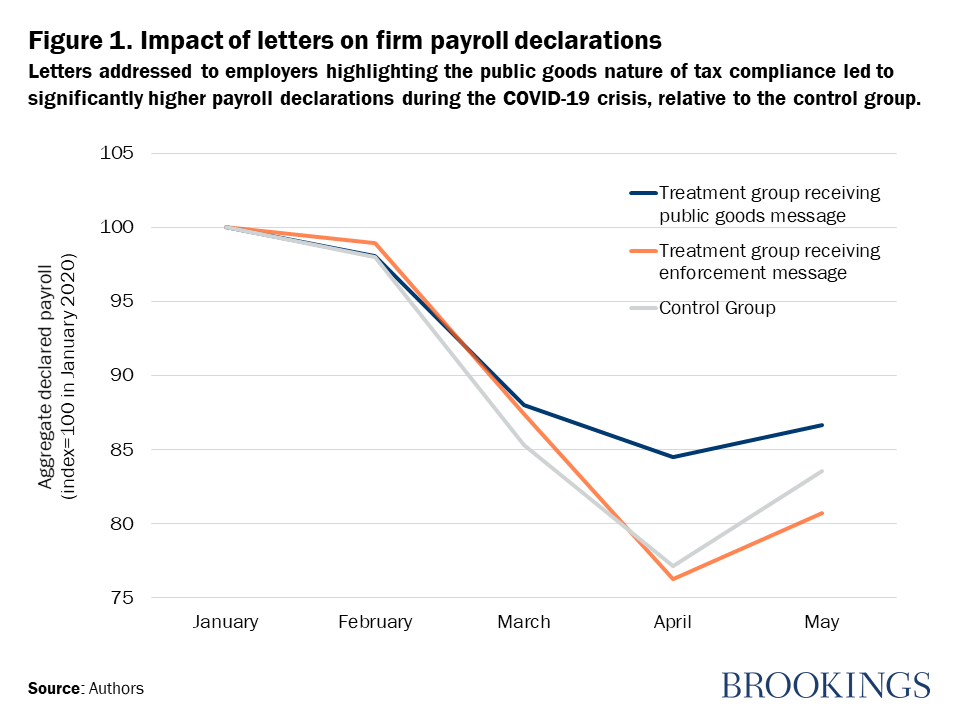

Given its coincidental timing, this communications pilot yields a useful window into how taxpayers react during the pandemic to messages prompting tax compliance. The graph below displays key results. Messages highlighting the public goods nature of tax compliance elicited significantly larger average payroll declarations relative to the control group, while enforcement messages had no statistically significant net impact on the average firm. This result stands in sharp contrast to most other existing studies—conducted in more normal times—that tend to find that enforcement messages are more effective.

Note: A panel regression of firm-level monthly payroll declarations on a treatment variable (identifying whether employers received a taxpayer communication and which type), time controls, and treatment-time interactions confirms that the treatment effect of the public goods message is statistically significant at the 5 percent significance level for the March and April declarations.

Results from this pilot may be specific to the current crisis context. As the pandemic is overcome, will enforcement messages gain more traction? During the crisis, many firms managed their payrolls more actively than usual to navigate the pandemic. In more normal times, will payroll declarations become less responsive to taxpayer communications? Will compliance gains be longer-lasting, as firms adjust their payroll declarations once and then are less likely to readjust them further? A parallel impact evaluation in spring 2020 that addressed letters to employees (instead of employers) found no significant compliance improvements. Will this result be overturned when communications are sent out in a period in which workers are back at their workplace (rather than under lockdown)?

These are questions that will require continued rigorous testing of alternative communication strategies going forward. Leveraging behavioral insights is a continuous process that needs to become embedded in the public policy design process—the potential benefits for tax administrations, but also for other public sector institutions, are large.

In the context of taxpayer communications during the pandemic, however, the results of this pilot seem to confirm Theodore Roosevelt’s adage: “Speak softly and carry a big stick; you will go far.”

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How should governments communicate with taxpayers during the COVID-19 pandemic?

September 14, 2020